Published: 28 Apr 2026, 10:10 UTC

Newsquawk Desk

US Market Open: NQ underperforms, DXY rises in tandem with Crude & BoJ shows hawkish vote split

0:00--:--

- US President Trump is reportedly not satisfied with and is unlikely to accept the Iranian proposal; CNN reports that the US and Iran are not as far apart as they seem.

- BoJ maintained its policy rate as expected, though subject to a hawkish 6-3 vote split, dissenters highlighted upside risks to inflation. Ueda non-committal on the timing of the next move.

- European bourses firmer, lifting incrementally after a contained open. US futures are mixed/lower into earnings and after OpenAI missed internal targets.

- JPY led post-BoJ before retreating and weakening on Ueda, USD firmer to the modest detriment of peers across the board; base & precious metals hit.

- Energy bolstered by the overnight updates, and as Iran's Foreign Minister is not returning to Pakistan post-Russia.

- Fixed falters as energy climbs, Bunds hit by the latest ECB surveys, Gilts lag into the Privileges debate regarding PM Starmer.

- Looking ahead, highlights include US ADP Weekly Employment Change, US House Price Index (Feb), US CB Consumer Confidence (Apr), US Richmond Fed Index (Apr), US Dallas Fed Index (Apr), NBH Policy Announcement (Apr), and speakers include ECB President Lagarde, Supply from the US.

- Earnings from RobinHood, Bloom Energy, Visa, Booking.com, NXP Semiconductor, UPS, Coca-Cola, Spotify, General Motors, Centene.

EUROPEAN TRADE

IRAN

- US President Trump has told advisers he is not satisfied with Iran’s latest proposal to reopen the Strait of Hormuz and end the war, NYT reported; a US official said that accepting it [the Iran proposal] could appear to deny Trump a victory. The proposal also called on the United States to end its naval blockade, but would have set aside questions about what to do with Iran’s nuclear program. A US official also said that accepting it [the Iran proposal] could appear to deny Trump a victory. US officials say Iran’s leadership has not authorised its negotiators to make concessions on the nuclear deal, frustrating any attempts to forge a compromise or peace agreement. At the heart of the debate over whether to accept the Iranian proposal were discussions in the Trump administration about the issue of economic leverage and what further American military operations would be needed to get Tehran to make significant concessions in negotiations. Some administration officials believe that continuing the blockade for two more months would cause significant long-term damage to Tehran’s energy industry. "Without a resumption of military action, there is little reason to think the Iranian position will shift.".

- US President Trump is reportedly sceptical of Iran’s Strait of Hormuz proposal, WSJ reported citing sources; said White House will continue to negotiate with Iran; White House expected to provide its response and counterproposals in the coming days. President Trump and his national security team are sceptical of Iran’s offer to open the Strait of Hormuz in exchange for tabling discussions on its nuclear work, according to US officials. Trump discussed the offer with aides on Monday morning, expressing doubts about Iran’s good faith and its willingness to meet his key demand of ending nuclear enrichment and committing never to develop a nuclear weapon. The US plans to continue negotiations with Iran, with the White House expected to provide its response and counterproposals in the coming days. White House spokeswoman stated that the US will not negotiate through the press and that anything not announced by President Trump or the White House should be considered speculation.

- US and Iran are not as far apart as they seem, and that the first part of any potential agreement will focus on opening the Strait of Hormuz without restrictions or fees, CNN reported, citing sources. The US and Iran may not have met for a second round of talks in Pakistan, but the two sides are not as far apart as they seem, according to sources familiar with the mediation process. Intense diplomacy continues behind the scenes, the sources say, and ongoing talks are centred around a staged process in which the first part of a potential deal would focus on returning to the status quo before the war and reopening the Strait of Hormuz without restrictions or tolls. The issue of Iran’s nuclear program – which both the US and Israel cited as their casus belli – would be addressed later. US President Donald Trump has previously said that any deal would require Iran to forfeit its supply of near bomb-grade uranium and give up enrichment, demands Iran has steadfastly refused to accept. According to the sources, mediators are applying pressure on both sides to reach an agreement, with the next few days being especially crucial. Hanging over it all is the chance that the US may decide to disengage and return to war.

- Israeli PM Netanyahu reportedly told US President Trump the Israel-Lebanon ceasefire is fragile, N12 reported citing sources. Netanyahu told Trump that he believes that the strategy he has chosen is correct for now, but that it can only succeed if there is no compromise with the Iranians regarding the Strait of Hormuz. Israel and the US see eye to eye on the Iranian issue. n discussions in Israel, the Iranian difficulty in pumping oil from the wells is raised, which puts them in great distress.

- "Netanyahu informed his ministers that there is no more he can do in Lebanon and this is what Washington wants", Al Jazeera reported citing an Israeli Radio source.

- Pakistan Defence Minister said "our earnest efforts to end the conflict, impacting the entire region and beyond, are ongoing, and we remain hopeful of achieving a positive outcome", reported Anas Mallick.

- Iran’s Deputy Defence Minister Talaei-Nik said Tehran is ready to share its defensive weapons capabilities with members of Shanghai Cooperation Organisation.

- "Kuwaiti News Agency: The Gulf Cooperation Council holds an extraordinary summit in Jeddah", Sky News Arabia reported.

- "Iran’s Foreign Minister is NOT returning to Pakistan following his Russia visit", journalist Mallick reported; "team is currently in consultation mode and will return when there to Islamabad, soon, when they think there is headway in talks.".

- reported of Israeli airstrikes in the south of Lebanon, Al Jazeera reported.

- US President Trump is unlikely to accept Iran's plan, according to CNN citing sources; reopening the strait without resolving the nuclear issues could remove a key piece of US leverage.

- "Guided-missile destroyer USS Rafael Peralta (DDG 115) enforces the U.S. blockade of Iranian ports against M/T Stream after it attempted to sail to an Iranian port, April 26", US CENTCOM said.

- US President Trump is unhappy with the Iranian proposal, according to a US official.

- Taiwanese Defense Ministry said that Taiwan has spotted two Chinese warships operating in waters near the Penghu Islands and has sent its own naval and air forces to keep watch.

- US Secretary of State Rubio said the ceasefire in Iran is unique because Israel is at war with Hezbollah, not Lebanon.

- US Secretary of State Rubio said the Iran offer is better than we thought. Indications that Iranian Supreme Leader Khamenei is alive. Direct communications with Iran are very rare and discreet. Level of sanctions and pressure on Iran is extraordinary. Hopes the rest of the world will sanction Iran.

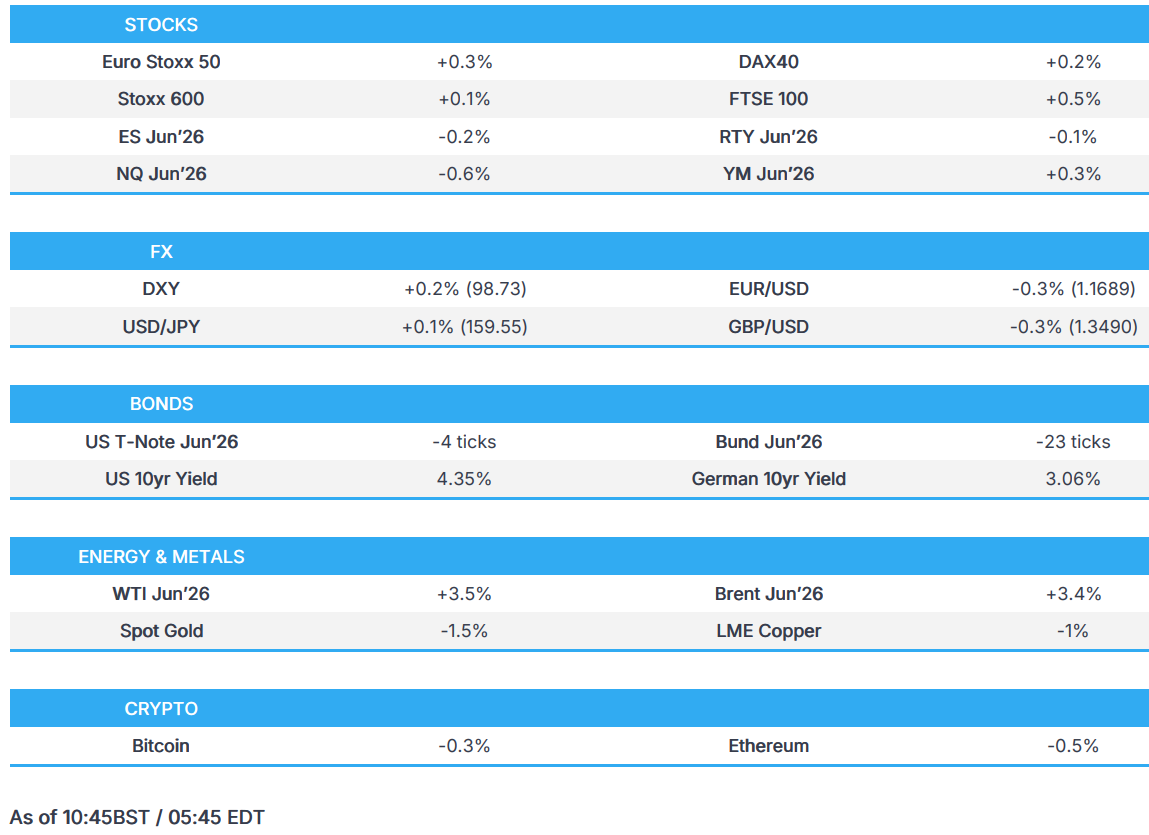

EQUITIES

- European bourses (STOXX 600 U/C) spent most of the European morning a touch lower after several geopolitical updates spurred energy benchmarks higher on the day. On the geopolitical front this morning, journalist Mallick said Iran’s Foreign Minister was not returning to Pakistan following his Russia visit - a post which soured the risk tone.

- European sectors opened mixed, and continue this way. Energy tops the pile amid BP's (+3.3%) stellar Q1 results, while Healthcare sits at the bottom amid losses in the sector's second-largest constituent Novartis (-2.6%), alongside Bayer (-2.7%). The former reported disappointing earnings, whilst the latter is hit on reports that the US Supreme Court is split over Bayer's fight against Roundup lawsuits.

- Stateside, indices are mixed, but have been moving a little lower in recent trade. NQ (-0.3%) underperforms on tech weakness after a WSJ article said OpenAI recently missed internal targets for new users and revenue. Its CFO was also said to have told employees the co. may be unable to pay for future computing contracts if revenue does not grow fast enough. Elsewhere, WSJ also reported Meta was preparing to potentially unwind its USD 2.5bln acquisition of Manus after China banned the transaction on national-security grounds.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- FX shows a risk-off bias with all G10 currencies lower against the Buck.

- DXY is back above its 100 & 200 DMAs around 98.50, after falling below those levels on Monday. The buck saw weakness after the BoJ announcement, where the vote split was more hawkish than expected at 6-3. However, following the meeting, the USD moved higher in tandem with crude benchmarks after news that Iran’s Foreign Minister was not returning to Pakistan following his visit to Russia.

- In addition to this, Ueda at the BoJ presser failed to support bets for a June hike, with the initial move seen on the 6-3 vote split paring to bring USD/JPY to above 159.50, to pre-announcement levels (ventured as low as 158.96). MUFG said the BoJ meeting was unlikely to trigger a sustained reversal of the bearish JPY trend that has been in place since the Middle East conflict started in late February

- Elsewhere, NOK fares the best against the USD amid firmer oil prices. NOK/SEK, +0.4%, continues to edge towards the 1.00 mark not seen since November 2024, with a session high of 99.63.

- GBP is one of the worst performers in the G10FX space, with UK Political developments in the spotlight ahead of a debate & vote on whether PM Starmer should be referred to the Privileges Committee (Full analysis on the headline feed at 09:05 BST) GBP/USD traders lower by 0.3% and breached the 1.35 mark, while EUR/GBP has been creeping higher throughout the session but remains flat on the day.

- Japanese Finance Minister Katayama said volatility in crude is affecting FX, ready to take decisive action; will closely coordinate with the US and will act when necessary; standing by around the clock.

FIXED INCOME

- Another bearish start for fixed income as energy climbs, and with some influence from a hawkish hold by the BoJ. (Details on geopols can be found in the commodities section below).

- Most recently, the ECB SCE saw an increase in inflation expectations for the next 12 months, and for three years ahead, both saw a significant increase to 4.0% (prev. 2.5%) and 3.0% (prev. 2.5%), respectively. By way of comparison, the March baseline HICP peak was 2.6% in 2026, the adverse 3.5% for the same period, while the severe peaked at 4.8% in 2027. As such, 12-month expectations are hotter than all but the severe scenario, a point that adds a measure of hawkishness ahead of Thursday's ECB. Though this view is somewhat offset by the tightening of credit conditions and weaker loan demand evidenced in the BLS, a survey that was released alongside the CSE.

- Amidst all this, Bunds down to a 124.87 base with a downside of nearly 50 ticks. The low was printed just after the ECB SCE release.

- USTs down to a 110-26 base into a session that is likely to once again be dominated by geopolitics, earnings and looking ahead to the FOMC on Wednesday. We do get supply, 2yr FRN and a 7yr note offered, following a strong 2yr and mixed 5yr on Monday.

- JGBs gapped lower on the resumption after the BoJ announcement, before then filling the move in short order. To recap, the BoJ was a hawkish-hold with three dissenters in favour of a hike, citing price concerns. Forecasts showed an increased inflation view, while the growth view was cut. Thereafter, Ueda was non-committal regarding the timing of the next hike, and seemingly attempted to temper expectations around June, commentary that had little JGBs impact but spurred notable JPY moves.

- Gilts gapped lower by 21 ticks, acknowledging the above, and have since fallen another 29 to an 86.51 trough. If the move continues, we look to 86.00 before 85.91 from the last week of March. Gilts underperform marginally, awaiting the start of the debate and then vote on whether UK PM Starmer should be referred to the Privileges Committee or not; full primer available at 09:05BST.

- Netherlands sold EUR 1.31bln vs exp. EUR 1-1.5bln 3.75% 2042 DSL: average yield 3.456%.

- China said to be weighing a second green sovereign bond sale, Bloomberg reported.

- Australia sold AUD 1.0bln 4.25% 2035 AGB; b/c 3.31x (prev. 2.35x), average yield 5.02% (prev. 4.63%).

COMMODITIES

- Crude prices are once again on a stronger footing this morning, with a number of sentiment-hitting headlines helping to lift demand for energy. In brief, CNN reported that President Trump is not satisfied with the Iranian proposal, adding that he is unlikely to accept it. But the piece did suggest that the US and Iran are not as far apart as they seem. Thereafter, Pakistani journalist Mallick reported that Iran’s Foreign Minister would not return to Pakistan following his visit to Russia, adding that he would only head back to the region if his team thinks there is “headway in talks”. This helped to spur some strength in both WTI and Brent, by around a USD 1/bbl.

- As it stands, WTI holds at the upper end of a USD 96.24-99.66/bbl range, whilst Brent sits at the upper end of a USD 107.81-111.86/bbl range.

- Sticking with geopols, but over in Europe, Ukraine said that it had struck Russia’s Tuapse oil refinery. It is considered amongst the top 10 largest in the country, with a capacity of 240k BPD. Elsewhere, on the supply front, Bloomberg reported that Saudi Arabia may cut its June OSP to Asia, citing easing demand.

- Spot gold is lower this morning, by around a percent, and currently resides towards the lower end of a USD 4,614-4,701/oz range. Ultimately, spot gold has been pressured throughout the Iranian conflict, given the inflationary implications – a theme which appears to have played out today; the mild strength in USD this morning is also a factor.

- Base metals also hold a negative bias – likely hampered by the downbeat risk tone seen during overnight trade. 3M LME Copper trades within a USD 13,105.98-13,264/t range.

- Saudi Arabia reportedly may cut its official June crude selling prices to Asia as spot premiums eased and demand eased, Reuters reported.

- Eneos (5020 JT) is reportedly the final bidder for some of the Asian assets of Chevron (CVX).

- ADNOC has told some oil buyers to pick up Gulf supply outside the Strait of Hormuz, as producers look to diversify to other routes and bring their oil to the market, Bloomberg reported. ADNOC has told customers of the availability of cargoes for loading off Fujairah.

- ADNOC is planning to invest tens of billions of dollars to build a natural gas business in the US to diversify its commodity exposure and the XRG business.

- Ukrainian drones attack Russia's Tuapse oil refinery, causing a fire, according to authorities.

- China allows the purchases of banned BHP (BHP AT) portside cargoes following a deal with the Co., according to sources.

- Venezuela is to raise crude shipments to 1.06mln bpd and fuel sales to 134k by year-end, PDVSA vice president said.

TRADE/TARIFFS

- Indonesia's Economy Minister said they are going to cut the import duty for naphtha to 0%.

NOTABLE EUROPEAN HEADLINES

- ECB Consumer Expectations Survey: 1yr CPI expectations 4% (exp. 2.8%, prev. 2.5%), 3yr CPI expectations 3.0% (exp. 2.6%, prev. 2.5%).

NOTABLE EUROPEAN DATA RECAP

- Italian PPI MoM (Mar) M/M 4.4% (Prev. -0.4%).

- Italian PPI YoY (Mar) Y/Y 4.2% (Prev. -2.7%).

- Italian Industrial Sales MoM (Feb) M/M 0.60% (Prev. -0.3%).

- Italian Industrial Sales YoY (Feb) Y/Y 0.5% (Prev. -1%).

- Spanish Retail Sales YoY (Mar) Y/Y 4.1% (Prev. 2.2%).

- Spanish Retail Sales MoM (Mar) M/M 1.2% (Prev. -0.1%).

- UK BRC Shop Price Inflation (Apr) 1.0% vs. Exp. 1.5% (Prev. 1.2%).

CENTRAL BANKS

- BoJ Governor Ueda said there are possibilities of a rate hike if either upward risks to prices emerge or downside risks to the economy are limited. By June, probably no big upward pressure appears in consumer price data. It is possible to decide before confirming upward price pressure in price data. Communicating closely with government on monetary policy. When asked if a rate hike is not possible while the Strait of Hormuz is closed, the decision would depend on inflation risks and the economy beyond that. Not thinking there is a high likelihood of the current situation resembling the early 1970s. If the trend inflation overshoots by 2% by a big margin, then strong tightening could be required. In the process of adjusting rates towards neutral, all other conditions being equal. Japan's exposure to private credit is not big; it requires caution, given transparency in the sector is low. Unless significant downside pressure to the economy, a rate hike is possible. Rate hike decision and QT adjustment will be separate. Inflation upward risk could be a reason for raising rates, but not the only reason. Can not say how many months it would take to gauge timing of next rate hike, will look to see if underlying inflation has a clear upward risks. Need to be mindful of further economic slowdown depending on supply shock levels; Japan economy has some degree of endurance.

- BoJ maintains its short-term interest rate at 0.75%, as expected; vote split 6-3 to hold (exp. near-unanimous); Nakagawa, Takata and Tamura voted to hike by 25bps to 1.0%.

- BoJ Outlook Report: Real GDP: Fiscal 2026 median forecast 0.5% (prev. 1.0%). Fiscal 2027 median forecast 0.7% (prev. 0.8%). Fiscal 2028 median forecast 0.8%. Core CPI. Fiscal 2026 median forecast 2.8% (prev. 1.9%). Fiscal 2027 median forecast 2.3% (prev. 2.0%). Fiscal 2028 median forecast 2.0%. Dissenters (voted for 25bps hike).

- BoJ’s Takata: price stability target had been more or less achieved and that risks to prices in Japan were already skewed to the upside due to the second-round effects of price rises stemming from overseas developments.

- BoJ’s Tamura: Considering that, with risks to prices becoming significantly skewed to the upside, the bank should set the policy interest rate as close to the neutral rate as possible.

- BoJ's Nakagawa: Risks to prices skewed to the upside under accommodative financial conditions. Monetary policy Will scrutinise timing, pace of policy adjustment with a close eye on economic and price impact from the Middle East developments.

- Japanese Economy Minister Kiuchi will attend the BoJ policy meeting, hopes the BoJ communicates and coordinate policy closely with the government and work towards sustainably achieving a 2% inflation target.

- ECB BLS: Banks tightened credit standards across all loan categories, driven by higher perceived risks and lower risk tolerance. Banks tightened credit standards across all loan categories, driven by higher perceived risks and lower risk tolerance. Banks expect to also tighten credit standards in the second quarter, influenced by geopolitical tensions, energy developments, and higher funding costs. Loan demand from firms and households expected to decrease, resulting from reduced financing for fixed investments, lower consumer confidence, and decreased spending on durables. Nearly half of euro area banks use securitisation to grant new loans, manage credit risk and enhance liquidity and funding, relying on non-bank financial entities to purchase securitised loans.

- PBoC guided banks to increase lending in April, according to sources.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian drones attack Russia's Tuapse oil refinery, causing a fire, according to authorities.

CRYPTO

- Bitcoin is a little lower this morning and trades just below USD 77k whilst Ethereum holds around USD 2.2k.

APAC TRADE

- Asia-Pac stocks traded broadly weaker, as risk sentiment weakened amid reports that US President Trump is unlikely to agree to Iran’s proposal.

- ASX 200 started the session on the backfoot, and held onto its earlier losses. Sectors were broadly in the red, as Utilities underperformed while Energy was supported by higher crude prices.

- Nikkei 225 opened flat but fell lower, a move which was later exacerbated after the hawkish hold by the BoJ. The Bank upgraded inflation outlook and downgraded growth, with FY27 growth only modestly cut. The index fell back towards the 60,000 handle. For single stock stories, DENSO reported earning in which all metrics rose annually, but the Co. cut its FY net and op. profit guidance while stating its withdrawal of the proposal of Rohn acquisition.

- KOSPI was the outperformer, with LG Electronics among those that lifted the index after reports that the Co.’s CEO is to meet Nvidia CEO Huang’s daughter to discuss strategic cooperation.

- Hang Seng and Shanghai Comp. followed the broadly negative bias. CATL’s HK shares were under pressure after the Co.’s announcement of a plan to raise over HKD 39bln in private share placement to step up expansion in its renewables business.

NOTABLE ASIA-PAC HEADLINES

- China State owned refiners have begun applying for government permits that would allow them to resume fuel exports in May, Bloomberg reported.

NOTABLE APAC DATA RECAP

- Hong Kong Balance of Trade (Mar) -89.1B (Prev. -64.2B).

- Hong Kong Imports YoY (Mar) Y/Y 41.2% (Prev. 29.9%).

- Hong Kong Exports YoY (Mar) Y/Y 35.8% (Prev. 24.7%).

- Japanese Unemployment Rate (Mar) 2.7% vs. Exp. 2.6% (Prev. 2.6%, Low. 2.6%, High. 2.7%).

- Japanese Jobs/applications ratio (Mar) 1.18 vs. Exp. 1.18 (Prev. 1.19, Low. 1.18, High. 1.20).