Published: 14 May 2026, 10:55 UTC

Newsquawk Desk

US Market Open: Constructive US/China summit boosts ES and NQ, US said to approve some H200 chip sales, NVDA +2%; US data/Fed speak ahead

0:00--:--

- US President Trump had a good meeting with Chinese President Xi, in which the two sides discussed ways to enhance economic cooperation. The two sides agreed that the Strait must remain open and that Iran can never have a nuclear weapon. However, Taiwan was not mentioned.

- US President Trump's team is now discussing options for military escalation to break the deadlock, Axios reported. Options include resuming Project Freedom or striking Iranian infrastructure.

- European bourses continue to rebound; NVDA gains after the US reportedly approved around 10 Chinese firms to buy H200 chip.

- DXY flat, GBP immediately pared post-GDP gains as politics remains in focus.

- USTs attempt to bounce back from recent losses; Gilts eye a potential leadership challenge.

- Crude holds a mild upward bias but wanes off its best levels as US and Iran prefer diplomacy.

- Looking ahead, highlights include Trump-Xi Summit (14th-15th May); US Retail Sales (Apr), Export/Import Prices (Apr), Jobless Claims (May 9), Atlanta Fed GDP. Speakers include BoE’s Pill, Fed’s Bowman, Miran, Logan, Schmid, Hammack & Williams.

- Holiday: Ascension Day Holiday (Closures in Switzerland, Sweden, Norway, Finland, Denmark).

TRUMP-XI SUMMIT

- In the White House official statement, it stated that US President Trump had a good meeting with Chinese President Xi, in which the two sides discussed ways to enhance economic cooperation. On the Iran conflict, the two sides agreed that the Strait must remain open and that Iran can never have a nuclear weapon. However, Taiwan was not mentioned.

- US President Trump told Chinese President Xi that they've had a fantastic relationship, and they are going to have a fantastic future together, while he added that he has such respect for China and that he tells everybody Xi is a great leader. Trump also stated that the relationship between the US and China will be better than before, with trade to be totally reciprocal on their behalf and he looks forward to doing business with China.

- Chinese President Xi said to US CEOs that China's door will only open wider, adds China welcomes US to strengthen reciprocal cooperation in China, according to Xinhua.

- Chinese President Xi told US President Trump it is a pleasure to meet him in Beijing, while he has always believed that the common interests between China and the US outweigh the differences. Xi stated that the success of China and the US is an opportunity for each other, and he looks forward to discussions with US President Trump.

- Chinese President Xi said talks are the only right way to resolve disputes and that there are no winners in a trade war, while he also commented that the Taiwan issue is the most important in US-China ties, and if the issue is not handled well, the two countries will clash, according to Xinhua.

- China People's Republic Chair Qiang said the US and China should focus on cooperation, and continue to be friends.

- Click here for more analysis

EUROPEAN TRADE

EQUITIES

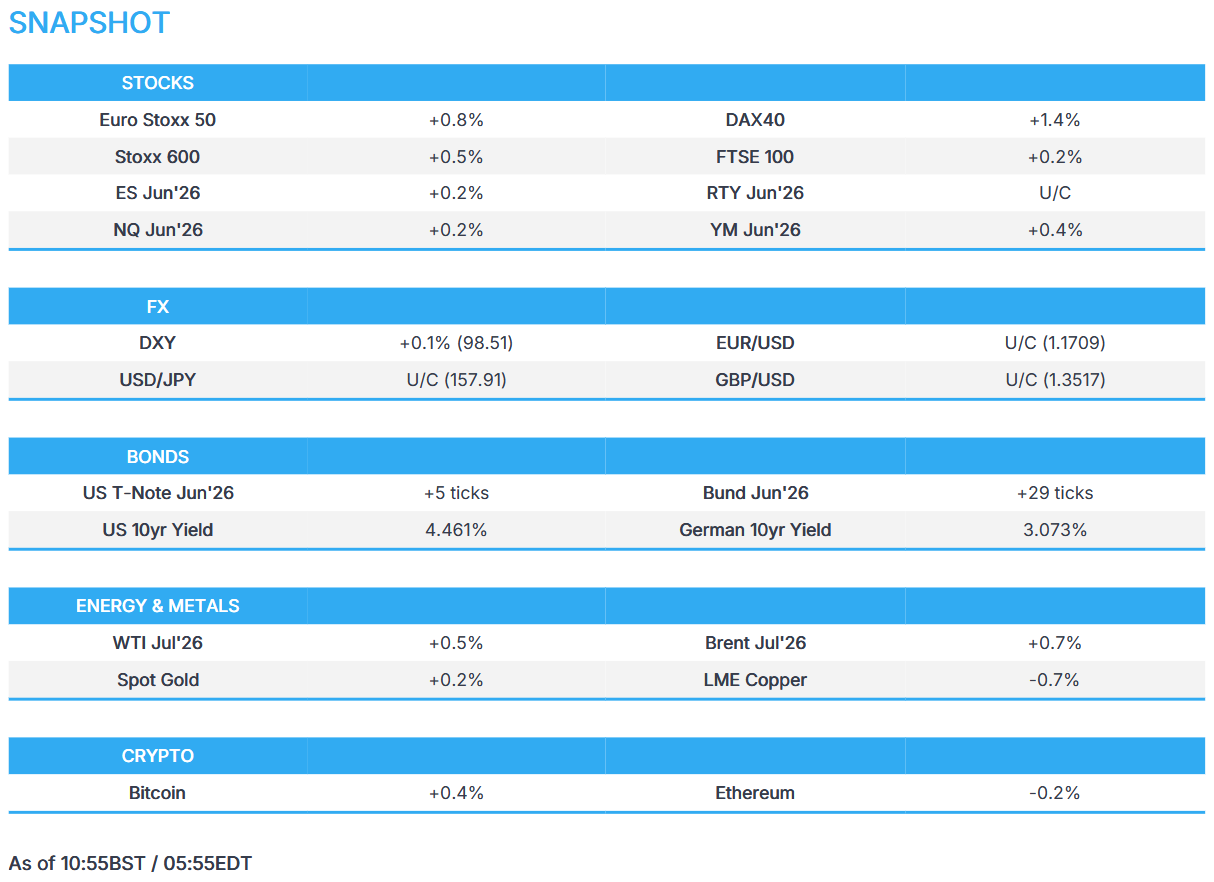

- A broadly positive start for European bourses (STOXX 600 +0.5%) to begin Thursday’s session. The DAX 40 (+1.4%) is the clear outperformer, supported by Infineon and Rheinmetall while the FTSE 100 (+0.2%) underperforms, as 3i Group slumps after its FY total return missed estimates.

- European sectors hold a positive bias. Tech tops the sector pile while Financial Services lies at the bottom. Newsflow surrounding European tech has been light, but gains in US-listed Cisco after-hours seem to have passed through to the broader tech area. A Reuters report suggesting that the US approved H200 chip sales to Chinese companies also helped to lift sentiment.

- US equity futures gain pre-market, further extending on ATHs. Initial upside in NQ futures came following reports that the US have approved around 10 Chinese firms to buy Nvidia H200 chips, and Nvidia shares have risen 2.0% pre-market as a result. Packed session ahead with Fed speak and US data, including Retail sales, Jobless claims and Import/Export prices slated.

- US approved around 10 Chinese firms to buy NVIDIA (NVDA) H200 chips, according to Reuters sources. Chinese buyers include Alibaba (BABA/ 9988 HK), ByteDance, Tencent (TCEHY/0700 HK), JD.com (JD/ 9618 HK).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY continues higher into of a packed session of US data and Fed speak. Today's focus, aside from the scheduled data/speakers, will be on the US/China summit, where we recently saw a positive US readout with no mention of Taiwan and agreement that the Strait of Hormuz must remain open. So far, the Buck has yet to move significantly to the aforementioned updates and resides within narrow 98.41-98.55 parameters.

- In terms of notable news overnight, the US Senate confirmed Kevin Warsh to Fed Chair - to remind, Powell's term officially terminates tomorrow. In terms of some analyst commentary on the Greenback, MUFG wrote this morning that the "Buck could strengthen if there is any indication that the Fed’s tolerance for looking through higher inflation is diminishing", while ING wrote "face‑to‑face summits involving the US President have tended to generate a slew of conciliatory headlines, which can bolster risk assets".

- USD/JPY continues to chop with a c. 45 pip move lower this morning, seen on hawkish remarks from BoJ's Masu, who said the central bank needed to raise rates "at the earliest stage possible". Masu, at the last BoJ confab, was not one of the three hawkish dissenters, meaning the vote split could theoretically be 5-4 should former dissenters maintain their votes. Markets are reluctant to fully price a June meeting hike, with just 15bps of tightening expected. The move seen on Masu's remarks has since been faded as oil prices remain high.

- GBP trades with mild losses, with a strong regional GDP report ultimately overlooked by ongoing political unrest. Latest UK political updates suggest former Deputy PM Rayner may put herself forward in a leadership race after HMRC cleared her tax case. Rayner has indicated she favours supporting Manchester Mayor Burnham, which potentially strengthens his bid. Burnham, however, still needs to find an MP willing to step aside to spark a by-election and give Burnham a route to Parliament; reports and denials on the seat in question continue. Some analysts are circulating a survey from Survation, which indicates that soft-left Burnham is the most popular candidate amongst Labour members by a margin. Cable finds support at the round 1.3500 mark.

- Click for NY OpEx Details

FIXED INCOME

- Global fixed benchmarks are firmer this morning, attempting to clamber off recent lows, as energy prices remain stable in today’s session. Geopolitical updates overnight were lacking, but attention this morning was on reports that a vessel off the coast of the UAE has been taken by unauthorised personnel. Later reports by Axios stating that US President Trump's team is now discussing options for military escalation to break the deadlock failed to move benchmarks.

- USTs are firmer by 5 ticks, and currently trading within a 110-02 to 110-06+ range. Strength, which appears to be a bounce-back from the lows seen on Wednesday, following a hotter-than-expected PPI report. Oxford Economics outlined that following both CPI and PPI, its PCE “nowcast points to a 3.8% y/y rise in headline prices.

- Bunds are stronger by c. 30 ticks, and trades within a 124.80 to 125.03 range. Price action has followed the above, with a lack of fundamental European drivers this morning. It is also worth noting that today is Ascension Day, celebrated across parts of Europe, so lower volumes are possible. From a policy perspective, ECB’s Chief Economist Lane stated on Wednesday that the surge in energy prices may require the Bank to deliver hikes. He continued his hawkish remarks by suggesting that an increase in selling price expectations suggests input cost pressures will map into higher output prices in the coming months.

- Gilts are performing in-line with peers, and trade within an 86.14 to 86.48 range. A strong GDP report this morning is having little follow-through on price action. ING opines that it does not change much for the BoE, which is “singularly focused on the impending inflation spike”. UK traders also eye the domestic political situation, with reports on Wednesday suggesting that Health Minister Streeting is preparing to resign as soon as today. Close allies suggest he has more than the required 81 MPs to launch a leadership contest, though others question these claims. Another growing risk is Former Deputy PM Rayner being cleared of any tax wrongdoing by the HMRC, which gives her better credibility should she decide to launch a challenge.

- JGBs underperform vs peers, following hawkish commentary from BoJ’s Masu, who stated that there is a need to raise rates at the earliest stage possible. The 10yr now resides at levels not seen since 1997. Elsewhere, the 30yr auction overnight gave an indication that demand remains strong at these elevated yields, as the b/c rose to 3.49x (prev. 3.12x). However, the wider tail suggests that some buyers are potentially holding out for a 4% yield.

- Japan sells JPY 454.4bln 30-yr JGBs; b/c 3.49x (prev. 3.12x), and average yield 3.842% (prev. 3.697%).

COMMODITIES

- In geopolitics, the US and Iran both signalled a preference for diplomacy. US VP Vance said Washington is making progress in talks and remains focused on a diplomatic path “for now”, reiterating that Tehran must not obtain nuclear weapons. Iranian Foreign Minister Araghchi also said Iran does not seek war. However, tensions remain elevated: Tehran warned that new confrontations with the US are possible, said its forces are ready to deliver a “crushing” response if attacked, and confirmed it is preparing new navigation laws for the Strait of Hormuz. Separately, Iran accused Kuwait of unlawfully attacking an Iranian boat and detaining four Iranian citizens near an island allegedly linked to US operations. Shipping risks also rose after UKMTO reported that a vessel northeast of Fujairah was taken by unauthorised personnel and moved toward Iranian waters.

- Crude markets are holding a mild positive bias but trade off best levels following the diplomacy-first approach by the US and Iran, whilst the positive US-China commentary could also be underpinning the benchmarks. Some mild pressure was seen in energy benchmarks after a WH statement outlined that the US and China agreed that the Strait of Hormuz must remain open. WTI July resides in a 95.48-98.13/bbl range while Brent July sits in a USD 104.57-107.13/bbl range. Sticking with energy, Dutch TTF meanwhile is choppy but posts mild gains (+0.2%) above EUR 47/MWh at the time of writing.

- In terms of metals, spot gold is choppy within a narrow range, and largely within yesterday’s parameters after finding support near yesterday’s trough (4,669.53/oz). Newsflow has remained somewhat light this morning with no real macro drivers. Spot gold resides in a USD 4,669-4,719/oz while spot silver consolidates with modest losses above USD 87/oz after gaining for yet another session yesterday, bringing the win streak to seven straight sessions. HSBC raised its average silver price forecasts to USD 75/oz in 2026 and USD 68/oz in 2027.

- Copper futures pulled back from record levels despite the broadly positive risk sentiment, with 3M LME copper briefly dipping under USD 14,000/t to trade in a current USD 13,887.50- 14,132.78/t range.

- Cuba's Energy and Mines Minister said Cuba has run out of diesel and fuel oil amid the US oil blockade.

- India has asked the US to extend its waiver on Russian oil, Bloomberg sources reported.

- India banned sugar exports until September 30th this year, according to a government notice.

- HSBC raises average silver price forecasts to USD 75/oz in 2026 and USD 68/oz in 2027.

TRADE/TARIFFS

- China renewed export licenses for more than 400 US beef plants, according to customs data.

- EU officials said they are open to collaboration with the UK, but the UK will need to relax its trade and economic integration stance in order to progress towards a more ambitious deal, Politico reported.

NOTABLE EUROPEAN HEADLINES

- Former UK Deputy PM Rayner is prepared to put her herself forward in any leadership race if required, Sky News' Rigby reported citing sources.

- Former UK Deputy PM Rayner said she's been cleared of any tax wrongdoing by HMRC.

- Afzal Khan told Sky News he has no plans to give up his seat for Manchester Mayor Burnham. This is a denial of earlier reports.

- Leadership candidates are considering making an early statement that Chancellor Reeves would actually be retained as Chancellor to secure market stability in the event of a longer leadership contest, according to Mail on Sunday's Hodges citing UK MPs.

- BoE is set to water down stablecoin rules after industry pressure, with Deputy Governor Breeden stating that initial plans may have been ‘overly conservative’ and the central bank is ‘looking very hard’ at alternatives, according to FT.

- British Chambers of Commerce warned UK manufacturers and construction groups will be hit by significant financial and logistical problems as a result of ministers' plans to double tariffs on steel imports from July 1st, according to FT.

NOTABLE EUROPEAN DATA RECAP

- UK GDP 3-Month Avg (Mar, Q1) 0.6% vs. Exp. 0.5% (Prev. 0.5%, Low. 0.5%, High. 0.6%).

- UK GDP Growth Rate QoQ Prel (Q1) Q/Q 0.6% vs. Exp. 0.6% (Prev. 0.1%).

- UK GDP Growth Rate YoY Prel (Q1) Y/Y 1.1% vs. Exp. 0.8% (Prev. 1%, Low. 0.6%, High. 0.7%).

- UK GDP MoM (Mar) M/M 0.3% vs. Exp. -0.2% (Prev. 0.5%, Low. -0.3%, High. 0%).

- UK Balance of Trade (Mar) -9.658B vs. Exp. -3.4B (Prev. -0.720B).

- UK RICS House Price Balance (Apr) -34% vs. Exp. -25% (Prev. -23%).

- Spanish Inflation Rate MoM Final (Apr) M/M 0.4% vs. Exp. 0.4% (Prev. 1.2%).

- Spanish Inflation Rate YoY Final (Apr) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3.4%).

CENTRAL BANKS

- BoJ's Masu said they need to raise the rate at the earliest stage possible, and due attention should be paid to whether inflation triggered by the yen's depreciation may raise people's inflation expectations and, in turn, affect underlying inflation. Masu said the BoJ will continue to raise rates in response to economic, price, and financial developments, as well as noted that Japan has clearly entered an inflationary phase. Masu said there were mixed views among policy board members at the April meeting on whether to raise the policy interest rate immediately, while he judged at the April MPM that the situation did not warrant a hasty policy rate hike. Masu also commented that he is convinced the BoJ needs to raise the policy interest rate further, so that it falls solidly within the estimated range of neutral interest rate, and warned that if inflation is not contained at an appropriate level, this could lead to a vicious cycle in which firms have to further raise wages to retain workers. Furthermore, he noted that given Japan is no longer in a deflationary period, negative real rates should be addressed as soon as possible.

- Fed’s Collins (2028 voter) said she expected the Federal Reserve would need to maintain restrictive policy for some time but hoped the economy would eventually permit more rate cuts later this year. Collins stated that further rate hikes could become necessary to cool inflation pressures and said current Fed policy remained “well positioned” to address risks. It was later reported by WSJ that Collins said she is watching the extent to which tariffs continue to pass through the price chain and that the Fed may need to raise rates if inflation pressures broaden in the coming months, but sees inflation pressures from the Iran war eventually subsiding.

- ECB's Kazaks said can't yet see full impact of Iran war on inflation, and the situation is a bit worse than the ECB's baseline scenario.

NOTABLE US HEADLINES

- US President Trump's proposals are reportedly facing opposition in Congress, Semafor reported. These include a gas tax holiday and federal funding for a new ballroom in the White House.

- US Pentagon has not signed new contracts to replenish its munitions supplies, NBC reported.

GEOPOLITICS

MIDDLE EAST

- US President Trump's team is now discussing options for military escalation to break the deadlock, Axios reported. US officials don't expect Trump to take any dramatic steps during his trip but think he could make his next move immediately afterward. One option is to resume "Project Freedom," while another is to launch a new bombing campaign focusing on Iranian infrastructure.

- Pakistan Foreign Ministry said the peace process is intact, its holding on, we remain engaged and hopeful, Journalist Mallick reported.

- Iranian Foreign Minister Araghchi said although Iranian forces are ready to "deliver a crushing and devastating response to foreign aggressors, we do not seek war."

- US Secretary of State Rubio said US hopes to convince China to play a more active role in persuading Iran to back down on its actions in the Gulf, according to Reuters.

- US intelligence report emphasised that China acted to maximise its advantage and achievements against the US following the war in Iran on the diplomatic, military, economic and intelligence levels, according to WaPo.

- UKMTO reports an incident 38NM northeast of Fujairah, UAE. The vessel has been taken by unauthorised personnel whilst at anchor and now bound for Iranian territorial waters.

- Israel is to inform the Lebanese delegation that its strategy that it will not be committing to a comprehensive ceasefire, Al Hadath reported citing sources. Israel may offer to avoid bombing northern Bekaa and Beirut

- Iraqi sources reported hearing the sound of several explosions in Erbil, Iraq, while a drone strike hit an Iranian opposition camp north of Iraq's Erbil, according to Fars. It was also reported shortly after that a second drone strike hit an Iranian opposition camp north of Erbil, according to security sources.

- Israeli raid was reported on the town of Arnoun in the district of Nabatieh in southern Lebanon, while Hezbollah said it targeted a Merkava tank with a guided missile in Tel Nahas on the outskirts of the town of Kafr Kila and achieved a confirmed hit, according to Al Jazeera. It was also reported that Hezbollah conducted 17 operations against Israeli forces on Wednesday.

- Israeli PM Netanyahu reportedly made a secret visit to the UAE in the midst of the Iran operation, where he met with UAE President Mohamed bin Zayed Al Nahyan, while the visit resulted in a historic breakthrough in relations between Israel and the UAE. However, the UAE later denied the report of a visit.

RUSSIA-UKRAINE

- Russia fired at least 800 drones in a massive daytime barrage on about 20 regions of Ukraine on Wednesday, according to NBC

- Ukraine's capital Kyiv was under Russian attack early on Thursday with explosions sounding in the city, according to reports citing its mayor Klitschko.

OTHERS

- Russia's Kremlin said President Putin's trip to China will happen very soon with preparations complete.

CRYPTO

- Bitcoin found support at the 20-SMA and nears the USD 80k handle.

APAC TRADE

- APAC stocks traded mixed following the mostly positive lead from Wall St, where markets were choppy and gradually brushed aside the firmer-than-expected PPI data amid strength in tech and communications, while the focus turns to the Trump-Xi summit, which has begun in Beijing, although it has provided very little so far to excite markets.

- ASX 200 was lacklustre as weakness in consumer staples, tech, health care and energy counterbalanced the resilience in the top-weighted financials sector, while a lack of tier-1 data added to the humdrum mood.

- Nikkei 225 initially climbed to a fresh record high, before fading the gains amid quiet catalysts.

- Hang Seng and Shanghai Comp were mixed as participants digested earnings releases, including from the likes of Alibaba and Tencent, which both beat on the bottom line but disappointed on sales, while participants now await any concrete outcomes from the Trump-Xi summit.

NOTABLE ASIA-PAC HEADLINES

- Japan considers drafting an extra budget, according to Kyodo. However, Japanese Chief Cabinet Secretary Kihara said no immediate need for a supplementary budget.