Published: 1 May 2026, 09:45 UTC

Newsquawk Desk

US Market Open: JPY breaches Thursday low in potential further intervention, bourses in thin trade amid holiday, US futures lacklustre

0:00--:--

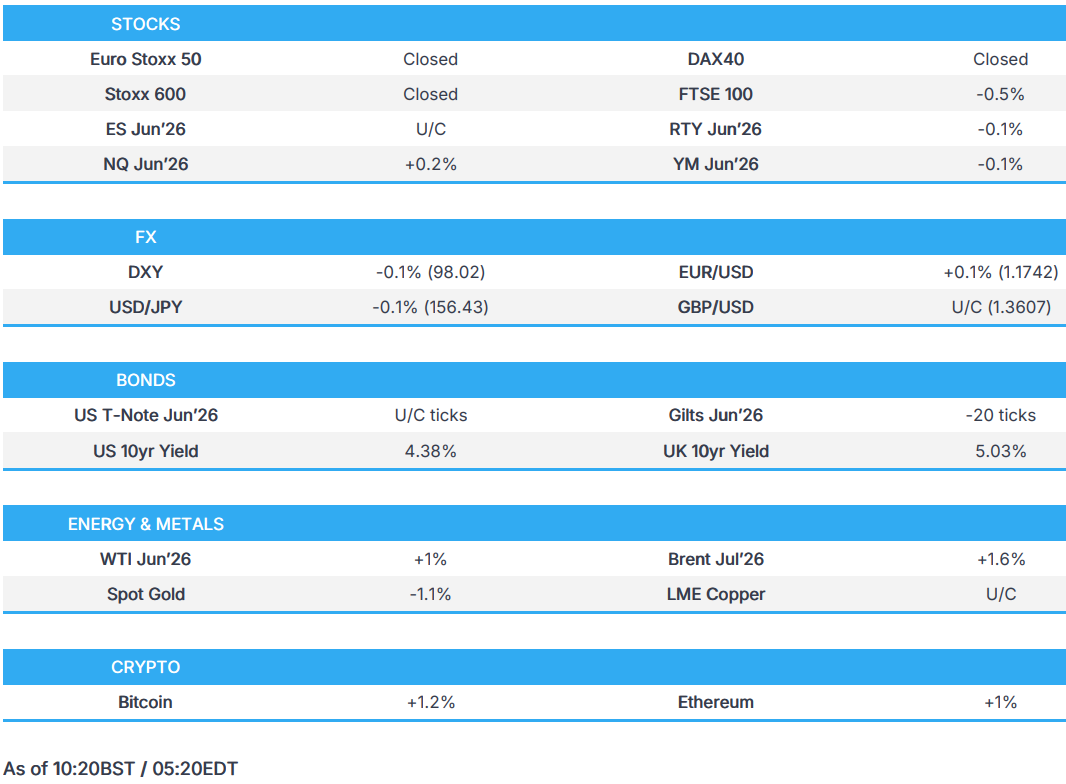

- Conditions in Europe thin amid Labour Day, FTSE 100 dragged by NatWest and AstraZeneca.

- US equity futures are modestly mixed. Apple (+2.8%) gains after strong results, driven by iPhone sales; SanDisk (-6.1%) dips despite a strong Q3 report.

- DXY is a touch lower; USD/JPY sank to a 155 handle, potentially on intervention.

- Fixed income futures are contained in limited conditions, with US data ahead.

- Crude futures remain elevated heading into another weekend of geopolitical risk.

- Looking ahead, highlights include US ISM Manufacturing (Apr), Speakers include BoE's Pill, Earnings from Chevron, Colgate, Exxon, Moderna, Estee Lauder.

- Holiday: Labour Day (Eurozone cash and derivatives closed).

EUROPEAN TRADE

IRAN

- US President Trump is expected to make a decision on the path forward [on Iran] in the coming days, NBC reported citing a US official.

- US President Trump said would not have approved enriched Uranium for Iran; needs guarantees Iran will not have a nuclear weapon ever. Hormuz blockade is 100% effective.

- A senior Trump administration official said that for War Power Resolution purposes, hostilities that began on February 28th have been terminated.

- Iranian Judiciary head said Iran does not accept negotiation based on imposition; adds Iran has never left the negotiating table, Iranian press reported.

- Iranian National Security Commission member Rezei said "we are currently in the second phase of the war with the enemy..the naval blockade is a continuation of the war.. we are not in a ceasefire situation now", Mehr reported. Full post:"Iran cannot be besieged; We have different ways to export and import In a conversation with Mehr, Ebrahim Rezaei said: "The enemy has turned to our naval blockade after failing in the military war and direct confrontation, and we are currently in the second phase of the war with the enemy." In other words, the naval blockade is a continuation of the war that the Americans have started against us. So, we are not in a ceasefire situation now. A member of the National Security Commission of the Majlis, stating that the Americans do not have the operational capacity to blockade Iran by sea, said: "Our only access route for transit is not through the Persian Gulf and the Strait of Hormuz.".

- US CENTCOM Commander Cooper briefed President Trump for 45 minutes on new operational plans for potential strikes against Iran, Axios' Ravid reported citing sources.

- Iranian Foreign Ministry Spokesperson said that it is not responsible to expect a quick conclusion of the negotiations and that the other party has not used the opportunity provided by Iran's proposal, must be ready for any eventuality. The US and Israeli regime are famous for breaking their promises and the biggest guarantee for not repeating the war is the power of Iran.

- Drone attack hits Iranian Kurdish opposition camp east of Iraq's Erbil, according to Reuters, citing security sources. via vv.

- The defense sound heard over Tehran is related to countering micro-birds and reconnaissance drones, via Tasnim.

- Air defence sounds are being heard in some areas of Tehran but reasons are unclear, Mehr News reported.

EQUITIES

- Eurozone cash and derivatives are closed today in observance of Labour Day.

- FTSE 100 (-0.6%) is lower this morning, dragged lower by the likes of NatWest (-4.2%), AstraZeneca (-2%) and pressure across the mining names. Delving into the UK bank in a bit more detail, the Co. reported strong headline metrics and lifted its income guidance for the year, whilst reaffirming other components. Despite the upbeat Q1, shares find themselves in the red; some will point towards the 1.4% decline in interest income. As for AstraZeneca, shares have dropped after the US FDA voted against the co’s breast cancer drug.

- US equity futures traverse on either side of the unchanged mark. In pre-market trade, Apple (+2.8%) gains after it reported an earnings and revenue beat, driven by strong iPhone and services sales, better-than-expected China revenue, upbeat revenue guidance, and signs the company is managing through higher memory costs and supply constraints. Sandisk (-6.1%) moves lower, despite beating earnings, revenue and guidance, with reports suggesting that expectations were already extremely elevated after a huge rise in its shares.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- USD/JPY took another leg lower this morning, surpassing Thursday’s low of 155.55 to mark a session trough of 155.48.

- Thursday saw strong verbal intervention from Japanese Finance Minister Katayama, then later comments from top FX official Mimura, which pushed the pair lower in excess of 2%. Later in the session on Thursday, Nikkei sources said a Japanese government official confirmed the intervention to Nikkei, but we are still awaiting official confirmation, with Mimura declining to comment on intervention speculation, and figures showing potential FX intervention due late May. Some desks noted the remarks/potential intervention on Thursday may have had a follow-through to the downside in Brent prices as Mimura's "looking at markets on all fronts" could have been viewed as having cross-asset implications. However, there was no move in the Brent Jul'26 contract this morning.

- Though it is impossible to say whether intervention occurred in this morning’s 150pip+ move, 7:45 am BST (3:45 pm JST) marks the low-liquidity period and the final hour of the Tokyo trading session, a European holiday, and also month-end. Factors which provide a relatively low liquidity environment, which boost the effectiveness of intervention.

- In terms of the move this morning, USD/JPY fell 156 pips from 157.05 to a low of 155.48, half of the move has now been pared as participants continue to price the still low real rates in Japan, and the potential for energy prices to remain high, which MUFG says will see USD/JPY rebound quickly.

- DXY was resilient to JPY moves, with the index falling briefly below the 98.00 mark, then paring most of the move. DXY will likely attempt to return to 100 and 200 DMAs either side of 98.50, which it has mostly respected throughout the week.

- BoJ data for April 30th shows FX intervention of some JPY 5.4tln.

FIXED INCOME

- Fixed benchmarks are flat amid mass market closures with liquidity thin and the docket sparse.

- USTs in a narrow 110-17+ to 110-22+ range, awaiting Final Manufacturing PMI and then the ISM Manufacturing figure thereafter. Today's docket also has Fed's Miran; reminder, as Powell has indicated he will remain at the Fed once he is no longer Chair, Miran will likely vacate his spot for Warsh.

- Gilts gapped lower by 15 ticks and then slipped to an 86.36 low, though comfortably above Thursday's 85.90 contract base. No move to the Final Manufacturing PMI, which unsurprisingly points to marked price pressures and frontloading of purchase activity.

- Ahead, BoE Chief Economist Pill is due; Pill was the sole hawkish dissenter in April, and sees the risk of second round effects as being to the upside vs the three scenarios, calling for a "prompt but modest hike" to "help mitigate upside risks to price stability".

- Japan sold JPY 250bln 10-year I/L JGBs: b/c 3.40x, Yield at the Lowest Accepted Price 0.578%.

- Australia sold AUD 1.0bln 4.50% 2033 bond: b/c 3.56x, average yield 4.8608%.

COMMODITIES

- In geopolitics, the Trump administration is framing hostilities with Iran as “terminated” under the War Powers Resolution due to a ceasefire, allowing it to bypass the 60-day congressional approval requirement despite ongoing tensions and historically weak enforcement of the law. Trump’s stance remains inconsistent—he alternates between suggesting a deal with Iran may or may not be necessary while firmly maintaining that Iran must never acquire nuclear weapons—and he has indicated that Iran’s military capabilities are significantly degraded, though the ceasefire’s durability is uncertain. Meanwhile, CENTCOM has already presented detailed strike options, with a decision on next steps expected within days. Diplomatically, talks are stalled: Iran signals slow progress, internal disagreements are emerging within its leadership over negotiation strategy, and external actors like Israel anticipate a collapse in talks, potentially triggering escalation, including possible strikes on Iranian energy infrastructure. Iran, for its part, is preparing for “any eventuality,” adopting a defiant posture, reinforcing defences, and continuing limited military responses.

- Crude prices remain elevated with WTI Jun between USD 104.13-106.65/bbl and Brent July towards the middle of a USD 110.33-112.45/bbl range at the time of writing. Price action this morning has been fairly muted amid broad market closures in APAC and Europe, due to the Labour Day holiday. Unlike Thursday, oil was unreactive this morning to JPY strength. (See FX for details)

- Spot gold and silver are softer as higher crude prices keep the precious metals space pressured, with little action seen from a slide in the DXY amid a sudden surge in the JPY around 0745BST. Spot gold resides within yesterday’s USD 4,539-4,647.05/oz.

- Base metals are mixed with 3M LME copper flat within a narrow USD 13,008.53-13,121.88/t range amid little impetus as Chinese markets were closed overnight and a large part of Europe is away.

- US President Trump's mineral reserve reportedly plans to purchase rare earths from China.

- White House said presidential permit authorizes bridger pipeline expansion to construct, connect, operate, and maintain pipeline facilities at boundary at Phillips County, Montana, between US and Canada. Permitee granted permission to transport between the United States and Canada crude oil and petroleum products.

TRADE/TARIFFS

- Japanese PM Takaichi said she will be visiting Vietnam and Australia. "Moreover, through these visits to both countries, taking into account the current situation in the Middle East, I will confirm cooperation on strengthening supply chain resilience, including stable energy supply and critical minerals within the Asian region. I believe such initiatives are also important for procuring critical supplies such as crude oil and petroleum products in Japan.".

- USTR Greer said he suggested a US-China Board of Trade in his meeting with Chinese VP He Lifeng.

- USTR Greer said the US will extend preferential treatment to other UK goods.

NOTABLE EUROPEAN DATA RECAP

- UK M4 Money Supply MoM (Mar) M/M 0.8% vs. Exp. 0.5% (Prev. 0.6%).

- UK Net Lending to Individuals MoM (Mar) M/M 8B vs. Exp. 5.9B (Prev. 6.8B).

- UK BoE Consumer Credit (Mar) 1.895B (Prev. 1.935B).

- UK Mortgage Approvals (Mar) 63.53K vs. Exp. 60K (Prev. 62.58K).

- UK Mortgage Lending (Mar) 6.15B (Prev. 4.84B).

- UK S&P Global Manufacturing PMI Final (Apr) 53.7 vs. Exp. 53.6 (Prev. 51.0).

- UK Nationwide Housing Prices YoY (Apr) Y/Y 3.0% (Prev. 2.2%).

- UK Nationwide Housing Prices MoM (Apr) M/M 0.4% vs. Exp. -0.3% (Prev. 0.9%).

CENTRAL BANKS

- ECB's Kocher said it is too early to see second round inflation effects.

- ECB's Nagel said it is more appropriate for the ECB to respond in June if the outlook does not improve markedly.

- ECB's Muller said it is increasingly likely that the ECB needs to raise rates; there are already signs that rising energy prices are being passed on.

NOTABLE US HEADLINES

- US President Trump has signed the DHS funding bill.

GEOPOLITICS

RUSSIA-UKRAINE

- Local governor said port infrastructure in Ukraine's Odesa region was damaged and wounded two people.

- Ukrainian forces have reportedly launched another attack on Russia's Tuapse oil refinery causing a fire, according to the Kyiv Independent.

- Ukrainian Envoy to Japan tells Reuters that Ukraine is seeking supply of military equipment from Japan after the easing of weapons-exports rules.

OTHERS

- China's Foreign Minister said the Taiwan issue is the biggest risk in US relations, urges US Secretary of State Rubio to maintain the stability of bilateral relations.

CRYPTO

- Bitcoin is firmer this morning by around 1.5% and trades just above USD 77k, with Ethereum also moving a little higher and towards USD 2.3k.

APAC TRADE

- Asia-Pac stocks traded with decent gains, helped by the positivity seen stateside. The majority of markets are closed today for Labour Day.

- ASX 200 rebounded after 8 straight days of losses. Miners led gains while Energy underperformed following Thursday’s drop in oil prices. ANZ reported cash profit that beat estimates; however shares have slipped lower after it raised its coverage ratio by 4bps due to the heightened geopolitical risk.

- Nikkei 225 posted decent gains, despite the sudden JPY strength amid intervention talk. Tokyo Electron benefited following its positive Q4 results, in which net profit beat estimates.

NOTABLE ASIA-PAC HEADLINES

- Japan's Top Diplomat Mimura said will not comment on FX.

NOTABLE APAC DATA RECAP

- Australian PPI QoQ (Q1) Q/Q 0.4% vs. Exp. 1.5% (Prev. 0.8%).

- Australian PPI YoY (Q1) Y/Y 3.0% (Prev. 3.5%).

- Australian S&P Global Manufacturing PMI Final (Apr) 51.3 (Prev. 49.8).

- Japanese S&P Global Manufacturing PMI Final (Apr) 55.1 vs. Exp. 54.9 (Prev. 51.6).

- Japanese Stock Investment by Foreigners (Apr/25) 807.9B (prev. 2380.6B).

- Japanese Foreign Stock Investment (Apr/25) 41.2B (prev. 338.3B).

- Japanese Bond Investment by Foreigners (Apr/25) -786.9B (prev. -294.7B).

- Japanese Foreign Bond Investment (Apr/25) -887.7B (prev. -8.8B).

- Japanese Tokyo Core CPI YoY (Apr) Y/Y 1.5% vs. Exp. 1.8% (Prev. 1.7%).

- Japanese Tokyo CPI Ex Food and Energy YoY (Apr) Y/Y 1.9% vs. Exp. 2.3% (Prev. 2.3%).

- Japanese Tokyo CPI YoY (Apr) Y/Y 1.5% vs. Exp. 1.6% (Prev. 1.4%).

- New Zealand Building Permits MoM (Mar) M/M -1.3% (Prev. 2.7%).

- New Zealand ANZ Roy Morgan Consumer Confidence (Apr) 80.3 (Prev. 91.3).