Published: 30 Apr 2026, 10:25 UTC

Newsquawk Desk

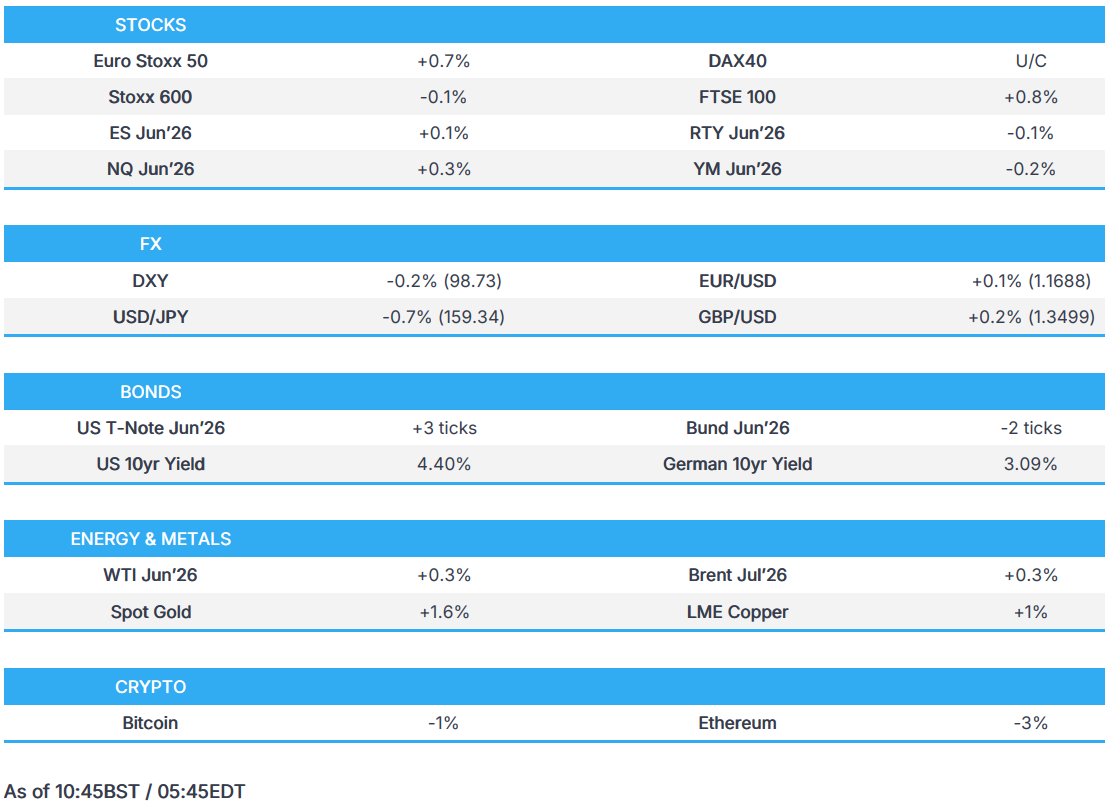

US Market Open: USD/JPY pressured after Katayama/Mimura verbal intervention, NQ outperforms after tech earnings

- US CENTCOM is to brief US President Trump on new plans for potential military action in Iran on Thursday, Axios reported, citing sources. The plan includes a short and powerful strike, potentially targeting infrastructure to break the nuclear issue deadlock.

- The Axios report initially lifted the crude complex, but contracts have recently slipped towards lows, lacking a clear driver.

- Pakistan's Foreign Ministry says channels of dialogue with officials in Washington and Tehran remain open, Al Hadath reports.

- European bourses are broadly lower, but have clambered off worst levels.

- US equity futures are flat/incrementally firmer. In pre-market trade; Qualcomm (+11%), Google (+5.9%), Amazon (+2%) are all higher after earnings, whilst Microsoft (-1.8%) and Meta (-7.8%), extend lower.

- DXY is under pressure, USD/JPY sinks below the 160.00 mark after FinMin Katayama warned that they are “nearing” the time to take bold FX steps.

- Fixed benchmarks hold a slight bearish bias, but off worst levels heading into the ECB and BoE.

- Looking ahead, highlights include US PCE Price Index (Q1/Mar), US GDP Growth Rate (Q1), Jobless Claims (Apr/25), US Chicago PMI (Apr), ECB Policy Announcement (Apr), BoE Policy Announcement & MPR (Apr), CBRT Minutes (Apr). Speakers include BoE Governor Bailey and ECB President Lagarde.

EUROPEAN TRADE

MIDDLE EAST

- US CENTCOM is to brief US President Trump on new plans for potential military action in Iran on Thursday, Axios reported citing sources; plan includes a short and powerful strike potentially targeting infrastructure to break the nuclear issue deadlock. Other options expected to be presented include a plan to take over part of the Strait to allow for commercial shipping, which could involve ground forces, and a special forces op to secure Iran's uranium stockpile.

- US CENTCOM has asked to send the Army's hypersonic missile to the Middle East for possible use against Iran, Bloomberg reported citing sources.

- US CENTCOM said the US navy has redirected 42 vessels from the blockade in the Strait of Hormuz and that the military is fully committed to enforcing the blockade.

- US President Trump told Israeli PM Netanyahu that Israel should only take surgical military action in Lebanon and avoid a full resumption of the war, Axios reported.

- US Treasury Secretary Bessent said sprinting for the finish line with Iran, according to Fox Business; willing to do secondary sanctions on Iran oil buyers. Every day adding more economic pressure to Iran. Close to half a billion in Iran-related crypto seized. Consumers and stock market are looking through Iran. UAE and others have requested swap lines, swap lines are not a bailout.

- Iran lawmaker Mottaki says a naval blockade would amount to a declaration of war, and that fighters could decide as soon as tomorrow or next week to remove such obstacles via military action.

- Iran’s Navy Commander said the Islamic Republic will soon unveil a new weapon that would deeply terrify the enemy, IRNA reported. He said Iran has closed the strategic Strait of Hormuz from the Arabian Sea. Condemned the US’s illegal seizure of several Iranian vessels as part of the blockade, which he said amounted not only to “piracy” but also “hostage-taking".

- Iran's Navy commander warns that Iran will soon face its enemies with a very dreadful weapon that will strike fear into their hearts, according to Press TV.

- Pakistan's Foreign Ministry said channels of dialogue with officials in Washington and Tehran remain open, Al Hadath reported. "“The clock on diplomacy has snit stopped. We remain hopeful for a negotiated settlement on this issue. We will continue with our sincerest efforts”,.

- China's Military said they conducted combat readiness patrols near Scarborough Shoal, according to a statement.

- "No point" in negotiating over zero enrichment, Iranian lawmaker said, Al Jazeera reported; adding “I have no objection to going to the negotiating table, but we should have looked more closely at how to proceed”.

- The US administration is asking countries to join a new international coalition that would enable ships to navigate through the Strait of Hormuz, WSJ reported. The Maritime Freedom Construct would be a US-led coalition that would share information, coordinate diplomatically and enforce sanctions.

- A surveillance drone near the US embassy in Baghdad has been shot down, according to Iraqi security sources.

- Iranian Navy Commander said we have closed the Strait of Hormuz from the Arabian sea side and will take swift action if enemy advances, Al Araby reported.

EQUITIES

- European bourses (STOXX 600 -0.2%) started the session broadly in the red, but have attempted to move higher as the morning progressed; currently towards highs. From an index standpoint, the FTSE 100 (+0.5%) and the AEX (+0.5%) lead, whilst the FTSE MIB (-0.5%) lags. Initial downbeat sentiment stemmed from an Axios report which suggested that the US CENTCOM is to brief President Trump about military options in Iran on Thursday. Ahead, focus will be on the ECB and BoE policy announcements, where both are expected to stand pat on rates, but focus will be on any hawkish guidance. (Previews in the Research Suite)

- European sectors initially held a negative bias, but are now mixed. Basic Resources took the top spot, buoyed by strength in gold prices and after Glencore (+2%) reported a 19% jump in copper output. Utilities takes the second spot, led higher by United Utilities (+10%) after strong results and announcing an equity raise to fund a multi-billion dollar investment plan. Media is found at the foot of the pile, joined closely by Autos; the latter has been driven lower by Stellantis (-7.4%), where shares have slumped on a tariff-adjusted miss.

- US equity futures are flat/incrementally firmer, but contracts are holding an upward bias, following European peers higher. There were several key US earnings reports published after-hours, in brief; Qualcomm (+11), Google (+5.9%), Amazon (+2%) are all higher after earnings, whilst Microsoft (-1.8%) and Meta (-7.8%), extend lower.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10 FX are mostly stronger against the Buck after DXY fell on remarks from Japanese Finance Minister who said "getting closer to taking decisive steps in FX", and Mimura, the top FX diplomat, said "This is the final warning before FX action". This strong commentary saw USD/JPY fall 80 pips on Katayama, then a further 30+ ticks on Mimura's remarks.

- USD/JPY, as mentioned, trades higher by around 0.6% as commentary from both officials proved more hawkish than previous verbal intervention attempts which failed to propel the JPY.

- EUR/USD trades a touch below the 1.17 mark in choppy trade, with the FOMC and decent JPY moves failing to knock the single currency ahead of the ECB meeting. Full preview in the Newsquawk research suite. This morning, EZ inflation ticked up from the prior but broadly in line with expectations. There was no real reaction from the series, which sticks to the narrative that price pressures remain broadly confined to the headline measures, with the core figures steady or actually moderating from the last reading. On Energy, that lifted to 10.9% (prev. 5.1%) and remains the primary contributor to the headline rate.

- EUR/GBP is also unchanged into the BoE and MPR, where it is expected to hold rates in a 9-0 vote split, with risks towards a dovish and/or hawkish dissent a possibility. Focus will be on any clues or hints towards the timing of the next move, and the MPC’s current view on market pricing. In terms of UK Politics, The Times reported that Former deputy PM Rayner is said to be weighing up mounting a direct challenge for the leadership after next week's local elections. Rayner is regarded as the most left-wing candidate, and also the bookies' favourite.

- Japanese Finance Minister Katayama says timing to take decisive action is near; "we are getting closer to taking decisive steps in FX"; have long mentioned possible bold action on FX; monitoring FX while on holiday.

- Japanese Top Currency Diplomat Mimura says this is the final warning before action is taken; speculative moves in FX are mounting; getting closer to taking decisive steps; seeing speculative activity in FX market.

- US will reportedly seek forfeiture of Iran-linked oil tankers seized at sea.

FIXED INCOME

- Overall, a contained session for fixed benchmarks. USTs lifted off overnight 110-07+ lows across the European morning, up to an 110-15+ high but with gains of just a few ticks at most. Action that comes as the space eases off the hawkish lows delivered after the Fed and Powell (recap on the board).

- Ahead, the US is focused on PCE, consensus chimes with the guidance from Chair Powell last night. Recent pricing data has shown that energy was the primary driver, with the core offering some relative relief as such. Though, PCE-related PPI components suggest service pressures remain sticky. Policy implications would be in line with the direction of the series, though a cooler print would likely provide only temporary relief given the clear signs of persistent price pressures elsewhere.

- Bunds in the red, though only by c. 5 ticks. Got to a 110-07 base before rebounding a touch, though only as high as 124.75, where it was briefly flat. EZ Flash HICP sparked no real reaction, sticks to the narrative that price pressures remain broadly confined to the headline measures. Ahead, the ECB is expected to maintain rates, a decision merited by the relatively limited amount of data, no overt signs of second-round effects and uncertainty on the duration of the shock and degree of pass-through.

- Gilts gapped lower by 29 ticks and then slipped another five to an 85.90 low, an open that took out Wednesday's 85.98 base and notched a fresh contract low. Amidst this, the UK 10yr yield got to a 5.09% peak, nearing but not testing the recent 23rd March peak at 5.12%. Ahead, attention on the BoE, where a hold is expected, and while 9-0 is technically the base case , dissent on both the dovish and hawkish side of things is very possible. Overall, we are mainly after hints from the MPC itself, and the individual statements and press conference around the timing of the next move, though neither the statement nor Bailey are likely to be that explicit at this stage. Gilts are currently incrementally in the green, amidst a recent bout of pressure in the energy space.

- Japan sold JPY 2.8tln 2-year JGBs: Average yield 1.407%, b/c 5.24x, price tail 0bps.

- China allocates CNY 91.5bln in special bonds for equipment upgrades.

COMMODITIES

- In geopolitics, US CENTCOM is set to brief President Trump on new military options for Iran, including potential strikes, Hormuz intervention, and uranium seizure operations, according to Axios. Meanwhile, the US blockade remains the core strategy, with Trump calling it “genius” and refusing to lift it without a nuclear deal. Elsewhere, Iran is threatening “unprecedented military action” if the blockade continues, while economic pressure is intensifying internally. The US is pushing to form a global maritime coalition to restore shipping through the Strait of Hormuz. On this note, US CENTCOM Commander Adm. Brad Cooper will brief Trump on Thursday on new Iran military plans, with Joint Chiefs Chairman Gen. Dan Caine also attending, according to Axios.

- WTI June and Brent July futures are firmer as de-escalation efforts between US and Iran seem futile, with neither side publicly willing to move on demand. WTI resides in a USD 106.39-110.93/bbl range and Brent in a USD 109.63-114.70/bbl parameter. Do note that a bout of pressure was seen in the crude complex, taking contracts towards lows - a move which lacked a clear driver. Dutch TTF holds a mild upward bias and found some resistance at EUR 49/MWh before waning to near EUR 47/MWh.

- Spot gold and silver are firmer as the DXY falls on recent JPY strength following the “final warning” from Japan’s Top currency diplomat with regards to JPY intervention, with Japanese Finance Minister Katayama earlier sparking JPY strength as she said the timing to take decisive action is near – which comes ahead of the Japanese market holidays between May 3rd-6th. Spot gold has topped yesterday’s high to trade in a current USD 4,539-4,629/oz.

- Base metals are also benefiting from the softer USD coupled with above-forecast Chinese RatingDog and NBS Manufacturing PMIs. 3M LME copper resides in a 12,977.97- 13,120.35/t range at the time of writing.

- California gasoline price tops USD 6/gallon for first time since 2023, Bloomberg reported.

- IEA's Birol said oil prices over USD 120/bbl is putting a lot of pressure on many countries.

- Oman crude OSP calculated at USD 104.73/bbl for June (prev. USD 124.05/bbl in May).

- Japanese Prime Minister Takaichi reportedly to announce naphtha supply secured "until the new year", Nikkei reported.

- Russia's Novak said OPEC+ to evaluate possibilities to supply global oil market at May 3 meeting, IFX reported.

- China reportedly to allow state refiners to export some fuels to Asia buyers.

- Fire at Russia's Tuapse oil refinery has been extinguished, regional Governor said.

- Russia's Deputy PM Novak said UAE exit does not mean a price war, reiterates there are no plans to leave OPEC+, IFX reported. OPEC+ will continue working together.

- The Japanese Government is considering reviving power and gas subsidies this summer, according to sources; Plan is to use reserve funds and no extra budget eyed for now.

- The Iranian oil minister has urged the public to reduce energy consumption, while dismissing the impact of the US naval blockade, CNN reported; the government has instructed government offices to cut electricity use by up to 70%.

- Iran's delegation to the UN said its enriched uranium is under the full supervision of the IAEA.

- Indonesia set May Crude Palm Oil reference price at USD 1,049/mt.

- US National Emergency Dominance Council Director Agun is set to travel to Venezuela on Thursday for meetings with oil, gas and mining execs.

- Fire at PDVSA's Cardon refinery's FCC unit is reportedly under control.

NOTABLE EUROPEAN HEADLINES

- POLITICO, citing UK Officials, said May 8 looks set to be a moment of real danger for the PM; said a long-time critic promised to go public with a call for PM Starmer to step down if results are as bad as expected.

- US President Trump posted that the US is studying and reviewing the possible reduction of troops in Germany with a determination to be made over a short period of time.

NOTABLE EUROPEAN DATA RECAP

- EU Super Core Inflation Rate YoY Flash (Apr) Y/Y 2.2% vs. Exp. 2.1% (Prev. 2.3%); Core 2.1% vs exp. 2.3% (prev. 2.2%).

- EU GDP Growth Rate YoY Flash (Q1) Y/Y 0.8% vs. Exp. 0.8% (Prev. 1.2%).

- EU Inflation Rate MoM Flash (Apr) M/M 1% (Prev. 1.3%).

- EU GDP Growth Rate QoQ Flash (Q1) Q/Q 0.1% vs. Exp. 0.2% (Prev. 0.2%).

- EU Inflation Rate YoY Flash (Apr) Y/Y 3.0% vs. Exp. 2.9% (Prev. 2.6%); Services 3.0% (prev. 3.2%).

- EU Unemployment Rate (Mar) 6.2% vs. Exp. 6.2% (Prev. 6.2%).

- Italian Inflation Rate MoM Prel (Apr) M/M 1.2% vs. Exp. 0.6% (Prev. 0.5%).

- Italian Inflation Rate YoY Prel (Apr) Y/Y 2.8% (Prev. 1.7%).

- Italian Unemployment Rate (Mar) 5.2% vs. Exp. 5.3% (Prev. 5.3%).

- Italian GDP Growth Rate QoQ Adv (Q1) Q/Q 0.2% vs. Exp. 0.1% (Prev. 0.3%).

- Italian GDP Growth Rate YoY Adv (Q1) Y/Y 0.8% (Prev. 0.8%).

- German GDP Growth Rate QoQ Flash (Q1) Q/Q 0.3% vs. Exp. 0.2% (Prev. 0.3%).

- German GDP Growth Rate YoY Flash (Q1) Y/Y 0.3% (Prev. 0.4%).

- German Unemployment Rate (Apr) 6.4% vs. Exp. 6.3% (Prev. 6.3%).

- German Unemployed Persons (Apr) 3.006M (Prev. 2.977M).

- German Unemployment Change (Apr) 20K vs. Exp. 5K (Prev. 0K).

- German Import Prices MoM (Mar) M/M 3.6% vs. Exp. 3.3% (Prev. 0.3%).

- German Retail Sales MoM (Mar) M/M -2.0% vs. Exp. -0.6% (Prev. -0.6%).

- German Retail Sales YoY (Mar) Y/Y -2.0% (Prev. 0.7%).

- German Import Prices YoY (Mar) Y/Y 2.3% (Prev. -2.3%).

- Spanish GDP Growth Rate QoQ Flash (Q1) Q/Q 0.6% vs. Exp. 0.5% (Prev. 0.8%).

- Spanish GDP Growth Rate YoY Flash (Q1) Y/Y 2.7% (Prev. 2.7%).

- French PPI YoY (Mar) Y/Y 0.20% (Prev. -2.4%).

- French PPI MoM (Mar) M/M 2.0% (Prev. -0.2%).

- French prelim. HICP (Apr): 2.5% Y/Y vs exp. 2.3% (prev. 2.0%); 1.2% M/M vs exp. 0.9% (prev. 1.1%).

- French Inflation Rate MoM Prel (Apr) M/M 1% vs. Exp. 1% (Prev. 1%).

- French Inflation Rate YoY Prel (Apr) Y/Y 2.2% (Prev. 1.7%). Insee "The increase in inflation should again be driven by the sharp acceleration in energy prices (+14.2% over a year after +7.4% in March), in particular those of petroleum products.".

- French Private Non Farm Payrolls QoQ Prel (Q1) Q/Q -0.1% (Prev. -0.1%).

- French Household Consumption MoM (Mar) M/M 0.7% vs. Exp. 0.7% (Prev. -1.4%).

- French GDP Growth Rate YoY Prel (Q1) Y/Y 1.1% (Prev. 1.2%).

- French GDP Growth Rate QoQ Prel (Q1) Q/Q 0.0% vs. Exp. 0.2% (Prev. 0.2%).

NOTABLE EUROPEAN EQUITY HEADLINES

- Unilever (ULVR LN) Q1 2026 Trading Statement: Underlying Sales +3.8% (exp. 3.7%); FY26 outlook unchanged with USG at lower end of 4-6% and modest margin improvement expected.

- Glencore (GLEN LN) Q1 Production Report: Maintains FY production guidance; Copper production 199.6kt (prev. 167.9kt Y/Y), Cobalt 5.8kt (prev. 9.5kt Y/Y), Zinc 176.9kt (prev. 213.6kt Y/Y), Nickel 17.2kt (prev. 18.8kt Y/Y), Gold 68koz (prev. 145koz Y/Y).

CENTRAL BANKS

- Morgan Stanley expects the Fed to leave rates unchanged in 2026 (prev. forecasted cuts in Sep and Dec), expects 25bps of rate cuts each in Jan'27 and Mar'27.

- US President Trump posted that Jerome "Too Late" Powell wants to stay at the Fed because he can't get a job anywhere else.

- US Treasury Secretary Bessent said it is highly unusual for Powell to stay on the Fed board, calling it an insult and violation of norms; adds Warsh will be Fed Chair on time.

- BoJ maintains May outright bond buying operations at the same levels as April.

- BoJ Outlook Report: weak JPY pushes up prices for a wide range of good services, thereby giving a bigger boost to core consumer inflation; impact of a weak JPY shock is bigger than that of oil shock. "...while a yen depreciation shock tends to lead to a rise in the GDP deflator through wage increases and greater profit margins, an increased crude oil price shock tends to cause a decline in the GDP deflator through compressed profit margins and wages, reflecting worsened trading gains...In the current phase, it is possible that both shocks could occur at the same time...".

- The BoE has raised concerns over plans to cut the capital requirements of specialist trading firms, the FT reported; BoE officials are worried they could increase financial stability risks by making firms less able to withstand a crisis.

- The RBNZ is to release details on how the MPC members vote, making the votes publicly available when a consensus is not reached.

- PBoC set USD/CNY mid-point at 6.8628 vs exp. 6.8414 (prev. 6.8608).

- NBH Governor Varga said that the forint gains have helped the Bank reach its inflation target.

- BoK official said that we act if needed to stabilise financial markets and monitor the Middle East conflict.

- BCB cuts 25bps to 14.50%, as expected; decision was unanimous and it affirms serenity and caution in the conduct of monetary policy.

NOTABLE US HEADLINES

- US House has approved a Republican plan making way for a USD 70bln bill for ICE and Border Patrol.

- The White House opposes Anthropic's plan to expand access to Mythos due to national security concerns and worries about computing power, WSJ reported citing sources.

- US Senators are to introduce legislation to tighten ban on Chinese vehicles.

- The US House has passed a three-year extension of the FISA re-authorisation.

GEOPOLITICS

RUSSIA-UKRAINE

- Russia's Novak said OPEC+ to evaluate possibilities to supply global oil market at May 3 meeting, IFX reported.

- Ukrainian President Zelensky said Ukraine is to seek clarification from the US, on details of Russia's ceasefire proposal; Ukraine's proposal is a long term ceasefire.

- Fire at Russia's Tuapse oil refinery has been extinguished, regional Governor said.

- Russia's Deputy PM Novak said UAE exit does not mean a price war, reiterates there are no plans to leave OPEC+, IFX reported. OPEC+ will continue working together.

- The EU is preparing a package of short-term benefits for Ukraine, which would include greater market access and deeper participation in EU programmes, Politico reported citing diplomats.

CRYPTO

- Bitcoin is a little lower this morning and trades around USD 76k, whilst Ethereum underperforms and hovers around USD 2.2k.

APAC TRADE

- Asia-Pac stocks traded with a negative bias, as weakness stateside in cash hours, earnings and recent geopolitical updates drive price action. More recently, Axios reported that US CENTCOM is to brief President Trump on new plans for potential military action, which is to include a short and powerful strike to break the nuclear issue deadlock.

- ASX 200 printed modest losses. IT and Tech topped the sector pile while consumer staples and mining underperformed.

- Nikkei 225 returned from holiday closure with losses in excess of 1%, returning to the 59,000 handle. Fujitsu weighed on the index after the Co.’s Q4 op. profit and FY forecast missed estimates. On the other hand, TDK was one of the outperformers, following FY net that rose by around 20%.

- KOSPI lacked direction, trading either side of the unchanged mark. Initial upside came after Samsung Electronics reported Q1 earnings that beat top- and bottom-line metrics. However, the earlier gains were erased as trade continued. LG Electronics held onto its earlier gains, after the Co. reported Q1 net that beat expectations.

- Hang Seng and Shanghai Comp. traded mixed, with the Hang Seng the clear underperformer. Stronger-than-expected manufacturing PMIs failed to support the indices, while China Construction Bank printed losses following its Q2 earnings.

NOTABLE ASIA-PAC HEADLINES

- Japanese Top Currency Diplomat Mimura said this is the final warning before action is taken; speculative moves in FX are mounting; getting closer to taking decisive steps; seeing speculative activity in FX market.

- South Korea to launch 24hr USD/KRW trade from end-June.

NOTABLE APAC DATA RECAP

- Japanese Consumer Confidence (Apr) 32.2 vs. Exp. 33.1 (Prev. 33.3).

- Japanese Industrial Production MoM Prel (Mar) M/M -0.5% vs. Exp. 1.1% (Prev. -2.0%).

- Japanese Industrial Production YoY Prel (Mar) Y/Y 2.3% (Prev. 0.4%).

- Japanese Retail Sales MoM (Mar) M/M 1.3% (Prev. -2.0%).

- Japanese Retail Sales YoY (Mar) Y/Y 1.7% vs. Exp. 0.8% (Prev. -0.2%).

- Chinese RatingDog Manufacturing PMI (Apr) M/M 52.2 vs exp. 50.9 (prev. 50.8).

- Chinese NBS General PMI (Apr) 50.1 (Prev. 50.5).

- Chinese NBS Manufacturing PMI (Apr) 50.3 vs. Exp. 50.2 (Prev. 50.4).

- Chinese NBS Non-Manufacturing PMI (Apr) 49.4 vs. Exp. 49.9 (Prev. 50.1).

- Australian Export Prices QoQ (Q1) Q/Q 0.5% (Prev. 3.2%).

- Australian Import Prices QoQ (Q1) Q/Q 0.1% vs. Exp. -0.6% (Prev. 0.9%).

- Australian Private Sector Credit YoY (Mar) Y/Y 8.1% (Prev. 7.8%).

- Australian Private Sector Credit MoM (Mar) M/M 0.7% vs. Exp. 0.6% (Prev. 0.6%).

- Australian Housing Credit MoM (Mar) M/M 0.6% (Prev. 0.6%).