Published: 6 May 2026, 10:25 UTC

Newsquawk Desk

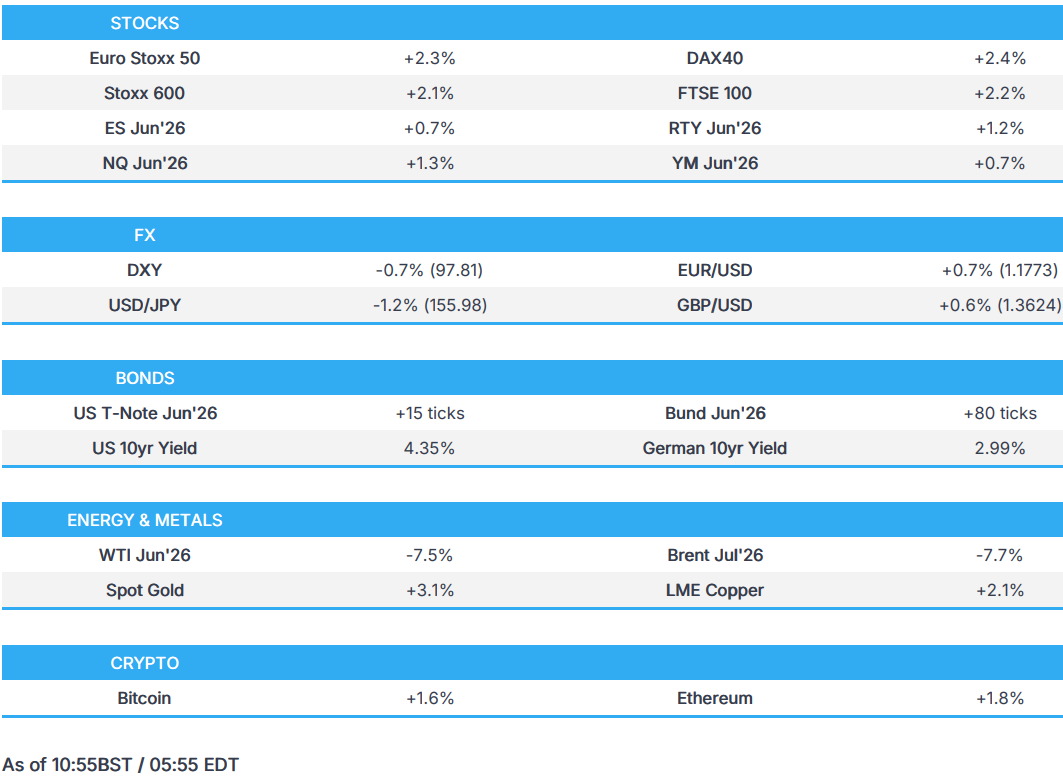

US Market Open: US and Iran reportedly close to an MoU to end the war, Axios reports; crude hit, stocks at highs

0:00--:--

- Crude & USD dented, equities & fixed bid after Trump paused Project Freedom and more recently as Axios reports that the US & Iran are closing in on an MOU to end the conflict.

- Brent below USD 101.50/bbl, ES +0.7%, DAX 40 +2.5%, EUR/USD above 1.1770, Bunds firmer by over 80 ticks.

- JPY was likely the subject of intervention overnight, falling from 157.00 to a 155.03 low, but has since rebounded back towards the 156.00 mark.

- NQ +1.3%, outperforming as AMD surges +19% as data centre growth drives a beat.

- Israeli security/military officials reportedly believe negotiations are a waste of time, and conveyed to the US a desire to resume attacks on Iran.

- Looking ahead, highlights include Canadian Ivey PMI (Apr), US ADP Employment (Apr), US Treasury Refunding Announcement, NBP Policy Announcement, Speakers include Fed’s Goolsbee, Musalem, BoC's Macklem & Rogers.

IRANIAN CONFLICT

Axios report which touts MoU between US-Iran:

- A Pakistani source has confirmed that the US and Iran are closing in on a one-page memorandum to end their conflict, Reuters reports.

- US and Iran are reportedly closing in on one-page memo to end war, Axios reported citing officials; White House believes it is close to an agreement to end the war and establish a framework for detailed nuclear negotiations.

- MoU details, as it stands: Declare an end to the war in the region and the start of a 30-day period of negotiations, which could occur in Geneva or Islamabad. Iran committing to a moratorium on nuclear enrichment (at least 12-15 years). US agreeing to lift sanctions and release billions in frozen Iranian funds. Both sides lifting restrictions through the Strait of Hormuz, to occur gradually during the 30-day negotiation.

- If talks collapsed, US forces could restore the blockade or resume military action.

- Uranium Component: The duration of the moratorium is being actively negotiated. Sources suggest at least 12yrs and one suggesting 15yrs is likely; Iran sought five, the US wanted 20. Suggested that Iran would agree to its highly enriched uranium being removed from Iran, potentially to the US.

- Timeline: Iran is expected to respond within 48 hours. While nothing has been agreed upon, sources indicate this is the closest the parties have been to a deal since the war began.

- Issues: Some US officials remain sceptical that even an initial deal will be reached. Fractures within the Iranian leadership.

OTHER:

- US President Trump posted that Project Freedom will be paused for a short period to see whether or not the agreement with Iran can be finalised and signed, blockade will remain in full effect.

- Journalist Mallick posted "...i would not be surprised if there is an incoming Iranian proposal to Washington via Islamabad, soon.". Full post:"As what I understand, while the ball largely lies in Iranian court when it comes to US - Iran negotiations, i would not be surprised if there is an incoming Iranian proposal to Washington via Islamabad, soon.".

- Iranian and Saudi Arabian Foreign Ministers held a phone call; stressed continuing diplomacy and prevent escalation of tensions.

- Iranian President Pezeshkian said US demands from Iran are impossible and unattainable.

- US Secretary of State Rubio spoke with Russia's Foreign Minister Lavrov, in which the US-Russia relationship, Russia-Ukraine war and Iran was discussed.

- Iranian Foreign Ministry Spokesperson denies the UAE's accusation that Iran fired missiles and drones at it, stating that Iran's defensive actions were exclusively directed at the US, according to a statement. UAE is cooperating with the US and Israel against Iran.

- Israeli Ambassador said relations with the UAE are growing.

- IRGC denies any involvement with the attacks on the UAE earlier in the week.

- Pakistan's PM thanks the US President for pausing Project Freedom, in response to a request from Pakistan and Saudi Arabia, among others.

- "Iraqi Prime Minister-designate Ali al-Zaidi held a telephone conversation with US Secretary of War Hegseth about bilateral relations in various fields", Tasnim reported.

- The two US commercial ships that crossed the Strait of Hormuz on Monday had military security aboard, NBC reported citing sources.

- A French bulk carrier was hit by a cruise missile in the waters near the UAE, CBS reported citing officials.

- CMA CGM confirms a vessel was the target of an attack on Tuesday while it was crossing the Strait of Hormuz.

EUROPEAN TRADE

EQUITIES

- European bourses are stronger across the board, buoyed by optimism surrounding US-Iran peace. Opened higher as markets reacted to Trump’s decision to temporarily pause “Project Freedom”, and then took another leg higher to make fresh peaks on an Axios report which suggested that the US and Iran are closing in on an MoU to end the conflict.

- European sectors are entirely in the green, except for Energy and Utilities; the latter, unsurprisingly, is hampered by losses in underlying oil prices. The top of the pile consists of Basic Resources (lifted by strength in metals prices), Autos and Consumer Products. The Autos sector has been driven higher by post-earning strength in BMW (+5%, beat exp. but faced fierce price competition in China) and Continental (+5.5%, Q1 results topped exp. and confirmed guidance). The Consumer Products sector has benefited from gains in jewellery-name Pandora (+9%) after Q1 revenue beat estimates, but did experience weakness across North America and Europe.

- US equity futures are entirely in the green, following the geopolitical-related optimism seen in Europe; the NQ (+1.3%) outperforms vs ES/RTY, thanks to pre-market strength in AMD (+17%). The chip-maker beat on its headline metrics, and guidance came in stronger than forecast, driven by accelerating data centre growth and strong demand for processors and GPU shipments. Further lifting Tech sentiment is a piece in The Information, outlining that Anthropic committed to spend USD 200bln with Google Cloud over five years under a recent agreement.

- AMD (+18% pre-market) after earnings and revenue beat expectations, and guidance came in stronger than forecast, driven by accelerating data centre growth and strong demand for processors and GPU shipments.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Snapshot: G10s are stronger against the USD this morning, to varying degrees. Antipodeans outperform, given the risk tone; JPY is also towards the top of the pile, following likely intervention overnight. SEK is a touch weaker vs EUR, after a cooler-than-expected inflation report, but is unlikely to shift the dial for the Riksbank on Thursday.

- DXY is weaker this morning, and currently trades at the lower end of a 97.79 to 98.34 range. Pressure facilitated by the risk-on mood, amidst optimism surrounding progress towards US-Iran peace. This stems from a post from the POTUS, who announced that the US would pause Project Freedom to allow time for negotiations to occur. The move lower was then exacerbated after an Axios report suggested that the US and Iran are closing in on an MoU to end the conflict. In its current form, it would declare and end to the war with Iran. Potential JPY intervention also facilitating the pressure this morning

- Focus overnight was on USD/JPY, where an aggressive move lower took the pair to a 155.00 handle, before bouncing back towards 156.00. There is currently no confirmation that the move was intervention, but markets should begin to get some details on recent moves late in the Japanese session. Time will tell whether these attempts of intervention proves effective, given the volatile nature of the Middle Eastern conflict. A near-term resolution will help the USD/JPY trundle lower, a factor which Japanese Officials would probably require to achieve any lasting strength in the JPY.

FIXED INCOME

- Unsurprisingly, a bullish start for fixed income as the marked energy retreat has allowed yields to ease. Pressure in energy facilitated by a) Trump pausing Project Freedom to allow time for negotiations, b) Axios report suggested US-Iran are close to an MoU. (See geopols section for details).

- USTs to a 110-28+ peak, with gains of 15 ticks and breaching Monday's WTD 110-26+ best. For the US, aside from geopols, we are attentive to ADP ahead of NFP on Friday; ADP is seen at 79k from 62k, vs a 73k (prev. 178k) consensus for Friday's Payrolls. Additionally, we get the full Treasury Quarterly Refunding announcement after Monday's projections, before remarks from Fed's Musalem (2028) and Goolsbee (2027).

- Bunds post gains in excess of 80 ticks and currently hold just off a 125.88 peak. A high that printed in proximity to the above geopolitical updates this morning, and after a slew of Final PMIs, which were subject to modest revision. Of note for policymakers, the ECB's latest wage tracker showed upside across the year. Though, the ECB will at this stage likely welcome the relatively modest level of upside and particularly that the Q4-2026 figure remains shy of the 2.709% reported in February.

- Gilts gapped higher by 48 ticks before climbing another 30 ticks to an 87.32 peak, notching a new high for the week, but remain shy of last week's 87.03 closing price. Potentially capping a return to and test of that level is the ongoing scrutiny around PM Starmer, as UK press continues to brief that the challenge against Starmer is increasing, with the Welsh Labour leader seemingly primed to call for Starmer to step down on Friday and reports that the party is working to get Burnham back in the Commons.

- Germany sells EUR 2.662bln vs exp. EUR 3.5bln 2.50% 2032 Bund Auction: b/c 2.4x (prev. 1.1x), avg. yield 2.8% (prev. 2.78%), retention 23.94%.

- China sold 50-year ultra-long special treasury bonds at 2.52%.

- Australia sold AUD 1.0bln 4.25% 2036 AGBs: b/c 3.86x, average yield 4.9735%.

COMMODITIES

- Energy on the backfoot after US President Trump paused Project Freedom to allow time for talks and potential progress with Iran. An update that weighed on crude overnight, sending WTI below USD 100/bbl and Brent beneath USD 108/bbl. Thereafter, the complex took another hit after an Axios report which suggested that the US and Iran are closing in on an MoU to end the conflict (see geopols section for details).

- As it stands WTI Jun’26 and Brent Jul’26 are holding towards session lows at USD 93.96/bbl and USD 101.46/bbl, respectively. Brent now eyes USD 100/bbl to the downside, and a further leg lower could see a retest of the low from 27th April 2026, at USD 99.58/bbl.

- Gold is benefiting from the energy and USD downside, XAU as high as USD 4,708/oz, matching its 21 DMA. Base metals are also firmer, cheering the general risk tone and welcoming the return of Mainland China. 3M LME Copper above USD 13.2k, with gains in excess of USD 150 as things stand.

- China has ordered its oil refineries that purchase crude from Tehran not to comply with or enforce US sanctions on Iranian oil, CNN reported.

- Australia's PM Albanese said that they are to lift minimum stockpiles of every type of fuel by around 10 days, the fuel reserve is to be around 1 billion litres and the package is to cost more than AUD 10bln.

- Weekly private inventory data (bbls): Crude -8.1mln (exp. -2.8), Gasoline -6.1mln (exp. -1.7mln), Distillates -4.6mln (exp. -2mln), Cushing -1.1mln.

TRADE/TARIFFS

- Chinese Foreign Ministry Spokesperson Lin said China and the US are in communication on Trump's trip.

- US Ambassador Puzder wants the US-EU trade agreement to be agreed on before July, Bloomberg TV.

- US Envoy to India said Indian companies plan to invest over USD 20.5bln in the US tech, manufacturing and pharmaceuticals.

NOTABLE EUROPEAN DATA RECAP

- EU PPI MoM (Mar) M/M 3.4% vs. Exp. 3.3% (Prev. -0.7%, Low. 0.8%, High. 3.7%).

- EU PPI YoY (Mar) Y/Y 2.1% vs. Exp. 1.8% (Prev. -3%, Low. -0.5%, High. 2.1%).

- EU S&P Global Composite PMI Final (Apr) 48.8 vs. Exp. 48.6 (Prev. 50.7).

- EU S&P Global Services PMI Final (Apr) 47.6 vs. Exp. 47.4 (Prev. 50.2).

- UK S&P Global Services PMI Final (Apr) 52.7 vs. Exp. 52 (Prev. 50.5).

- UK S&P Global Composite PMI Final (Apr) 52.6 vs. Exp. 52.0 (Prev. 50.3).

- Italian Retail Sales MoM (Mar) M/M 0.8% vs. Exp. -0.4% (Prev. 0%).

- Italian Retail Sales YoY (Mar) Y/Y 3.7% (Prev. 1.6%).

- Italian S&P Global Composite PMI (Apr) 50.5 (Prev. 49.2).

- Italian S&P Global Services PMI (Apr) 49.8 vs. Exp. 48.1 (Prev. 48.8).

- German S&P Global Composite PMI Final (Apr) 48.4 vs. Exp. 48.3 (Prev. 51.9).

- German S&P Global Services PMI Final (Apr) 46.9 vs. Exp. 46.9 (Prev. 50.9).

- French S&P Global Composite PMI Final (Apr) 47.6 vs. Exp. 47.6 (Prev. 48.8).

- French S&P Global Services PMI Final (Apr) 46.5 vs. Exp. 46.5 (Prev. 48.8).

- French Industrial Production MoM (Mar) M/M 1.0% vs. Exp. 0.5% (Prev. -0.7%).

- Spanish S&P Global Composite PMI (Apr) 48.7 (Prev. 52.4).

- Spanish S&P Global Services PMI (Apr) 47.9 vs. Exp. 52.1 (Prev. 53.3).

- Swedish Services PMI (Apr) 52.5 (Prev. 55.7).

- Swedish CPIF-XE Prelim. (Apr): 0.0% Y/Y (prev. 1.1%), M/M -0.6%.

- Swedish CPIF MoM Prel (Apr) M/M -0.6% (Prev. -0.6%).

- Swedish CPIF YoY Prel (Apr) Y/Y 0.8% vs exp. 1.2% (Prev. 1.6%).

CENTRAL BANKS

- ECB's Cipollone said the EZ inflation trend is moving towards adverse.

- ECB Wage Tracker: 2026 annual 2.282% (prev. 2.270%). Q1 1.847% (prev. 1.887%). Q2 2.131% (prev. 2.10%). Q3 2.553% (prev. 2.521%). Q4 2.597% (prev. 2.574%).

- BoE Governor Bailey said we must be mindful of risks of private credit.

- NAB sees the RBA hiking in June to take the cash rate to 4.60%.

- RBNZ Governor Breman said banks are resilient under stress tests.

- RBNZ Financial Stability Report: New Zealand's financial system is resilient and well positioned to support households and businesses even if economic conditions soften. The global risk environment has worsened over the past six months, as conflict in the Middle East threatens world energy supply.

- PBoC set USD/CNY mid-point at 6.8562 vs exp. 6.8160 (prev. 6.8628).

- BoK official said inflation is seen higher in May and are closely monitoring inflation trend as uncertainty is high over the Middle East situation.

CRYPTO

- Bitcoin rises to a 3-month high, now trading above USD 81k.

APAC TRADE

- Asia-Pac stocks traded entirely in the green, following on from the gains stateside and the positive update from President Trump, stating that Project Freedom is to be paused for a short time to see whether or not the agreement with Iran can be finalised and signed.

- ASX 200 neared last week’s peak of 8787, rebounding after two consecutive days of losses. The bounce was supported by Financials and Industrials, while Energy lagged as oil prices fell.

- KOSPI surged at the open, breaking the 7000 handle, and even activated the buy-side sidecar within the first 5 minutes of trade. Tech giants helped the surge in the index, with Samsung Electronics (+15%) being the latest Co. to join the USD 1tln market cap group.

- Shanghai Comp. and Hang Seng followed the positive risk-on tone as Shanghai returned from holidays. CK Hutchison gained after the Co. agreed to sell its 49% stake in VodafoneThree, while Wuliangye Yibin underperformed after a double downgrade at Goldman Sachs. On the data front, RatingDog services PMI beat estimates, which further supported the indices.

NOTABLE ASIA-PAC HEADLINES

- China's Foreign Minister Wang Yi held talks with Iranian Foreign Minister Araghchi, Xinhua reported.

NOTABLE APAC DATA RECAP

- Indian HSBC Services PMI Final (Apr) 58.8 (Prev. 57.5).

- Indian HSBC Composite PMI Final (Apr) 58.2 (Prev. 57.0).

- Chinese RatingDog Composite PMI (Apr) 53.1 (Prev. 51.5).

- Chinese RatingDog Services PMI (Apr) 52.6 vs. Exp. 52.0 (Prev. 52.1).

- Hong Kong S&P Global PMI (Apr) 48.6 (Prev. 49.3).

- Australian Ai Group Construction Index (Apr) -19.3 (Prev. -31.4).

- Australian Ai Group Manufacturing Index (Apr) -27.9 (Prev. -27.9).

- Australian Ai Group Industry Index (Apr) -24.4 (Prev. -23.6).

- New Zealand Participation Rate (Q1) 70.40% (Prev. 70.5%).

- New Zealand Employment Change QoQ (Q1) Q/Q 0.2% vs. Exp. 0.3% (Prev. 0.5%).

- New Zealand Labour Costs Index QoQ (Q1) Q/Q 0.5% vs. Exp. 0.4% (Prev. 0.4%, Low. 0.3%, High. 0.4%).

- New Zealand Labour Costs Index YoY (Q1) Y/Y 2.0% vs. Exp. 2% (Prev. 2%, Low. 1.9%, High. 2%).

- New Zealand Unemployment Rate (Q1) 5.3% vs. Exp. 5.4% (Prev. 5.4%, Low. 5.3%, High. 5.5%).

NOTABLE APAC EQUITY HEADLINES

- BHP (BHP AT) CFO said new investors are buying into the Co. on copper exposure and AI demand.

- KOSPI sidecar activated after KOSPI 200 futures rise by 5%.