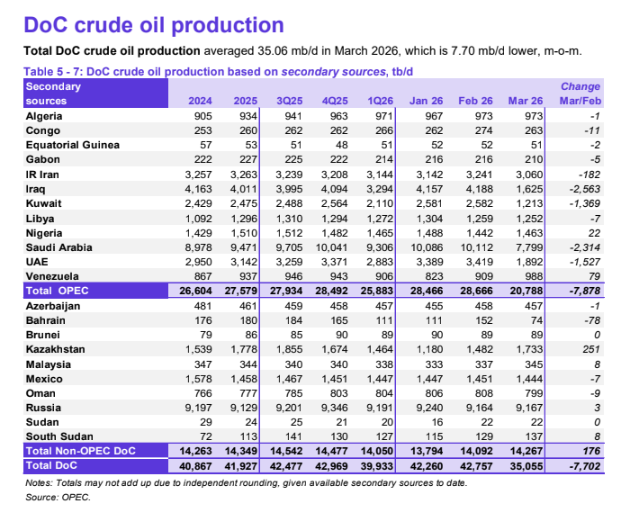

OPEC MOMR (Mar – Incorporates Iranian War): In March, crude oil production by countries participating in the DoC (OPEC+) dropped by 7.70mln BPD M/M, to average about 35.06mln BPD, according to available secondary sources

SUPPLY

- In March, crude oil production by countries participating in the DoC (OPEC+) dropped by 7.70mln BPD M/M, to average about 35.06mln BPD, according to available secondary sources.

- OPEC+ March crude production breakdown is available at the bottom.

DEMAND

- The demand for DoC crude (i.e., crude from countries participating in the DoC) in 2026 remains unchanged from the previous month’s assessment to stand at 42.9mln BPD.

- Global oil demand growth for 2026 is forecast at 1.4mln BPD Y/Y, unchanged from the previous month’s assessment.

- The OECD is forecast to grow by 0.1mln BPD, while the non-OECD is forecast to grow by about 1.3mln BPD.

- In 2027, global oil demand is forecast to grow by about 1.3mln BPD Y/Y, also unchanged from last month’s assessment.

- The OECD is forecast to grow by 0.1mln BPD, while the non-OECD is forecast to grow by around 1.2mln BPD.

REFINING MARGINS

- In March, refining margins surged across all major regions, given the sharp reduction in product output and rising middle distillate crack spreads, which reached multi-year highs.

- Trade flow constraints and refinery run cuts in the East of Suez contributed further pressure on product margins amid the heavy refinery maintenance season.

TANKERS

- In March, trade disruptions and moves to source alternative supplies pushed dirty tanker spot freight rates to record levels.

- On the West Africa-to-East route, VLCC spot freight rates rose 34%, M/M. Suezmax spot freight rates on the USGC-to-Europe route jumped 104%, M/M.

- Aframax rates were particularly strong West of Suez, with the Intra-Mediterranean route increasing 68%, while the Indonesia-to-East route experienced more limited gains of 8%, M/M.

PRICES

- In March, the OPEC Reference Basket (ORB) value increased by USD 48.46/bbl, month-on-month (m-o-m), to average USD 116.36/bbl.

- The forward curves of the three main crude oil futures benchmarks – ICE Brent, NYMEX WTI and GME Oman – steepened sharply in March, and the calendar spreads between the nearest futures contracts moved into deeper backwardation.

- Traders were pricing in significant short-term supply tightness amid escalating geopolitical tensions. Tight physical crude supply prompted refiners, particularly in the Asia- Pacific and Europe, to compete for available spot cargoes through aggressive bidding.

- Hedge funds and other money managers turned increasingly bullish on oil in March, sharply increasing their net long positions amid supply disruptions and rising oil prices.

ECONOMY

- Following sound global GDP growth in 2025, estimated at 3.3%, the global economy is expected to be able to generally absorb temporary events like trade-related challenges and the current Middle East geopolitical developments.

- While geopolitical developments in the Middle East have been to the fore in recent weeks, US tariff-related developments have been volatile since the beginning of the year. They may become a topic of interest again in the near-term as the US administration may again raise tariffs.

Context

OPEC’s latest Monthly Oil Market Report reveals a significant production drop of 7.70 million barrels per day from OPEC+ countries, indicating tightening supply amidst increasing geopolitical tensions. With global oil demand forecasts unchanged and refining margins rising sharply, this production decline could lead to upward pressure on crude prices, especially as traders anticipate supply constraints in the near term.

Trade the TapeGet this analysis live, the moment it breaksNewsquawk's real-time dashboard delivers market-moving headlines and instant context to your desk before the rest of the market reacts.

Open Dashboard#UNITED STATES#USD#EUR#JAPAN#JPY#UNITED KINGDOM#GBP#ASIA#EUROPE#INTERCONTINENTAL EXCHANGE INC#ORBITAL SCIENCES CORP#ORB.US#OPEC#OECD#DATA#GEOPOLITICAL#IMPORTANT#FOREX#EQUITIES#ENERGY#METALS#EU SESSION#US SESSION#GROSS DOMESTIC PRODUCT#WTI#BRENT#COMMODITIES#GOLD#FINANCIAL EXCHANGES & DATA#METALS & MINING#CAPITAL MARKETS#MATERIALS (GROUP)#FINANCIAL SERVICES#S&P 500 INDEX#ICE#BRENT CRUDE#DXY#EIA#TARIFF#TRADE#ENERGY & POWER#TRADE