Published: 13 May 2026, 10:35 UTC

Newsquawk Desk

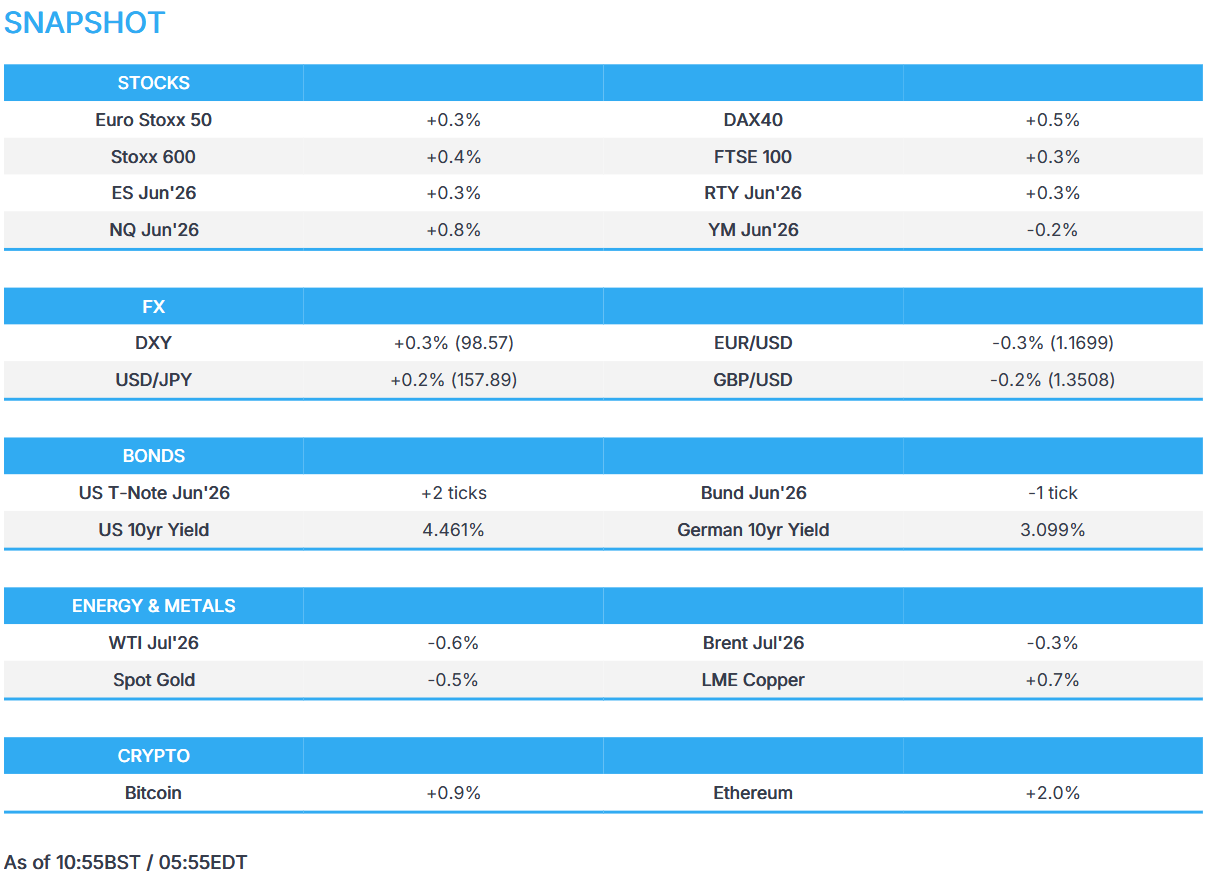

US Market Open: Equities broadly in the green with US/China summit looming; GBP continues lower as domestic politics dominates

0:00--:--

- US Treasury Secretary Bessent and Vice Premier He held talks. Following the conclusion, Chinese state media reported that China and the US held candid, in-depth and constructive exchanges.

- European bourses rebounded from Tuesday's selloff, DAX 40 outperform following a heavy earnings docket; US equity futures gain.

- GBP mixed against its peers as Starmer appears on a firmer footing but risks remain into on the return of Parliament.

- Global fixed benchmarks are flat/incrementally firmer, Gilts find reprieve after recent pressure.

- Crude lower but off lows after taking a breather overnight; IEA said world oil supply to fall by 3.9mln bpd in 2026.

- Looking ahead, highlights include US PPI (Apr), BoC Minutes (Apr), OPEC MOMR (May). Speakers include BoE’s Mann, Fed’s Collins & Kashkari, ECB’s Lane & Lagarde. Supply from the US. Earnings from Cisco Systems.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.4%) have begun to reverse the losses seen at the start of the week, despite the mixed Asia-Pac and stateside trade. The DAX 40 is the outperformer, helped by a flurry of positive earnings, while the CAC 40 lags its peers despite the gains in STMicroelectronics and ArcelorMittal.

- Sectors point to a more mixed picture. Basic Resources tops the pile, as copper extends above USD 14k/t while aluminium, nickel and iron ore are also bid. The underperformer is Media, closely followed by Travel & Leisure. TUI reported Q2 earnings, in which it sees strong demand in the Holiday Experiences Business Area in H2.

- US equity futures broadly higher pre-market, with the tech-heavy NQ leading gains with chip names in Asia/European trade resuming gains.

- Alibaba Group Holding (BABA) - Q4 2025 (CNY): EPS 1.30 (exp. 0.89), Revenue 243.38bln (exp. 282.47bln); "confident in our business outlook and will continue to invest in AI + Cloud to strengthen our competitive advantages"

- Siemens (SIE GY) - Q2 2026 (EUR): Revenue 19.8bln (exp. 20.1bln), Orders 24.11bln (exp. 22.6bln), Net Income 2.24bln, -8.3% Y/Y. Co. announces up to EUR 6bln share buyback for up to 5 years; confirms FY26 outlook.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s trade under a relatively strong USD, with recent upside in DXY as it vaulted its 100-DMA (98.45) and 200-DMA (98.52), to make a current peak at 98.58.

- USD continues to be driven by oil/yields as geopolitics remain in focus. Today, US President Trump is expected to arrive in China for his summit with Xi, where talks are expected to take place on Thursday and Friday. No breakthrough is expected in US-China relations, though the situation in Iran will likely be one of the core topics, with some fearing an Iran-for-Taiwan bargain. (Full analysis at 06:50BST on the headline feed). The session also sees a number of Fed speakers, including Collins, Kashkari and Logan.

- GBP trades a touch lower against a strong buck, but stronger against the Euro despite continued political uncertainty. As it stands, the PM intends to stay in his post and run in any leadership contest against challengers (likely Streeting. Potentially, Miliband, Rayner, Carns, and/or Burnham). Theoretically, if a contest were to be triggered now, Starmer would be the favourite (100+ MPs back him, against c. 90 who have expressed no-confidence). Recent newsflow has been around a very brief Starmer-Streeting meeting. We are unlikely to see a readout due to the King's speech later today. In terms of timing, at 14:30 BST, two backbench (Junior) Labour MPs will ask "typically light-hearted" questions, according to Politico. Opposition leader Badenoch speaks third, then the PM will respond to her questions.

- EUR/GBP trades towards the lower end of Tuesday's 0.8653-0.8697 range, Cable continues to move lower as it did on Tuesday, currently supported by the 1.3530, with further support lower at 1.35, the previous session's low. Ultimately, any leadership change would likely be a shift to the left and therefore weigh on the Pound.

FIXED INCOME

- Global benchmarks are incrementally firmer/flat this morning as crude benchmarks pull back from recent highs, and as geopolitical/political newsflow remains light.

- USTs are firmer by a couple of ticks and currently trade within a narrow 109-31+ to 110-04 range, but ultimately residing near the prior day’s trough at 110-01. As a reminder, US paper was pressured on Tuesday amidst higher energy prices and after a hotter-than-expected US CPI report, which has led markets to reprice hawkishly. Most recently, UBS pushed back its call for a cut at the Fed to December 2026 and March 2027 (prev. forecast cuts in September and December). Focus today will be on US PPI and a flurry of Fed speakers.

- Bunds are essentially flat in a quiet 124.59 to 124.87 range. Earlier this morning German Wholesale Prices M/M topped expectations, with the Y/Y figure also rising from the prior. The statistics office cited the war in the Middle East as the region for the jump in prices, “particularly for energy products and raw materials”. Despite the jump in prices, Bunds were choppy but ultimately little moved. Thereafter, EZ GDP 2nd estimate was not subject to revisions, whilst Employment Change Q/Q fell from the prior. No move following the German 2047/2054 auctions.

- Gilts initially gapped higher at the open, peaking at 86.31, as UK paper found some reprieve following on from a dire session seen in the prior session; traders may have also priced in the chance of quiet domestic politics, ahead of the King’s speech. However, since the cash open, UK paper has gradually trundled lower and is now only firmer by a handful of ticks – conforming to the action seen across peers. From a yield perspective, the 10yr remains above the 5% mark and a little short of the peaks made on Tuesday (5.13%).

- Markets remain on watch for domestic politics, and particularly on Wes Streeting after his short meeting with PM Starmer – UK journalists are questioning whether this signals increased likelihood of a potential leadership challenge. Before the duo met, Sky News reported that UK government whips believe Wes Streeting will make his move on Thursday, to avoid clashing with the King’s Speech, while they also believe Andy Burnham doesn’t have an MP ready to quit.

- Australian debt agency is to issue Treasury bonds of around AUD 125bln for 2026/2027, while further guidance of issuance plans will be provided in June.

- Australia sells AUD 300mln 4.75% June 2054 bonds b/c 4.08, avg yield 5.4979%.

- Italy sells EUR 7.5bln vs exp. EUR 6.25-7.5bln 2.40% 2029, 3.30% 2033 and 2.95% 2038 BTP.

- Germany sells EUR 1.14bln vs exp. EUR 1.5bln 2.50% 2054 and EUR 0.986bln vs exp. EUR 1bln 3.40% 2047 Bund.

COMMODITIES

- In geopolitics, US President Trump said Iran will either make a deal or be “decimated”, while reaffirming the effectiveness of the blockade. Meanwhile, Iran reiterated five conditions before entering nuclear talks, including sanctions relief, reparations and recognition of sovereignty over the Strait of Hormuz. US intelligence reportedly assessed Iran still retains significant missile capabilities along the Strait of Hormuz. Further, Sources familiar with negotiations said Iran’s top conditions before nuclear talks include ending the war on all fronts, lifting sanctions, releasing frozen funds, compensation for war damages and recognition of Iranian sovereignty over the Strait of Hormuz.

- Elsewhere, the IEA released its monthly oil market report today, in which it forecasts world oil supply to fall by 3.9mln bpd in 2026, assuming Strait of Hormuz flows gradually resume from June (prev. forecast 1.5mln bpd fall); Sees total world oil supply 1.78mln bpd lower than demand in 2026 (vs. prev. forecast 0.41mln bpd higher). IEA noted the war in the Middle East is depleting global oil inventories at a record pace.

- WTI July and Brent July futures have trimmed losses seen overnight, with the former in a USD 96.79-98.58/bbl range and the latter in a USD 106.09-107.56/bbl. Dutch TTF is now flat intraday after recovering from sub-EUR 46/MWh lows to levels north of EUR 46.50/MWh.

- Spot gold resides in a USD 4,685.90-4,727/oz range, well within yesterday’s USD 4,638.36-4,773.58/oz parameter, with the 100 DMA at USD 4,786.96/oz. Spot silver takes a breather from six straight sessions of gains, with the precious metal pulling back a touch after hitting resistance around USD 87.80/oz. Elsewhere, Shanghai Futures Exchange adjusted the price limit for the AG2705 silver futures contract to 17%.

- Base metals are posting varying gains across the board amid a broadly but cautiously positive risk appetite across Europe and US markets, and despite a firmer USD. 3M LME copper resides north of USD 14k/t in a 14,086.58- 14,191.48/t range at the time of writing.

- IEA OMR: world oil supply to fall by 3.9mln bpd in 2026 assuming Strait of Hormuz flows gradually resume from June (prev. forecast 1.5mln bpd fall); Sees total world oil supply 1.78mln bpd lower than demand in 2026 (vs. prev forecast 0.41mln bpd higher). Sees world oil demand falling by 420k bpd in 2026 on Iran war (prev. forecast 80k bpd drop).

- US Private Inventory Data (bbls): Crude -2.2mln (exp. -2.3mln), Distillates -0.3mln (exp. -1.3mln), Gasoline +0.5mln (exp. -2.5mln), Cushing -1.8mln

- US NEC Director Hassett said this is a temporary energy shock and that President Trump is confident the Strait of Hormuz will be open soon, while Hassett said regarding the SPR that they are releasing as fast as possible. Furthermore, he said Trump's view is that we should modernise the gasoline tax.

- Russia’s Perm oil refinery (260k BPD) has halted operations after May 7 drone attack, according to sources.

- Kuwait lowers June crude prices for Asia, according to a pricing document.

- UAE's ADNOC has set June Murban crude OSP at USD 104.44/bbl, USD -6.31/bbl from May.

- Mexico's Pemex has partially shut down its 325,000bpd Salina Cruz refinery due to circuit contamination affecting utilities, according to Iir Energy.

TRADE/TARIFFS

- The US White House has reportedly not ruled out potential Chinese direct investment in the US, Semafor reported.

- US President Trump posted that NVIDIA CEO Huang is on Air Force One along with a number of CEOs of large US companies, including Tesla, Boeing, Cargill, Citi, Goldman Sachs, GE Aerospace, Micron & Qualcomm. Trump added that his first request to Chinese President Xi will be to open up China so that these brilliant people can work their magic.

- US Treasury Secretary Bessent and Vice Premier He held talks. Following the conclusion, Chinese state media reported that China and the US held candid, in-depth and constructive exchanges.

- EU Commission has outlined a potential compromise to break the EU-US trade deal deadlock, with specific reference to the sunrise clause, Politico reported.

NOTABLE EUROPEAN HEADLINES

- UK Labour-affiliated union group TULO said Labour cannot continue on this path, is it clear the PM will not lead Labour into the next election.

- SNP to force a vote on UK PM Starmer via an amendment to King’s Speech debate.

- UK government appoints loyalists to fill gaps left by government resignations.

- UK government whips believe Wes Streeting will make his move on Thursday, to avoid clashing with the King’s Speech, while they also believe Andy Burnham doesn’t have an MP ready to quit, and that aside from the 87 MPs who’ve publicly called for Starmer to go, the same number privately want him to step down, according to Sky News reporter Jon Craig.

NOTABLE EUROPEAN DATA RECAP

- EU GDP Growth Rate QoQ 2nd Est (Q1) Q/Q 0.1% vs. Exp. 0.1% (Prev. 0.2%).

- EU GDP Growth Rate YoY 2nd Est (Q1) Y/Y 0.8% vs. Exp. 0.8% (Prev. 1.2%, Low. 0.8%, High. 0.8%).

- EU Industrial Production MoM (Mar) M/M 0.2% vs. Exp. 0.3% (Prev. 0.4%).

- EU Industrial Production YoY (Mar) Y/Y -2.1% (Prev. -0.6%).

- French Inflation Rate MoM Final (Apr) M/M 1.0% vs. Exp. 1% (Prev. 1%, Low. 1%, High. 1.1%).

- French Inflation Rate YoY Final (Apr) Y/Y 2.2% vs. Exp. 2.2% (Prev. 1.7%, Low. 2.2%, High. 2.2%).

- German Wholesale Prices MoM (Apr) M/M 2% vs. Exp. 1% (Prev. 2.7%).

- German Wholesale Prices YoY (Apr) Y/Y 6.3% (Prev. 4.1%).

- Swedish CPIF MoM Final (Apr) M/M -0.6% vs. Exp. -0.6% (Prev. -0.6%).

- Swedish CPIF YoY Final (Apr) Y/Y -0.1% vs. Exp. 0.8% (Prev. 1.6%).

CENTRAL BANKS

- ECB's Muller said the EU has not fallen into stagflation.

- ECB's Villeroy said the ECB must be ready to intervene on second round effects; underlying inflation is currently under control.

- ECB's Rehn said inflation expectations are still anchored.

- ECB's Radev said once again, seeing an external price shock.

- ECB's Dolenc said can expect consumer expectations from inflation to rise. Energy prices have a limited effect on the economy for now.

- ECB’s Elderson said banks need to update resilience plans to cater for the higher probability of severe disruptions because of Anthropic’ s Mythos AI tool.

- Riksbank Minutes: Market expectations regarding central bank policy rates have been closely interlinked with the inflation risks stemming from energy prices.

- BoJ will continue to closely monitor how the Middle East situation will affect economy and prices, according to an official.

- UBS sees the Fed to cut 25bps in December 2026 and March 2027 (prev. forecast cuts in September and December).

GEOPOLITICS

MIDDLE EAST

- US President Trump posted "When the Fake News says that the Iranian enemy is doing well, Militarily, against us, it’s virtual TREASON in that it is such a false, and even preposterous, statement. They are aiding and abetting the enemy! All it does is give Iran false hope when none should exist."

- "Pakistan’s Foreign Ministry is all set to hold a consultative meeting of its envoys in Middle East, West Asia and important capitals on Thursday in Islamabad", Pakistani journalist Mallick posted.

- Iranian Foreign Ministry spokesman said Iran will obtain a more accurate assessment of the American position through Pakistani mediators, Al ArabyTV reported. Further stated that Tehran rejects maximalist demands regarding its Nuclear Program and considers them unjust.

- Iranian Foreign Minister Araghchi said a lack of good faith and the dishonesty of the US is the most significant obstacle to a definitive end to the war, while he commented that the main cause and origin of the current situation in the Strait of Hormuz is the US and Israeli regime's military aggression against Iran, and subsequently the repeated violation of the ceasefire through the continued blockade of Iran's maritime ports. Furthermore, he said they are holding consultations to draft regulations concerning arrangements for the Strait of Hormuz in accordance with international law.

- Pakistan and Iraq have struck agreements with Iran to transport liquefied gas and oil via the Strait of Hormuz amid shipping risks, according to sources.

- China-flagged supertanker attempts to exit Hormuz, according to reports citing data.

- India, Japan and most European nations joined the Hormuz Strait draft resolution, while 112 countries back the resolution, according to Al Jazeera.

OTHER

- A group of bipartisan US senators is writing to Secretary of State Rubio to pledge their support for the Taiwan Relations Act, Semafor reported; Twelve senators signed the letter.

- North Korea leader Kim inspected munitions factories and called for modernisation and efficiency gains in the arms industry, according to KCNA.

CRYPTO

- Bitcoin neared the USD 82k handle, paring back most of Tuesday's losses.

APAC TRADE

- APAC stocks traded mixed following on from the mostly subdued handover from Wall Street, where sentiment was dampened by tech weakness, higher oil prices and firmer-than-expected inflation, while the geopolitical situation remained uncertain with Iran said to require five confidence-building conditions for it to enter a second round of talks with the US.

- ASX 200 declined amid weakness in the top-weighted financial sector after shares in Australia's largest lender CBA, slumped around 10% following its earnings results, while the recent federal budget announcement failed to spur risk appetite and was seen by analysts to hit consumer stocks.

- Nikkei 225 clawed back initial losses after encouraging current account and bank lending data, and despite hawkish market pricing of around a 70% chance for a BoJ rate hike next month.

- Hang Seng and Shanghai Comp were mixed as participants digested earnings releases and with the focus on the looming Trump-Xi summit, while the US President is on his way to Beijing with various CEOs on Air Force One, including the late addition of NVIDIA's Jensen Huang.

NOTABLE ASIA-PAC HEADLINES

- BoJ said there was no meeting held between the US Treasury Secretary Bessent and BoJ Governor Ueda.

- US Treasury Secretary Bessent said that thanks to the powerful bond between US President Trump and Japanese PM Takaichi, the relationship between the US and Japan is stronger than ever before, while he was happy to share with the PM the belief that the fundamentals of the Japanese economy are indeed strong and resilient. Furthermore, he said they exchanged views on the US-Japan investment program, critical minerals, President Trump's upcoming visit to Beijing, and other subjects of mutual interest.

NOTABLE APAC DATA RECAP

- Japanese Current Account (Mar) 4682B vs. Exp. 3900B (Prev. 3933B)

- Japanese Bank Lending (Apr) Y/Y 5.4% vs. Exp. 4.6% (Prev. 4.8%)

- Australian Wage Price Index QQ (Q1) 0.8% vs. Exp. 0.8% (Prev. 0.8%, Low. 0.8%, High. 0.9%)

- Australian Wage Price Index YY (Q1) 3.3% vs. Exp. 3.3% (Prev. 3.4%, Low. 3.3%, High. 3.4%)

- New Zealand 1-Year Inflation Expectations (Q2) 3.4% (Prev. 2.6%)

- New Zealand 2-Year Inflation Expectations (Q2) 2.5% (Prev. 2.4%)