US Market Open: NQ dragged lower by Meta (-13%) post-earnings, DXY softer & Antipodeans benefit from metals prices

25 Apr 2024, 11:05 by Newsquawk Desk

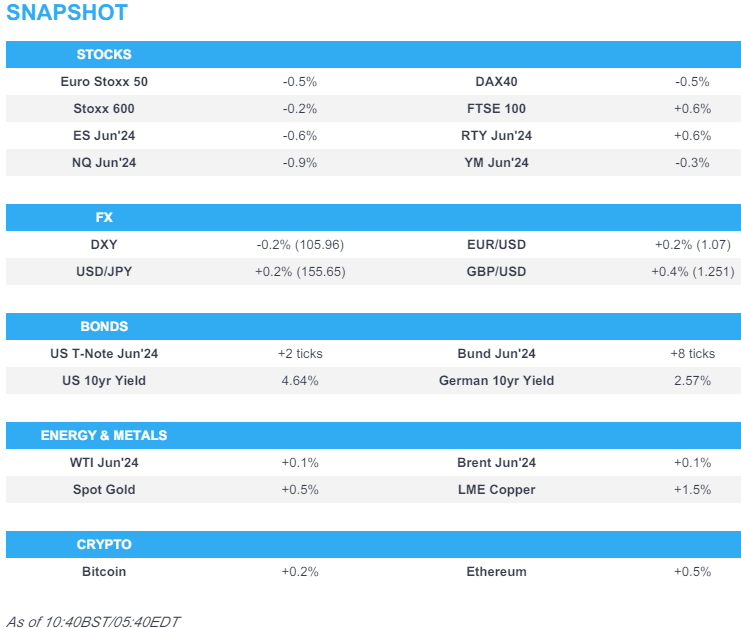

- European bourses are mostly lower, US equities are mixed, with the NQ underperforming after Meta (-13.1%) results

- Dollar is lower, Antipodeans benefit from higher metals prices, JPY is softer holding above 155.50 against the USD

- Bonds are rangebound awaiting impetus from Tier 1 data later today

- Crude is slightly lower in absence of energy-specific newsflow, XAU benefits from the weaker dollar, base metals are mostly firmer

- Looking ahead, US GDP Advance, PCE Advance, Initial Jobless Claims, Comments from ECB’s Nagel & Panetta, Supply from the US, Earnings from Merck, Microsoft, Gilead Sciences, Caterpillar, S&P Global, Intel, T-Mobile US & Alphabet.

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx600 (-0.1%) initially opened mixed, though sentiment quickly soured and indices now hold a negative bias.

- European sectors hold a negative tilt; Basic Resources is the clear outperformer, with Anglo American (+11.5%) taking the lion’s share of the gains on BHP takeover reports; positive price action in the metals complex is also helping. Food Beverage & Tobacco is found at the foot of the pile, following post-earning losses in Nestle (-3.9%) and Pernod Ricard (-2.9%).

- US Equity Futures (ES -0.5%, NQ -0.9%, RTY +0.5%) are mixed, with clear underperformance in the tech-heavy NQ, dragged down by Meta (-13%) post-earnings, with IBM (-8%) also fuelling the downside.

- Click here and here for the sessions European pre-market equity newsflow.

- Click here for more details.

FX

- Dollar is losing ground vs. peers (ex-JPY) with no obvious driver. DXY dipped under yesterday's 105.59 trough but it remains to be seen how much the dollar is sold ahead of upcoming tier 1 US data.

- EUR is benefiting from the broad softness in USD with EUR/USD eclipsing yesterday's 1.0714 peak and eyeing the 12th April high at 1.0729.

- GBP is enjoying a session of gains vs. the USD and to a lesser extent the EUR. Cable is back on a 1.25 handle for the first time since April 12th; 1.2558 was the high that day, which roughly coincides with the 200DMA at 1.2557.

- JPY is the only of the majors losing ground to the USD as USD/JPY's ascent above 155.50 overnight is sustained. Intervention speculation remains. However, comments from an LDP lawmaker yesterday that 160 could be the line of the sand has given USD/JPY bulls confidence to chase prices higher.

- Antipodeans are at the top of the leaderboard for the majors vs. the USD. AUD/USD breached its 200DMA at 0.6526 alongside strength in copper and iron prices.

- Click here for more details.

- Click here for NY Option Expiry details.

FIXED INCOME

- USTs are in consolidation mode below the 108 mark as traders brace for today and tomorrow's tier 1 US data. For today's quarterly PCE data, ING notes that a 0.4% MoM reading tomorrow could see Fed easing expectations cut back to just 25bp. Currently USTs remain contained within yesterday's 107.20-108.02.

- Steady trade for Bunds with macro drivers on the light side, and unreactive to typical hawkish-leaning commentary from ECB's Muller; Bunds are contained within yesterday's range with greater attention to the downside with the 10yr just circa 20 ticks above the recent contract low.

- Gilts are marginally firmer in quiet UK trade. However, the modest gains need to be taken in the context of recent selling pressure post-Pill. 96.18 is the high for today but is a far cry from Wednesday's 96.67 peak.

- Click here for more details.

COMMODITIES

- Choppy sideways trade for the crude complex; initial gains in the morning have now faded, with oil prices now lower on the session; Brent June in a USD 87.80-88.49/bbl parameter.

- Firm bias across precious metals amid a weaker Dollar and as geopolitical risks remain. Price action is more contained ahead of US GDP and PCE. XAU found support at USD overnight support at 2,305/oz before rising to a USD 2,328.88/oz intraday peak.

- Base metals are mostly firmer with clear outperformance in copper prices this morning and gains in iron overnight, with desks citing robust Chinese demand prospects. Elsewhere, mining giant BHP made a takeover offer for peer Anglo American.

- Click here for more details.

NOTABLE EUROPEAN HEADLINES

- ECB's Schnabel said may face bumpy last mile of disinflation; wage growth seems to be easing in line with projections.

- ECB's Muller said not comfortable starting with back-to-back cuts, via Bloomberg.

- BHP (BHP AT) confirmed that on the 16th April, it made an offer to Anglo America (AAL LN) regarding a potential combination; valuing Anglo American's share capital at GBP 31.1bln (vs GBP 25.75bln market cap on Wednesday's close)

DATA RECAP

- German GfK Consumer Sentiment (May) -24.2 vs. Exp. -26.0 (Prev. -27.4, Rev. -27.3)

NOTABLE US HEADLINES

- Apple (AAPL) China smartphone shipments grew 6.5% Y/Y to 69.3mln units in Q1, according to data from IDC, while Apple (AAPL) shipments in China fell 6.6% Y/Y in Q1.

- Boeing (BA) DoJ aims to determine by late May if Boeing breached an agreement shielding it from criminal prosecution over 2018 and 2019 fatal crashes, Reuters reports. Families of victims urged prosecution in five-hour meetings on Wednesday. Separately, Boeing said it was disappointed at not advancing in the US Air Force's Collaborative Combat Aircraft programme, but remains committed to delivering next-gen autonomous combat aircraft, including MQ-25 Stingray, MQ-28 Ghost Bat, and undisclosed proprietary programmes.

EARNINGS

- Meta Platforms Inc (META) Q1 2024 (USD): EPS 4.71 (exp. 4.32), Revenue 36.46bln (exp. 36.16bln), Q2 24 revenue view 36.5-39bln (exp. 38.38bln), FY24 capex view 35-40bln (exp. 34.73bln), also expects capex to increase in FY25 (exp. 37.73bln). Shares are down -12.9% pre-market.

- International Business Machines Corp (IBM) Q1 2024 (USD): Adj. EPS 1.68 (exp. 1.60), Revenue 14.46bln (exp. 14.55bln). Shares are down 8.5% pre-market

- Ford Motor Co (F) Q1 2024 (USD): Adj. EPS 0.49 (exp. 0.42), Revenue 42.8bln (exp. 40.1bln). Shares are up 3.2% pre-market

- Barclays (BARC LN) Q1 (GBP): Investment Bank Revenue 3.33bln (exp. 3.35bln). FICC Revenue 1.4bln (exp. 1.52bln); affirms FY24 NII guidance. CEO said seeing an uptick in deals flow and equity markets

- AstraZeneca (AZN LN) Q1 (USD): Core EPS 2.06 (exp. 1.89). Revenue 12.7bln (exp. 11.9bln); Confirms a 7% increase in the annual dividend announced at AGM.

- Unilever (ULVR LN) Q1 (GBP) Revenue 15bln (exp. 14.7bln). Underlying Sales +4.4% (exp. +3.6%). Co. is increasingly confident in its ability to deliver sustained volume growth and positive mix; affirms FY24 underlying sales growth.

- Nestle (NESN SW) Q1 (CHF): Organic Revenue +1.4% (Exp. 2.9%); Revenue 22.1bln (prev. 23.5bln Y/Y). CEO said “We had expected a slow start and see a strong rebound in Q2 with reliable delivery for the remainder of the year.”

- STMicroelectronics (STM FP) Q1 (USD): Revenue 3.47bln (exp. 3.63bln). Guides Q2 Revenue 3.2bln (exp. 3.8bln) and gross margin 40% (exp. 42.4%). Cuts FY24 Revenue guidance amid slower than expected Auto chip demand, now between 14-15bln (exp. 16.2bln). (Newswires)

GEOPOLITICS

- Russian Foreign Ministry said the appearance of NATO nuclear facilities in Poland makes it a military target for Russia, according to Al Arabiya.

- Belarusian President Lukashenko said probability of incidents on the Belarusian-Ukrainian border is quite high; around 120k Ukrainian servicemen deployed near the border; Belarus has moved several battalions of fully operational readiness to the border.

CRYPTO

- Bitcoin was ultimately flat in choppy trade and briefly approached near the USD 64,000 level.

APAC TRADE

- APAC stocks were mostly subdued after the uninspiring handover from the US where futures were pressured after-hours following Meta's underwhelming guidance, while the region also digested several earnings releases and markets in both Australia and New Zealand markets were closed for ANZAC Day.

- Nikkei 225 underperforms and retreated beneath the 38,000 level amid tech weakness and with earnings releases influencing price action, while the BoJ also kick-started its 2-day policy meeting.

- KOSPI was dragged lower amid losses in tech heavyweights despite stronger-than-expected GDP data and a blockbuster earnings report from SK Hynix.

- Hang Seng and Shanghai Comp. were positive with the Hong Kong benchmark underpinned amid resilience in the property industry, while the mainland eked slight gains after Premier Li noted China seeks to enhance development momentum and with US Secretary of State Blinken calling for the US and China to manage differences responsibly during a trip to China.

NOTABLE ASIA-PAC HEADLINES

- China is to speed up the local government special bond offer and is expected to accelerate special bond issuance in Q2 and Q3, according to PBoC-backed Financial News.

- China's mission to the EU said if the European side suspects the existence of so-called subsidies, it is entirely possible to verify and resolve the situation through communication with the firm or a government department, after Chinese security equipment company Nuctech's Dutch and Polish offices were raided by EU competition regulators.

- US Secretary of State Blinken called for the US and China to manage differences responsibly, according to AFP.

- Japanese Chief Cabinet Secretary Hayashi said won't comment on forex levels or intervention but reiterated it is important for currencies to move in a stable manner reflecting fundamentals and rapid FX moves are undesirable, while he added they are closely watching FX moves and will be ready to take full response.

- Japanese Finance Minister Suzuki said closely watching FX markets and will handle it appropriately.

- South Korea's market watchdog is preparing a new monitoring system to detect illegal stock short selling with the new mechanism to be implemented in a speedy manner, according to Reuters.

- CNOOC (883 HK) Q1 (CNY): Net 39.7bln (+24% Y/Y). Oil & Gas sales revenue CNY 89.98bln. Total net production -9.9% Y/Y

APAC DATA RECAP

- South Korean GDP QQ Advance (Q1) 1.3% vs. Exp. 0.6% (Prev. 0.6%); GDP YY Advance (Q1) 3.4% vs. Exp. 2.4% (Prev. 2.2%)