Published: 29 Apr 2026, 10:20 UTC

Newsquawk Desk

US Market Open: Crude benchmarks climb, Equites firm on NXPI earnings, Fed/BoC/BCB, AMZN, GOOG, META, MSFT ahead

0:00--:--

- Trump has told officials to prepare for an extended blockade of Iran, WSJ; Trump said they are doing very well in the Middle East.

- An update that lifted energy briefly overnight and while the move pared into the European morning, benchmarks are at fresh highs with WTI peaking just below USD 104/bbl.

- The fresh energy highs have weighed on fixed, though only modestly pre-FOMC and with brief EGB respite on German state CPIs.

- USD lifts into the likely final Fed as Chair for Powell, AUD lags post-CPI, EUR briefly hit by German state CPI

- Energy advances weigh on equity sentiment, numerous mega-cap earnings ahead, including AMZN, GOOG, META, MSFT & QCOM

- Looking ahead, highlights include US Durable Goods (Mar), US Housing Starts (Feb/Mar), Wholesale Inventories (Mar), Fed/BoC/BCB Policy Announcements (Apr), Speakers include BoC’s Macklem & Fed Chair Powell.

EUROPEAN TRADE

IRAN

- US President Trump tells officials to prepare for an extended blockade of Iran, WSJ reported citing sources; Trump has opted to continue squeezing Iran's economy, as other options would carry more risk than maintaining the blockade.

- US President Trump posted "Iran can’t get their act together. They don’t know how to sign a nonnuclear deal. They better get smart soon! President DJT". Post also includes an image of President Trump holding a rifle, with explosions behind him; caption reads "NO MORE MR. NICE GUY!".

- US President Trump said we are doing very well in the Middle East, King Charles agrees that Iran cannot have a nuclear bomb.

- Iran's Vice Chairman of the National Security Council Boroujerdi said, on negotiations, that Ghalibaf "personally manages" them.

- Iran has pushed back on statements from the US regarding pipeline explosions, ISNA reports.

- Senior Pakistani official said mediation continues, working to narrow the gap between the US and Iran.

- US Treasury Secretary Bessent said the US Treasury has targeted Iran's financial infrastructure, disrupting tens of billions of dollars in Iranian revenue; Kharg Island is approaching maximum storage capacity, forcing Iran to reduce oil production.

- The Israeli army carries out a massive bombing operation east of Gaza City.

- IRGC said that new means of power ready against any new US attack, Press TV reported.

- Israel's Hayom newspaper estimates that Israel may accept a limited ceasefire with Lebanon, with the stipulation of the disbandment of Hezbollah, Al Hadath reported.

- An Israeli army commander said that we are not talking about destroying terrorist infrastructure in southern Lebanon, but rather destroying everything, according to Haaretz.

- A political aide to the IRGC said that we will respond to any new aggression with surprises and new capabilities, will burn America's giant ships at sea if they miscalculate again, Al Jazeera Mubasher reported.

- Japanese PM Takaichi said Japan will engage with Iran for safe passage of ships.

- US Treasury has frozen USD 344mln in crypto linked to Iran, according to Fox Business citing officials.

EQUITIES

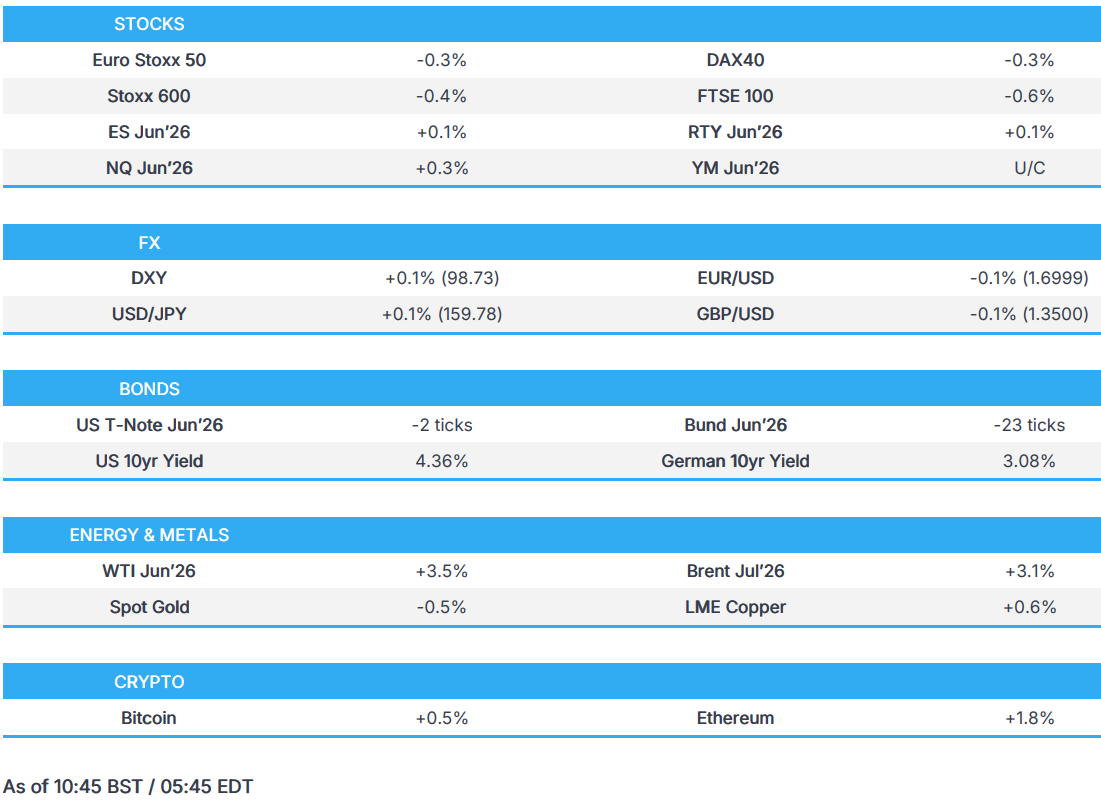

- European bourses (STOXX 600 -0.4%) began the session on a weaker footing as geopolitical headlines dictate the tape with WSJ reporting "Trump told officials to prepare for an extended blockade of Iran" and the US President posting this morning, "Iran can’t get their act together. They don’t know how to sign a non-nuclear deal. They better get smart soon! President DJT".

- European sectors opened mixed, though they now show a negative bias as the index dipped lower. Energy tops the pile, and Tech also does well after NXP Semi's Q1 beat-and-raise after hours; Insurance and Retail lag. In terms of key movers: Adidas (+7%, Strong Q1, raised guidance) and UBS (+4%, NII, Top and bottom line beat, share buyback).

- US equity futures are mostly flat, NQ outperforms after NXP earnings, the name is higher by some 16% in the premarket. In other stories, Visa +4.5% in pre-market trading after it reported a Q2 beat, while Meta’s Instagram and Facebook were found to have breached the EU's digital services rules in a preliminary investigation. Earnings are ahead for MSFT, AMZN, META, GOOG, and QCOM after hours.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY continues to outperform most G10 peers as the preferred hedge against higher oil prices. Many catalysts will dictate the path forward for the Greenback, FOMC and BoC today, then the BoE and ECB on Thursday.

- DXY remains supported by both the 100 and 200 DMAs at the 98.50 mark as crude benchmarks rise into a packed session. In addition to the Fed meeting, the Senate Banking Committee is expected to advance Kevin Warsh’s nomination as Fed Chair; the vote is set for 10:00EDT/15:00BST.

- A quick preview into the Fed, the Bank is widely expected to leave rates unchanged, with focus squarely on Chair Powell’s guidance as policymakers assess the inflationary impact of the ongoing US-Iran conflict. The recent surge in oil prices has pushed back rate cut expectations, with a Reuters poll showing a majority of economists now see easing delayed until at least September. Traders also seek details about Powell’s future, with this meeting expected to be his last as Fed Chair, providing Kevin Warsh is approved in time.

- EUR is also lower against the Buck but fares better than peers despite German state CPIs being indicative of a cooler mainland series. EUR remains supported by the 1.17 mark, and ING writes this morning, "Tomorrow’s ECB meeting should, in our view, largely meet market expectations.", aside from geopols, the next catalyst for the EUR will be the Fed meeting today.

- Antipodeans are the worst performers in the G10 space by a large margin after Aussie inflation for March was softer than expected and trimmed bets for hikes in Next week's RBA meeting. ING writes "The pullback in AUD looks mostly a function of stretched positioning rather than a real rethink of RBA expectations.

FIXED INCOME

- A modestly bearish start in fixed benchmarks, given continued upside in the energy complex. Gains for energy occurring in recent trade despite a lack of fresh driver, and potentially as participants take another look at the WSJ reporting around a prolonged Hormuz closure, as while this is less risky than strikes, it does suggest a further extension of the ongoing supply disruption.

- Amidst this, fixed benchmarks are at lows. USTs to a 110-24+ base, but with downside of just a few ticks as we await the FOMC. The Fed is expected to maintain its rate in a 3.50-3.75% band, with focus on the guidance from Chair Powell in what may be his last meeting as Chair. As a reminder, the Senate Banking Committee is today expected to advance the nomination of Warsh to the broader Senate.

- Bunds are also at lows, down to 110-24+ with downside of a few ticks at most. Fleeting upside seen in EGBs as the initial German State CPIs are indicative of a cooler mainland series than the consensus for the 13:00BST mainland series suggests. Bunds spiked higher from 124.95 to 125.07, shy of the earlier 125.16 high. Albeit, the move swiftly pared and Bunds are back at lows.

- Gilts gapped lower by nine ticks, and have since slipped another 14 to an 86.54 trough. Action a function of the above, with Gilts trading broadly in-line with peers this morning. On the UK specifically, PM Starmer was not referred to the Privileges Committee. However, the number of Labour MPs who defied the whip and those who abstained without a clear reason is indicative of a moderate rebellion, not one sufficient to yet hit the threshold to trigger a leadership contest, but nonetheless an ominous sign into the May 7th local elections and further Mandelson-related communication releases in the weeks ahead.

- Italy sold EUR 5.5bln vs exp. EUR 4.5-5.5bln 3.15% 2031, 3.35% 2035 BTP and EUR 3.5bln vs exp. EUR 3.0-3.5bln 2036 CCTeu.

- Germany sold EUR 3.8bln vs exp. EUR 5bln 2.90% 2036 Bund: b/c 1.15x (prev. 1.24x), average yield 3.08% (prev. 2.92%), retention 23.3% (prev. 23.66%)

COMMODITIES

- WTI and Brent began the European morning with very mild gains, and have continued to extend higher. WTI Jun'26 topped the USD 102/bbl mark, to make a peak at USD 102.78/bbl (vs trough of USD 98.42/bbl); Brent Jul'26 resides near peaks at USD 106.16/bbl, which also marks the WTD high.

- Focus remains on the US-Iran situation, which, as it stands, does not appear to be moving towards peace. A WSJ article overnight, citing sources, suggested that President Trump told officials to prepare for an extended blockade of Iran, attempting to squeeze Iran’s economy. This will ultimately guide traders to price in the possibility of long-term disruptions to energy, and hence explains the strength in energy this morning.

- Most recently, President Trump posted on Truth Social that “Iran can’t get their act together. They don’t know how to sign a non-nuclear deal. They better get smart soon!”. Alongside this, an AI image of himself holding a rifle, with explosions behind him, the accompanying caption read "NO MORE MR. NICE GUY!". A post which spurred about a bucks worth of upside in the complex.

- Spot gold is a touch lower this morning and currently resides towards the lower end of a USD 4,568-4,610/oz range. As has been the case, the yellow metal has been subdued by the stronger USD and inflationary implications of the war in Iran. Today’s focus will be on the Fed Policy Announcement, which is widely expected to leave rates unchanged at 3.50-3.75%, with focus squarely on Chair Powellʼs guidance, as policymakers assess the inflationary impact of the ongoing US-Iran conflict.

- Base metals are mixed; 3M LME Aluminium is a touch firmer this morning, alongside strength in 3M LME Copper, whilst Palladium and Nickel move lower. 3M LME Copper holds above the USD 13k/t mark, within a USD 13,026-13,155.93/t range. Copper has advanced as Chinese fabs replenished stockpiles ahead of the Labor Day holiday, with restocking supporting prices and some buyers viewing recent declines on global growth concerns as an opportunity.

- "More UAE accounts on X teasing another big announcement today", Bloomberg's Bercetche reported.

- UAE's Fujairah port oil inventories have fallen further to 6mln barrels.

- EU Commission President von der Leyen said stronger EU coordination is required on fuel reserves.

- Kazakhstan's Energy Minister said they have no intention to leave OPEC.

- Indian government issues draft rules to increase ethanol blending in petrol.

- China set May refined fuel exports to regions, ex. Hong Kong, at 500k metric tonnes, according to sources; May fuel exports double April's shipments but remains below pre-Iran war levels.

- China's Steel Association said China's apparent crude steel consumption fell 4.4% Y/Y in Q1'26.

- US Private Energy Inventories (bbls): Crude -1.8mln (exp +0.3mln), Distillate -2.6mln (exp. -2.3mln), Gasoline -8.5mln (exp. -2.1mln), Cushing -0.8mln.

TRADE/TARIFFS

- European lawmakers failed to reach a deal on watered-down landmark AI rules after 12 hours of negotiations, talks to resume next month.

- US Secretary of State Rubio expresses deep concerned by China's targeted economic pressure after the Barboa and Cristobal terminals decision.

NOTABLE EUROPEAN HEADLINES

- NIESR lowers the UK's 2026 growth forecast to 0.9% (prev. 1.4%) and raises its inflation forecast to 4.7% (prev. 3.3%) at the start of 2027; the BoE may have to respond with big rate hikes if energy disruption is prolonged. The UK would face recession and inflation of 5% in a more adverse scenario in which oil prices spike to around USD 140/bbl and Hormuz remains closed. The Middle East shock will also worsen the UK’s public finances. Relative to the OBR's outlook, debt-servicing costs are likely to be higher, growth weaker, and pressure greater for additional support to compensate vulnerable households.

- UK Chancellor Reeves said the Government needs to make targeted interventions that will not have a lasting impact on interest rates.

NOTABLE EUROPEAN DATA RECAP

- German State CPIs were indicative of a cooler mainland series than consensus for the 13:00BST mainland series suggests.

- EU Consumer Confidence Final (Apr) -20.6 vs. Exp. -20.6 (Prev. -16.3).

- EU Economic Sentiment (Apr) 93.0 vs. Exp. 95.5 (Prev. 96.6).

- EU Services Sentiment (Apr) 0.9 (Prev. 4.9).

- EU Industrial Sentiment (Apr) -7.7 vs. Exp. -8 (Prev. -7.0).

- EU Selling Price Expectations (Apr) 31.1 (Prev. 19.7).

- Italian Consumer Confidence (Apr) 90.8 (Prev. 92.6).

- Italian Business Confidence (Apr) 87.9 (Prev. 88.8).

- Spanish HICP Flash (Apr): 3.5% Y/Y (prev. 3.4%); Core 3.1% Y/Y (prev. 2.8%); M/M 0.7% (prev. 1.7%).

- Spanish Inflation Rate MoM Prel (Apr) M/M 0.4% (Prev. 1.2%).

- Spanish Inflation Rate YoY Prel (Apr) Y/Y 3.2% vs. Exp. 3.6% (Prev. 3.4%); Core 2.8% (prev. 2.9%).

- Spanish Core Inflation Rate YoY Prel (Apr) Y/Y 2.8% (Prev. 2.9%).

- Swedish Consumer Confidence (Apr) 91.5 (Prev. 95.2).

- Swedish Consumer Inflation Expectations (Apr) 6.8% (Prev. 7.3%).

- Swedish Business Confidence (Apr) 103.3 (Prev. 102.3).

- Swedish Household Lending Growth YoY (Mar) Y/Y 3.1% (Prev. 3%).

- Swedish GDP Growth Rate YoY Flash (Q1) Y/Y 1.6% (Prev. 2.1%).

- Swedish GDP Growth Rate QoQ Flash (Q1) Q/Q -0.2% (Prev. 0.5%).

- Swedish GDP MoM (Mar) M/M 1.9% (Prev. 0%).

- Swedish Retail Sales MoM (Mar) M/M 3.1% (Prev. -0.6%).

- Swedish Retail Sales YoY (Mar) Y/Y 6.2% (Prev. 2.4%).

NOTABLE EUROPEAN EQUITY HEADLINES

- AstraZeneca (AZN LN) Q1 2026 (USD): Revenue 15.3bln (exp. 14.9bln), adj. EPS 2.58 (exp. 2.55). Confirms guidance for FY26. "...remain on track to achieve our ambition for 2030 and beyond.".

- GSK (GSK LN) Q1 2026 (GBP) Adj. EPS 46.5p (exp. 43.2p), Turnover 7.63bln (prev. 7.51bln Y/Y), Gross Profit 1.87bln (prev. 1.93bln Y/Y); reaffirms 2026 guidance.

- Santander (SAN SM) - Q1 2026 (EUR): NII 5.46bln (exp. 4.97bln), EPS 0.36 (exp. 0.26), Total income 15.1bln (exp. 15bln), Net income 5.5bln (exp. 5.0bln), reaffirms 2026-28 targets. Net Loan provisions 3.23bln (exp. 3.17bln).

- UBS (UBSG SW) - Q1 2026 (USD): Revenue 14.2bln (exp. 13.2bln), Net income 3.04bln (exp. 2.42bln), confident in 2026 financial targets. Announces share buyback of up to USD 3bln by its Q2 results, aiming to do more by year-end.

CENTRAL BANKS

- RBNZ Governor Breman said the global environment continues to present headwinds, Q1 core inflation have remained stable within the 1-3% target band.

- PBoC set USD/CNY mid-point at 6.8608 vs exp. 6.8347 (prev. 6.8589).

- Banxico Governor Rodriguez said the Bank is close to finishing its rate cutting cycle that began in 2024.

NOTABLE US HEADLINES

- KPMG has closed its US government audit practice following the loss of an army contract, FT reported.

- US President Trump's budget office sent a memo urging House Republicans to agree to partly reopen DHS, even without new cash for immigration enforcement, CNN reported citing sources.

- Australia's Treasurer Chalmers said the Treasury expects inflation to peak at higher levels.

- The White House is developing guidance to allow agencies to get around Anthropic's supply chain risk designation and onboard Mythos, Axios reported citing sources.

- New Zealand Treasury said the economy is in a fragile spot due to the rise in fuel prices.

- US President Trump is to nominate McMaster for the Treasury Financial Markets position.

- US Senate votes 51-47 to block Cuba military action resolution.

- The White House is to hold a closed-door meeting with technology and cyber companies to discuss concerns about Anthropic's Mythos model, Politico reported citing sources. Meeting to include policy heads from Microsoft (MSFT), Red Hat, Amazon (AMZN), Google (GOOGL), Crowdstrike (CRWD), Palo Alto (PANW), Goldman Sachs (GS) and JPMorgan (JPM).

GEOPOLITICS

RUSSIA-UKRAINE

- Ukraine is facing risk of tougher terms to get some EU loan payouts, Bloomberg reported citing sources; payouts would be dependent on the introduction of a tax change for businesses.

CRYPTO

- Bitcoin is a little firmer and trades just shy of USD 77k, with Ethereum also extending higher to USD 2.3k.

APAC TRADE

- Asia-Pac stocks initially opened with a slight negative bias, amid the tech-led selloff stateside and the lack of progress between US and Iran. Sentiment improved throughout the APAC session, despite light newsflow.

- ASX 200 underperformed, with Health Care and Miners weighing on the index. Woodside Energy reported Q1 revenue that rose annually and maintained its FY guidance, helping support shares just shy of 2% gains.

- KOSPI reversed earlier losses, as the index shrugged off the tech-led selloff in US equities.

- Hang Seng and Shanghai Comp. outperformed, following a flurry of earnings and updates. For BYD, the Co. reported revenue that beat estimates, however net income fell annually. On the other hand, Hua Hong Semiconductor slipped after the US reportedly ordered numerous chip equipment companies to halt tool shipments to two of the co.’s facilities.

NOTABLE APAC DATA RECAP

- Australian Quarterly Inflation Rate QoQ (Q1) Q/Q 1.4% vs. Exp. 1.4% (Prev. 0.6%, Low. 1.1%, High. 1.6%).

- Australian RBA Weighted Median CPI YoY (Mar) Y/Y 3.5% (Prev. 3.5%).

- Australian RBA Trimmed Mean CPI YoY (Mar) Y/Y 3.3% (Prev. 3.3%).

- Australian RBA Weighted Median CPI MoM (Mar) M/M 0.8% (Prev. 0.2%).

- Australian Quarterly RBA Trimmed Mean CPI QoQ (Q1) Q/Q 0.8% (Prev. 0.9%).

- Australian Quarterly RBA Trimmed Mean CPI YoY (Q1) Y/Y 3.5% (Prev. 3.4%).

- Australian Quarterly Inflation Rate YoY (Q1) Y/Y 4.1% vs. Exp. 4.1% (Prev. 3.6%).

- Australian Inflation Rate MoM (Mar) M/M 1.1% vs. Exp. 1.3% (Prev. 0.0%, Low. 0.9%, High. 1.6%).

- Australian Inflation Rate YoY (Mar) Y/Y 4.6% vs. Exp. 4.7% (Prev. 3.7%).