Published: 29 Apr 2026, 06:15 UTC

Newsquawk Desk

EU Market Open: Europe set for modestly firmer open after a slew of earnings, USD and Brent firm a touch on WSJ report

0:00--:--

- Trump has told officials to prepare for an extended blockade of Iran, WSJ; Trump said they are doing very well in the Middle East.

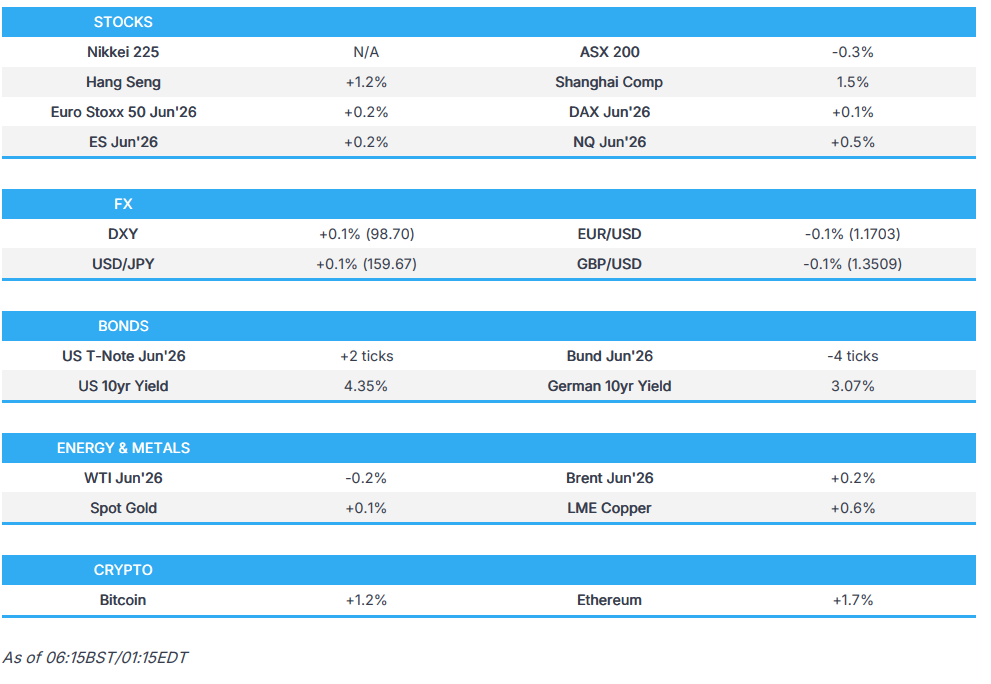

- APAC equity performance incrementally improved across the session, with outperformance in the Hang Seng & Shanghai Composite.

- USD rangebound, lifted briefly on the WSJ report. Peers are broadly contained into the Fed.

- Fixed income was hit on the WSJ report, but has since retraced the move.

- Energy benchmarks jumped on the blockade update, but the move was relatively short-lived. Precious metals contained, base peers followed China higher.

- Looking ahead, highlights include Spanish HICP (Apr), German State/Nationwide HICP (Apr), EZ Economic Sentiment (Apr), US Durable Goods (Mar), US Housing Starts (Feb/Mar), Wholesale Inventories (Mar), Fed/BoC/BCB Policy Announcements (Apr), Speakers include BoC’s Macklem & Fed Chair Powell, Supply from Italy & Germany.

- Earnings from Microsoft, Amazon.com, Meta, Alphabet, Ford, Qualcomm, Carvana, SoFi, Humana, Novartis, TotalEnergies, Iberdrola, GSK, Lloyds, Deutsche Bank, Mercedes-Benz, Adidas & Porsche AG.

- Click for the Newsquawk Week Ahead.

IRAN CONFLICT

- US President Trump tells officials to prepare for an extended blockade of Iran, WSJ reported citing sources. Sources went on to say that Trump has opted to continue squeezing Iran's economy, as other options would carry more risk than maintaining the blockade.

- US intelligence agencies are examining how Iran would react to US President Trump declaring victory in the war, according to Reuters citing sources.

- US President Trump said we are doing very well in the Middle East. He added that King Charles agreed that Iran cannot have a nuclear bomb.

- US President Trump said Germany's Chancellor Merz thinks it's ok for Iran to have a nuclear weapon and he doesn't know what he's talking about.

- US has issued new Iran related sanctions, targeting 35 Iranian entities and individuals for aiding sanctions evasion.

- IRGC said that new means of power ready against any new US attack.

- A political aide to the IRGC said that we will respond to any new aggression with surprises and new capabilities and will burn America's giant ships at sea if they miscalculate again.

- Satellite imagery showed ships departing Iran being redirected by the US Navy blockade.

- The Israeli army carried out a massive bombing operation east of Gaza City.

- An Israeli army commander said that we are not talking about destroying terrorist infrastructure in southern Lebanon, but rather destroying everything, according to Haaretz.

- Israel's Hayom newspaper estimates that Israel may accept a limited ceasefire with Lebanon, with the stipulation of the disbandment of Hezbollah, Al Hadath reported.

US TRADE

EQUITIES

- US stocks finished lower as risk tone soured, with Technology the clear sectoral laggard as AI-infrastructure exposed names were hit hard after WSJ reported that OpenAI missed targets, which stoked data centre spending concerns. Overall, sectors closed mixed, with Energy the clear gainer, followed by Consumer Staples, as the former was supported by strength in crude benchmarks, given that the lack of progress between the US and Iran outweighed the UAE exiting OPEC and OPEC+.

- SPX -0.49% at 7,139, NDX -1.01% at 27,029, DJI -0.05% at 49,142, RUT -1.15% at 2,756.

CENTRAL BANKS

- RBNZ Governor Breman said the global environment continues to present headwinds and that Q1 core inflation have remained stable within the 1-3% target band.

NOTABLE HEADLINES

- US has ordered numerous chip equipment companies to halt tool shipments to two facilities of Hua Hong (688347 CH), China's second largest chipmaker, according to sources.

- Amazon (AMZN) AWS CEO said the co. is working hard to add more capacity for OpenAI with AI chip, power, capacity demand outpacing supply.

- The White House is developing guidance to allow agencies to get around Anthropic's supply chain risk designation and onboard Mythos, Axios reported citing sources.

- The White House held a closed-door meeting with technology and cyber companies to discuss concerns about Anthropic's Mythos model, Politico reported citing sources.

- US President Trump's budget office sent a memo urging House Republicans to agree to partly reopen DHS, even without new cash for immigration enforcement, CNN reported citing sources.

APAC TRADE

EQUITIES

- Asia-Pac stocks initially opened with a slight negative bias, amid the tech-led selloff stateside and the lack of progress between US and Iran. Sentiment improved throughout the APAC session, despite light newsflow.

- ASX 200 underperformed, with Health Care and Miners weighing on the index. Woodside Energy reported Q1 revenue that rose annually and maintained its FY guidance, helping support shares just shy of 2% gains.

- KOSPI reversed earlier losses, as the index shrugged off the tech-led selloff in US equities.

- Hang Seng and Shanghai Comp. outperformed, following a flurry of earnings and updates. For BYD, the Co. reported revenue that beat estimates, however net income fell annually. On the other hand, Hua Hong Semiconductor slipped after the US reportedly ordered numerous chip equipment companies to halt tool shipments to two of the co.’s facilities.

- US equity futures traded higher, albeit modestly after rebounding from the selloff following the WSJ report. The initial positiveness came following a batch of positive earnings after-hours, including Seagate, in which Q3 EPS and revenue beat estimates.

- European equity futures are indicative of a muted open with the Euro Stoxx 50 future U/C after cash closed -0.5% on Tuesday.

FX

- DXY oscillated in a tight 98.57-98.68 range. Modest upticks were seen amid the WSJ report, in which Trump told officials to prepare for an extended blockade. However, the move was completely pared back in the hour following the headline. Coming up, the FOMC rate decision at 14:00EDT/19:00BST. With the rate widely expected to remain at 3.50-3.75%, focus will squarely be on Chair Powell’s guidance.

- EUR/USD continued to hold above the 1.1700 handle, heading into a flurry of inflation metrics out of Spain and Germany.

- GBP/USD found acceptance above the 1.3500 handle, despite the political turmoil. UK lawmakers voted against holding an inquiry into whether the PM misled parliament over the Mandelson appointment. In the near term, politics will remain front and centre as the May 7th local elections approaches.

- USD/JPY rotated in a tight 159.49-159.67 range, with Japan on holiday for Showa Day.

- Antipodeans underperformed, with the kiwi hit slightly harder. Australian inflation printed cooler-than-expected, which spurred AUD/USD to slip below 0.71700, but price action remains choppy. Commentary by Australia’s Treasurer Chalmers post-CPI stated that an inflation peak is expected at higher levels; however, this failed to spur a reaction.

FIXED INCOME

- UST Futures rotated in a 110-24+ to 110-30 range. Downside came amid the WSJ report, in which it cited US officials stating that Trump has told aides to prepare for an extended Hormuz blockade; the move since completely pared. Looking ahead, the Fed is to deliver its March policy decision, in which it is widely expected to be kept unchanged at 3.50-3.75%.

- Bund Futures held a 124.92-125.13 range, trading either side of the 125 handle. The brief downside following the WSJ report was quickly pared back, as 10yr yields held below 3.1%. German HICP is expected at 13:00BST, in which the Y/Y figure is expected to rise to 3.1% (prev. 2.8%) while the M/M figure is expected at 0.8% (prev. 1.2%).

- JGB Futures returned to the post-BoJ reaction low at the latter end of Tuesday’s trade and oscillated in a narrow 129.52-129.72 range.

- US sells USD 44bln of 7yr notes; Tail 0.5bps.

COMMODITIES

- Crude futures started the APAC session in a muted manner, with energy prices grinding lower in a tight USD 1/bbl range. As the session continued, volumes picked up and prices surged higher, with WTI briefly regaining the USD 100/bbl handle before completely reversing the move. The bid came following a WSJ report, citing sources, stating that US President Trump has told officials to prepare for an extended blockade of Hormuz, a less risky option compared to resuming strikes or walking away.

- Precious Metals lacked a clear directional bias, as spot gold rotated either side of the USD 4600/oz handle (USD 4576-4610/oz range).

- 3M LME Copper traded on the front foot, continuing to pare back Tuesday’s losses, as positive sentiment in Chinese equities supported the red metal.

- US Private Energy Inventories (bbls): Crude -1.8mln (exp +0.3mln), Distillate -2.6mln (exp. -2.3mln), Gasoline -8.5mln (exp. -2.1mln), Cushing -0.8mln.

- China set May refined fuel exports to regions, ex. Hong Kong, at 500k metric tonnes, according to sources. May fuel exports double April's shipments but remains below pre-Iran war levels.

- China's Steel Association said China's apparent crude steel consumption fell 4.4% Y/Y in Q1'26

CRYPTO

- Bitcoin regains the USD 77k handle.

NOTABLE ASIA-PAC HEADLINES

- China has paused new autonomous driving permits after Baidu (9888 HK/BIDU) outage.

DATA RECAP

- Australian Inflation Rate MoM (Mar) M/M 1.1% vs. Exp. 1.3% (Prev. 0.0%, Low. 0.9%, High. 1.6%).

- Australian Inflation Rate YoY (Mar) Y/Y 4.6% vs. Exp. 4.7% (Prev. 3.7%).

- Australian Quarterly Inflation Rate QoQ (Q1) Q/Q 1.4% vs. Exp. 1.4% (Prev. 0.6%, Low. 1.1%, High. 1.6%).

- Australian RBA Weighted Median CPI MoM (Mar) M/M 0.8% (Prev. 0.2%).

- Australian RBA Weighted Median CPI YoY (Mar) Y/Y 3.5% (Prev. 3.5%).

- Australian RBA Trimmed Mean CPI MoM (Mar) M/M 0.3% (Prev. 0.2%).

- Australian RBA Trimmed Mean CPI YoY (Mar) Y/Y 3.3% (Prev. 3.3%).

GEOPOLITICS

RUSSIA-UKRAINE

- Russian President Putin said Ukraine is intensifying attacks on Russian civilian targets, with the latest example being an attack on the Tuapse.

OTHER

- US Senate voted 51-47 to block Cuba military action resolution.

EU/UK

NOTABLE HEADLINES

- NIESR lowered the UK's 2026 growth forecast to 0.9% (prev. 1.4%) and raises its inflation forecast to 4.7% (prev. 3.3%) at the start of 2027; the BoE may have to respond with big rate hikes if energy disruption is prolonged.

- Ukraine is facing risk of tougher terms to get some EU loan payouts, Bloomberg reported citing sources. Payouts would be dependent on the introduction of a tax change for businesses

- European lawmakers failed to reach a deal on watered-down landmark AI rules after 12 hours of negotiations. Talks are to resume next month.

- EU Parliament called for new EU revenue sources, including a digital tax, a levy on online gambling, and a tax on profits from crypto transactions.

- UK lawmakers voted against holding inquiry into whether UK PM Starmer misled parliament over Mandelson appointment.