US Market Open: AAPL climbs post-earnings, NFP & Fed speak ahead

03 May 2024, 11:10 by Newsquawk Desk

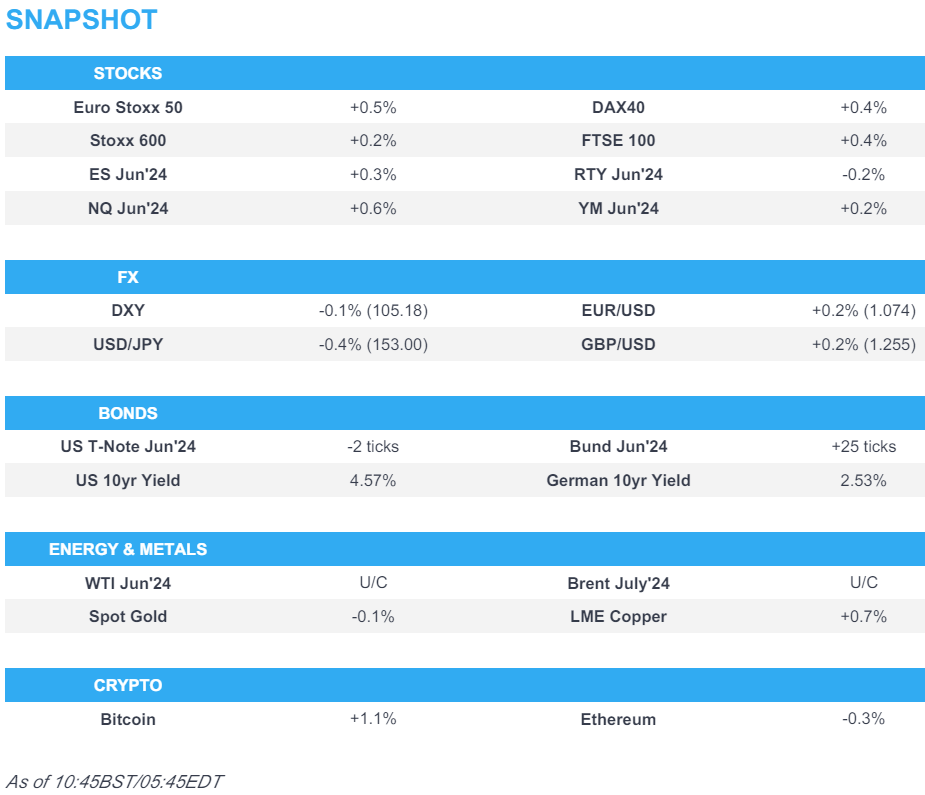

- European equities entirely in the green; US equity futures are mixed ahead of US NFP

- Dollar is slightly softer, USD/JPY dips lower to around 153.00

- Bonds are mixed but remain rangebound ahead of today’s key events

- Crude trades within a tight range, XAU flat and base metals mostly firmer

- Looking ahead, US NFP, Services PMI & ISM Non-Manufacturing, Comments from Fed's Goolsbee & Williams

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx600 (+0.2%) are entirely in the green, and with price action fairly muted as participants await the US Employment report at 13:30 BST / 08:30 EDT.

- European sectors hold a strong positive tilt, with Media taking the top spot, lifted by post-earning gains in JCDecaux (+12.5%) and UMG (+2.5%). Healthcare is found at the foot of the pile, dragged lower by Novo Nordisk (-4.5%), after recent Amgen updates.

- US Equity Futures (ES +0.3, NQ +0.6%, RTY -0.2%) are mixed, with clear outperformance in the NQ lifted by pre-market gains in Apple (+5.7%) after its earnings.

- Click here and here for the sessions European pre-market equity newsflow, including notable earnings/updates from: Shell, Maersk, Novo Nordisk and more.

- Click here for more details.

FX

- DXY is modestly lower on NFP day and within 105.16-37 confines after dipping under yesterday's trough (105.29) in APAC hours as with the next downside level the 11th April low (105.03) before the round figure.

- Sideways trade for the EUR against the Dollar amid a lack of drivers, whilst dovish ECB commentary continues with ECB's Lane yesterday. EUR/USD trades within a narrow 1.0725-45 parameter at the time of writing.

- Yen stands as one of the G10 outperformers despite a lack of fresh headlines following this week's double suspected intervention. USD/JPY trades in a 152.76-153.75 intraday band with potential support at the 12th April low (152.59).

- Antipodeans are modestly firmer and holding on to recent spoils and remained afloat amid the constructive mood but with price action quiet amid a lack of drivers. AUD/USD briefly topped its 100 DMA (0.6581).

- NOK came under some modest pressure as policy settings were maintained by Norges Bank but then appreciated slightly on the line that "the data so far could suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged."

- Click here for more details.

- Click here for OpEx for today's NY Cut

FIXED INCOME

- USTs are flat/incrementally softer with the curve flattening on the margin as the post-FOMC steepening settles into NFP and Fed speak. Currently within a busy 114'25-155'04 range.

- Bunds are firmer but only modestly so with overnight action sparse on account of Japan's holiday and EZ-specific drivers limited thus far; docket very much focused on US NFP & ISM Services alongside a handful of Fed speakers.

- Gilt price action has been in-fitting with EGBs after Thursday's session of outperformance. UK specifics light before Monday's bank holiday and then a packed week incl. the BoE on Thursday.

- Click here for more details.

COMMODITIES

- Crude is modestly firmer intraday but consolidating in the grander scheme after futures were relatively flat yesterday following a choppy session as participants await developments on the Israel-Hamas front after reports noted of "positive" spirit in talks. Brent July trades in a USD 83.77-84.15/bbl range.

- Precious metals are subdued but contained ahead of key US data and amid the absence of updates on the geopolitical front. XAU sits in a narrow USD 2,297.85-2,308.80/oz parameter.

- Base metals are mostly firmer across the board, but more so consolidation after yesterday's weakness, with sentiment not helped by the absence of Chinese markets.

- Click here for more details.

NOTABLE EUROPEAN HEADLINES

- Norges Bank maintains its Key Policy Rate at 4.50% as expected; the data so far could suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged. Click here for more details. Norges Bank Chief Bache says Norges has not decided when to cut rates.

- UK opposition Labour party wins Blackpool South by-election, taking the seat from the Conservatives in a blow for PM Sunak, according to BBC. It was also reported that the Labour party gained Hartlepool from no overall control in the local elections and they also claimed a win for Thurrock Council which the Tories won last year but had moved to no overall control after defections. Thus far, only around 30 of the 107 councils have declared but the swing as it stands is to Labour at the expense of the Conservatives. As a reminder, there have been reports in recent days that a bad result at the local elections could see MPs put in a no-confidence vote in PM Sunak in the next week or so.

- ECB's Lane said given the lags in transmission, the tightening effects from past interest rate hikes are still unfolding, while he noted expectations of future inflation normalising further and that leaving nominal rates unchanged implies a mechanical increase in real interest rates. Lane said moving from one meeting to the next meeting and from one projection round to the next projection round allows for the accumulation of further data that can help inform the rate decision. Furthermore, Lane said inflation has declined more quickly than expected and noted the more the data validates inflation coming back to the target, the more they will be able to remove restrictions this year and next year.

- ECB's Stournaras said three ECB rate cuts are more likely this year and the latest euro-area GDP figures were a positive surprise, according to comments made to Liberal cited by Bloomberg.

- German Engineering Orders -17% Y/Y in March (Domestic -23%; Foreign Orders -15%), Jan-Mar orders -13% (Domestic -16%; Foreign -12%), according to VDMA

DATA RECAP

- UK S&P Global PMI: Composite - Output (Apr) 54.1 vs. Exp. 54 (Prev. 54); S&P Global Services PMI (Apr) 55.0 vs. Exp. 54.9 (Prev. 54.9)

- EU Unemployment Rate (Mar) 6.5% vs. Exp. 6.5% (Prev. 6.5%)

- French Industrial Output MM (Mar) -0.3% vs. Exp. 0.3% (Prev. 0.2%); Budget Balance (Mar) -52.78B (Prev. -44.03B)

- Turkish CPI YY (Apr) 69.8% vs. Exp. 70.33% (Prev. 68.5%); Core 75.81% (exp. 75.70%)

EARNINGS

- Apple Inc (AAPL) Q2 2024 (USD): EPS 1.53 (exp. 1.50), Revenue 90.75bln (exp. 90.01bln); to buy back additional 110bln of shares and boosts quarterly dividend 4% to 0.25/shr, Revenue breakdown: Products 66.89bln (exp. 66.95bln), iPhone 45.96bln (exp. 45.76bln), Mac 7.45bln (exp. 6.79bln), iPad 5.56bln (exp. 5.91bln), Wearables, home and accessories 7.91bln (exp. 8.29bln), Service 23.87bln (exp. 23.28bln), Greater China revenue 16.37bln (exp. 15.87bln). Shares +5.9% in pre-market trade

- Amgen Inc (AMGN) Q1 2024 (USD): Adj. EPS 3.96 (exp. 3.87), Revenue 7.45bln (exp. 7.44bln); Still sees share buyback up to 500mln. Shares +14.9% in pre-market trade

- Booking Holdings Inc (BKNG) Q1 2024 (USD): EPS 20.39 (exp. 14.06), Revenue 4.40bln (exp. 4.25bln). Shares +1.9% in pre-market trade

GEOPOLITICS

MIDDLE EAST

- Israeli air strike hit a security building outside the Syrian capital of Damascus, according to a security source cited by Reuters, while Syrian state media later reported that 8 soldiers were injured in the Israeli airstrike on the outskirts of Damascus.

- Hezbollah announced it targeted the headquarters of Israel's 91st Division in the Branet barracks with rocket-propelled grenades, according to Sky News Arabia.

- Islamic Resistance in Iraq launched attacks on targets in Israel with Arqab-type cruise missiles from Iraqi territory which was the first attack targeting Israel's Tel Aviv by the Islamic Resistance in Iraq, according to a source in the group.

- Israel National Security Minister Gvir called on PM Netanyahu to remove Defence Minister Galant from office as he is not fit to continue his work as the defence minister.

- Israel's Foreign Minister said Turkish President Erdogan is breaking agreements by blocking ports for Israeli imports and exports.

OTHER

- Russian military personnel entered an air base in Niger that is hosting US troops which follows a decision by Niger's Junta to expel US forces from the country, according to Reuters citing a US official. However, US Defense Secretary Austin later commented that Russians do not have access to US forces or equipment in Niger and they will continue to watch the presence of Russian forces in Niger.

CRYPTO

- Bitcoin is modestly firmer and holds just above USD 59k, whilst Ethereum is still yet to firmly breach USD 3k.

APAC TRADE

- APAC stocks took impetus from Wall St where equities extended on post-FOMC gains and futures were also lifted by Apple's earnings beat, but with upside capped in the region amid key market closures including in Japan and Mainland China.

- ASX 200 traded higher as real estate led the outperformance in the rate-sensitive sectors.

- Hang Seng extended its rally after having recently entered a bull market and following stronger GDP data.

NOTABLE ASIA-PAC HEADLINES

- China May Day railway travel reached a record high of around 20.7mln trips, according to Xinhua.

- US FCC said roughly 40% of US telecom companies cannot replace Huawei or ZTE equipment in US networks without additional government funding.

APAC DATA RECAP

- Australian Judo Bank Services PMI Final (Apr) 53.6 (Prelim. 54.2); Judo Bank Composite PMI Final (Apr) 53.0 (Prelim. 53.6)