US Market Open: US equity futures gain alongside strength in USD/USTs as traders await US Budget updates

22 May 2025, 11:22 by Newsquawk Desk

- US President Trump's Tax/Spending bill is currently being debated in the US House (passed the Rules Committee overnight), the debate has formally hit the two-hour minimum as of the time of publication; vote time TBC.

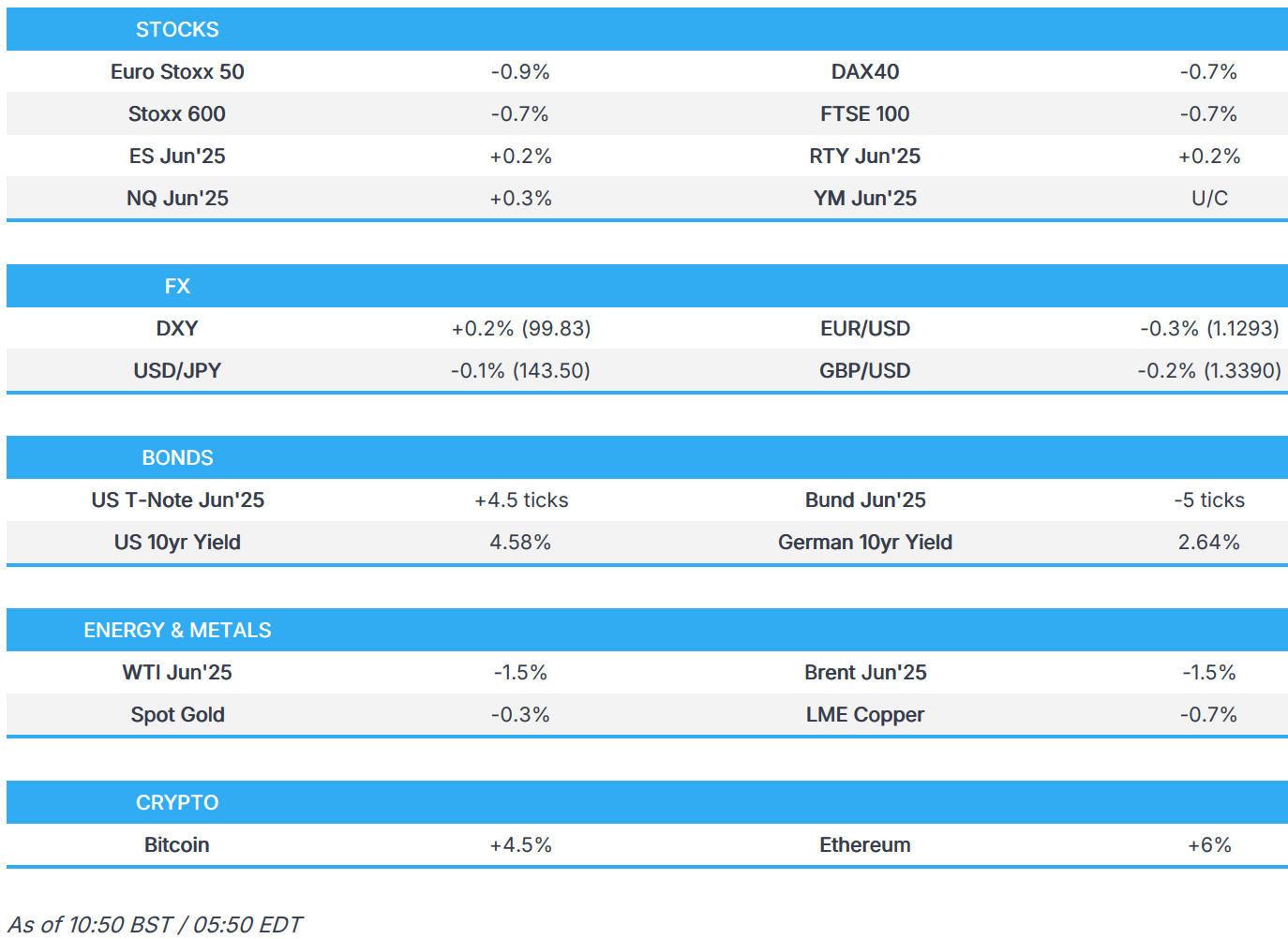

- European stocks trade lower following the Wall Street and APAC losses; US equity futures attempt to recover recent losses.

- USD mixed vs. peers, EUR and GBP digest PMI metrics, JPY narrowly leads.

- USTs a little firmer finding some reprieve following 20yr weakness, Bunds choppy following EZ PMIs.

- Crude pressured amid reports of further OPEC+ output hikes, Spot gold a little lower.

- Bitcoin extended on gains and printed a fresh all-time high of above the USD 111k level; Texas House approved the bill to create a Bitcoin reserve.

- Looking ahead, US Flash PMIs, Jobless Claims, Canadian Producer Prices, NZ Retail Sales, ECB Minutes. Speakers including RBA’s Hauser, BoE’s Breeden, Dhingra & Pill, ECB’s Elderson & de Guindos, BoC’s Gravelle, Fed’s Barkin & Williams, Supply from the US.

TARIFFS/TRADE

- EU is open to extending lobster deal as part of a package to remove tariffs imposed by US President Trump, according to FT.

- South African President Ramaphosa said following a meeting with US President Trump that they had discussions on trade and there will continue to be engagement on tariffs. It was also reported that South Africa's Trade Minister said they submitted a proposal regarding a framework agreement with the US and had some US feedback, while they then resubmitted a revised document with the proposal about a trade agreement.

- Canada's Minister of International Trade and Intergovernmental Affairs LeBlanc is to visit Washington DC to meet with Trump admin officials, while it was also reported that Canada's Finance Minister Champagne said he will discuss Canada's role as the largest customer for US exports in meeting with US Treasury Secretary Bessent.

- Japanese Finance Minister Kato said he told Bessent that US tariffs are regrettable and stated tariffs are not an appropriate means to correct macroeconomic imbalances that are behind trade imbalances, while Kato noted that he did not directly discuss Japan's US Treasury holdings in the meeting with Bessent.

- US Treasury Secretary Bessent and Japanese Finance Minister Kato discussed global security and bilateral trade and currency issues on the sidelines of the G7, while they reaffirmed shared belief that exchange rates should be market-determined and reaffirmed USD/JPY exchange rate currently reflects fundamentals.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.7%) opened lower across the board, in a continuation of the pressure seen on Wall St/APAC trade and have traded at subdued levels throughout the morning.

- European sectors hold a strong negative bias, with only Basic Resources and Chemicals marginally holding in positive territory. Consumer Products is underperforming after LVMH’s (-1.5%) cautious comments on the Luxury sector. Chemicals names are faring better vs peers, with Bayer (+1.7%) doing much of the heavy lifting. The Co. benefits from a WSJ report which suggests the US HHS Secretary's move will “go easier than expected on pesticides in farming”.

- US equity futures (ES +0.2%, NQ +0.3%, RTY +0.1%) are modestly higher across the board, attempting to recover some of the hefty losses seen on Wednesday; the pressure was attributed to deficit concerns and following a weak US 20yr auction, which sparked sell-US trade. US Flash PMIs, Jobless Claims and Fed speak via Williams/Barkin are due.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- USD is currently relatively steady and mixed vs. peers following three consecutive sessions of losses. With trade updates lacking, focus is currently on the fiscal front as markets await the outcome of the House vote on President Trump's tax bill. If the bill passes this hurdle, attention from an FX perspective will be on how back-end US rates react to the price tag and impact on the deficit. This week's data highlights are presented today via weekly claims and flash PMI metrics. The latter will likely carry greater sway as markets look for evidence on how the trade war is impacting US business. Fed speaker's today include Williams and Barkin.

- The rally in the EUR has paused for breath. This morning's macro focus has been on EZ PMI metrics which have painted a picture of a stabilising manufacturing sector but a slowdown in the services industry. The trade war is clearly acting as a cloud over the Eurozone economy; note, yesterday Bloomberg reported that the EU is preparing a trade proposal for the US to steer momentum into talks. Today's docket sees the ECB's account of the April meeting. Currently trading around the 1.13 mark.

- JPY is top of the G10 leaderboard alongside the soft risk sentiment and as markets digest comments from Japanese Finance Minister Kato and BoJ board member Noguchi. On the former, Kato noted that he agreed with US Treasury Secretary Bessent that FX rates should be set by markets and they did not directly discuss Japan's US Treasury holdings. Elsewhere, BoJ's Noguchi, in response to recent moves in Japanese yields, said that he does not think it is appropriate to recklessly intervene to correct bond yield moves.

- GBP is a touch firmer vs. the USD and extending its winning run for a fourth consecutive session. The latest round of PMI metrics from the UK saw the services component beat expectations and return to expansionary territory, manufacturing missed but ultimately, the composite rose and just about beat the consensus. Looking ahead, today's speaker slate sees a trio of MPC members with Breeden, Dhingra & Pill all due on deck. Cable is currently contained within Wednesday's 1.3380-1.3468 range.

- Mildly diverging fortunes for the Antipodes with AUD outperforming NZD as the AUD/NZD cross looks to close the post-RBA gap lower. Incremental newsflow for both has been lacking as the New Zealand Budget and forecasts garnered little fanfare and comments from RBA's Hauser proved to be non-incremental.

- PBoC set USD/CNY mid-point at 7.1903 vs exp. 7.2009 (Prev. 7.1937).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are a little firmer, attempting to recover following the hefty losses seen in the prior session following a weak US 20yr auction. Focus firmly is on the fiscal front. Overnight, the House Rules Committee passed President Trump’s tax/spending bill. Thereafter, the broader floor voted to open debate on the tax bill, a debate process that lasts for around two hours (started approx. 08:00BST) and is followed by a vote on the bill. Progress on the bill is bearish for USTs as it will increase the US’ debt level, a figure which has been increasing and was the driver behind the Moody’s downgrade last week. USTs currently trading around 109-19.

- Bunds started the day in the red but currently at the upper-end of a 129.49-91 band. Bunds have been gradually making their way off lows throughout the morning, edging higher slowly into the day’s data points which have featured generally weak Flash PMIs, with the expectation of Manufacturing where tariff-mitigation measures appear to have provided some support. No real reaction to the German Ifo figures at the same time. Ahead, ECB Minutes though as usual these will be deemed stale; focus will be on ECB's de Guindos, Elderson and Escriva throughout the day.

- Gilts are softer, trading slightly weaker than EGBs throughout the morning as has been the case at several points over the last few weeks but with today’s underperformance likely a function of Gilts reacting to Wednesday’s US auction and borrowing data this morning. PSNB data this morning came in well above expectations and the prior, though that was subject to a downward revision, in another unwelcome series for Chancellor Reeves after the hotter-than-expected inflation print earlier this week. Given all this, Gilts opened lower by 18 ticks and then slipped another 13 to a 90.29 trough in short order.

- Swedish Debt Office sees the 2025 deficit at SEK 93bln (Nov. forecast 65bln), nominal bond volume SEK 118bln (Nov. forecast 100bln); "new plan also contains an additional foreign currency bond for this year".

- Spain sells EUR 6.2bln vs exp. EUR 5.5-6.5bln 5.15% 2028, 3.10% 2031 & 1.00% 2042 Bonds.

- France sells EUR 12.497bln vs exp. EUR 10.5-12.5bln 2.40% 2028, 2.70% 2031, 0.00% 2032 OATs.

- Click for a detailed summary

COMMODITIES

- Crude futures were pressured overnight by the downbeat mood across markets and following bearish inventory data. Renewed pressure was seen during the European morning amid source reports that OPEC+ members are reportedly discussing whether to agree to another output hike of 411k BPD in July, via Bloomberg citing sources, although no agreement has been reached yet. WTI resides in a USD 60.37-61.75/bbl range while its Brent counterpart trades in a USD 63.67-65.03/bbl parameter.

- Overall, there is mixed trade across precious metals with hefty underperformance in spot palladium as it tracks the downbeat sentiment across the auto sector. Spot gold trades flat now and currently resides in a current USD 3,311.08-3,345.47/oz range.

- Base metals are mostly lower amid the broader downbeat risk profile, whilst Flash PMIs from Europe this morning were mixed but the commentary was mostly downbeat. 3M LME copper resides closer to the bottom end of a USD 9,495.65-9,579.20/t range at the time of writing.

- UK urged lowering price cap on Russian oil at the G7 meeting, according to Bloomberg.

- OPEC+ members are reportedly discussing on whether to agree to another output hike of 411k BPD in July, via Bloomberg citing sources; one of the options being discussed, no agreement has been reached yet.

- Click for a detailed summary

NOTABLE DATA RECAP

EZ PMIs

- EU HCOB Composite Flash PMI (May) 49.5 vs. Exp. 50.7 (Prev. 50.4); HCOB Services Flash PMI (May) 48.9 vs. Exp. 50.3 (Prev. 50.1); HCOB Manufacturing Flash PMI (May) 49.4 vs. Exp. 49.3 (Prev. 49.0)

- French HCOB Composite Flash PMI (May) 48.0 vs. Exp. 48.0 (Prev. 47.8); HCOB Services Flash PMI (May) 47.4 vs. Exp. 47.5 (Prev. 47.3); HCOB Manufacturing Flash PMI (May) 49.5 vs. Exp. 48.9 (Prev. 48.7)

- German HCOB Composite Flash PMI (May) 48.6 vs. Exp. 50.4 (Prev. 50.1); HCOB Services Flash PMI (May) 47.2 vs. Exp. 49.5 (Prev. 49.0); HCOB Manufacturing Flash PMI (May) 48.8 vs. Exp. 48.9 (Prev. 48.4)

- UK Flash Composite PMI (May) 49.4 vs. Exp. 49.3 (Prev. 48.5); Flash Services PMI (May) 50.2 vs. Exp. 50.0 (Prev. 49.0); Flash Manufacturing PMI (May) 45.1 vs. Exp. 46.0 (Prev. 45.4)

Other Data

- German Ifo Expectations New (May) 88.9 vs. Exp. 88.0 (Prev. 87.4); Ifo Current Conditions New (May) 86.1 vs. Exp. 86.8 (Prev. 86.4); Ifo Business Climate New (May) 87.5 vs. Exp. 87.4 (Prev. 86.9)

- UK PSNB Ex Banks GBP (Apr) 20.155B GB vs. Exp. 17.9B GB (Prev. 16.444B GB, Rev. 14.139B GB); PSNCR, GBP (Apr) 9.116B GB (Prev. 2.694B GB, Rev. 2.819B GB)

- French Business Climate Manufacturing (May) 97.0 vs. Exp. 99.0 (Prev. 99.0, Rev. 100)

NOTABLE EUROPEAN HEADLINES

- ECB's Nagel sees progress on the US tariff dispute but more hurdles to overcome and noted the US was showing a better understanding of Europe's point of view, while he is a little more confident than perhaps was a few days ago. Nagel stated that German economic growth in Q1 could surprise on the upside but will get worse in Q2 and could see 1% plus growth in 2026.

- ECB's Vujcic says "Euro area growth is positive but low; inflation is slowly converging to 2% target; expect to get close to 2% target at end-2025" Expect to reach 2% target in early 2026.

- IMF forecasts French growth of 0.6% in 2025 and 1% in 2026; says France needs fiscal effort of 1.1% of GDP in 2026, followed by an average of about 0.9% over the medium term; Says France needs credible and well-designed package of measures to rein in deficit over time.

- EU Parliament backs very high tariffs on nitrogen-based fertilisers and farm produce from Russia and Belarus.

NOTABLE US HEADLINES

- BofA Institute Total Card Spending (Week to 17th May) -0.7% (vs +1.0% average in April)

- US President Trump posted "I am giving very serious consideration to bringing Fannie Mae and Freddie Mac public. I will be speaking with Treasury Secretary Scott Bessent, Secretary of Commerce Howard Lutnick, and the Director of the Federal Housing Finance Agency, William Pulte, among others, and will be making a decision in the near future."

TRUMP'S TAX BILL

- US Tax/Spending Bill Timings: House floor debate on the bill is ongoing, the two hour minimum debate time runs out around 10:15BST/05:15BST. However, House Dems. can delay this, so the actual vote time is TBD but likely several hours away.

- US President Trump's Tax/Spending bill is currently being debated in the US House (passed the Rules Committee overnight), the debate has formally hit the two-hour minimum as of the time of publication. However, the timing of the vote is yet to be determined due to the Democrats possessing several procedural tools to delay it and, as Punchbowl reminds, the main unknown of House Minority Leader Jeffries' "Magic Minute", which enables him to speak for an unlimited duration. Punchbowl reports that Republicans expect him to speak for around one hour, but this is not a certainty.

- As a reminder, if the bill passes the House then it will move to various Senate committees before being debated and voted on by the Senate floor. A process that will likely take several weeks, after this, Trump has the final sign off.

GEOPOLITICS

MIDDLE EAST

- Iranian Foreign Minister says "We have a better understanding in many areas, but in some, especially enrichment, differences still remain. I think we cannot reach an agreement until this issue is resolved.", via Iran Nuances

- Israel is preparing to carry out a swift attack on Iran's nuclear facilities if nuclear talks between the US and Iran fail, via Walla citing sources.

- Israeli military said it identified and intercepted a missile launched from Yemen towards Israel.

- Two Israeli embassy employees were killed in a shooting near a Jewish museum in Washington DC, while the Washington DC police chief announced the suspect was detained by event security and had chanted "Free Palestine" while in custody.

RUSSIA-UKRAINE

- Moscow Mayor says Russian has downed two drones en route to Moscow

- US President Trump told European leaders in private that Russian President Putin isn't ready to end the war, according to WSJ.

OTHER

- North Korea said it will convene the ruling party central committee meeting in late June and North Korean leader Kim watched the launch of a 5000-ton destroyer, while an accident occurred during the launch of the North Korean warship. Furthermore, Kim said the accident was unacceptable and was the result of negligence and irresponsibility.

- Indian PM Modi says Pakistan will not get water, to which India has a right.

CRYPTO

- Bitcoin is on a stronger footing and has made a fresh ATH, currently trading above the USD 110k mark; Ethereum also moving higher.

APAC TRADE

- APAC stocks were on the back foot following the sell-off on Wall St where stocks, treasuries and the dollar were pressured amid deficit concerns and a weak 20-year auction.

- ASX 200 retreated with energy and tech front-running the declines, although continued strength in gold producers atoned for some of the losses.

- Nikkei 225 gapped beneath the 37,000 level amid a firmer currency and proceeded in a somewhat choppy fashion as participants also digested data releases, including a surprise surge in Japanese Machinery Orders and mixed PMI figures.

- Hang Seng and Shanghai Comp conformed to the downbeat sentiment in the absence of any fresh bullish catalysts and after recent earnings results failed to inspire, while the mainland initially showed resilience in early trade before succumbing to the broad risk-off mood.

NOTABLE ASIA-PAC HEADLINES

- PBoC to sell CNY 500bln of one year medium term lending facility loans on Friday.

- RBA's Hauser, on recent trip to China, says found confidence Beijing would do what was needed to sustain growth; Australian exporters upbeat about resilience of China demand Found striking confidence that China going into trade war with strong hand. China organisations expected large share of economic costs of tariffs would fall on US. China contacts expressed a determination not to cushion those costs. Found little expectation that yuan would be devalued to insulate US from tariffs. Possible could see more intense competition at home from Chinese firms discounting. Unclear how big an impact given limited overlap between Chinese and Australian output.

- BoJ's Noguchi says they do not look at the size of JGB buying from the standpoint of monetary policy. In tapering, market predictability and flexibility is the most important. Does not think it is appropriate to recklessly intervene to correct bond yield moves. Should not move on rates when there is a lack of clarity on economic outlook.

- Japanese Economy Minister Akazawa held unofficial phone talks with US Treasury Secretary Bessent before Wednesday, according to TV Tokyo; Bessent reportedly expressed reluctance to meet Akazawa this week; the two will meet next week instead.

- China's MOFCOM says China firmly opposes US export controls on Chinese AI chips.

DATA RECAP

- Japanese Machinery Orders MM (Mar) 13.0% vs. Exp. -1.6% (Prev. 4.3%); YY (Mar) 8.4% vs. Exp. -2.2% (Prev. 1.5%)

- Japanese JibunBK Manufacturing PMI Flash SA (May) 49.0 (Prev. 48.7); Services PMI Flash SA (May) 50.8 (Prev. 52.4)

- Japanese JibunBK Composite Op Flash SA (May) 49.8 (Prev. 51.2)

- Australian S&P Global Manufacturing PMI Flash (May) 51.7 (Prev. 51.7); Services PMI Flash (May) 50.5 (Prev. 51.0)

- Australian S&P Global Composite PMI Flash (May) 50.6 (Prev. 51.0)