Published: 15 May 2026, 10:30 UTC

Newsquawk Desk

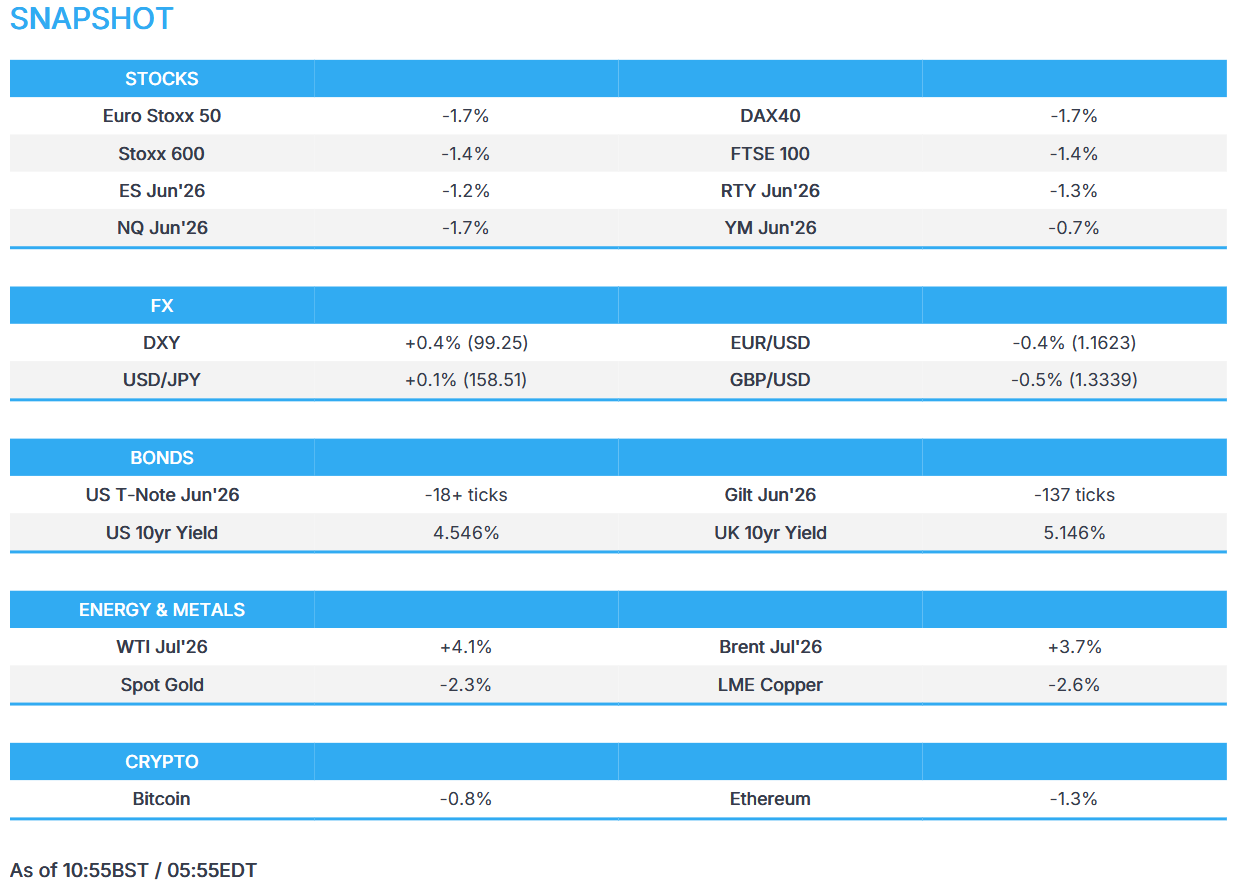

US Market Open: Stocks hit as Yields/Energy firm on renewed fears of US-Iran conflict resumption

0:00--:--

- US President Trump said it's just a question of time regarding Iran, but added that he is not going to be much more patient with Iran.

- US President Trump said he made fantastic trade deals with China, and it was an incredible visit, while they've settled a lot of different problems, and the relationship is a very strong one.

- Global equities hit, led by Tech and Basic Resources amid a number of factors: 1) Central bank repricing, 2) Tech sell-off driven by higher yields and strikes at Samsung Electronics, 3) Surging energy prices.

- DXY bid amid higher energy, GBP knocked by the potential of a Burnham premiership.

- Global yields jump amidst central bank repricing and higher energy prices.

- Crude grinds higher heading into the weekend as Trump returns from China and refocuses on Iran.

- Looking ahead, highlights include Canadian Wholesale Sales (Mar), US Industrial Production (Apr) and Credit Ratings Updates including Fitch on Germany, S&P on Italy, Morningstar DBRS on Portugal and the UK, Scope Ratings on Poland.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.4%) are entirely in the red, with sentiment hit for a multitude of factors: 1) Central bank repricing, 2) Tech sell-off driven by higher yields and strikes at Samsung Electronics, 3) Surging energy prices.

- European sectors confirm the negative bias, with only Health Care posting solid gains. Basic Resources and Tech sit at the bottom of the pile. Metal prices have slumped (XAU/USD -1.8%, XAG/USD -6%), as markets price in further rate hikes across the globe. In addition, South Korea’s KOSPI closed with losses of over 6%, adding to the pressure on silver prices as it highlights silver’s high-beta characteristics (as it stands, KOSPI-Silver correlation is c. +0.7).

- US equity futures fall as the global risk tone sours, with bond markets selling off. The surge to ATHs across the US equity space has been on a rocky footing anyway, as the market breadth fails to confirm the bid higher. One point to note, a record 30 S&P 500 stocks hit one-year lows on Wednesday.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s showing a risk-off bias as the Buck in tandem with Crude prices. Antipodeans are the underperformers, while EUR and GBP also lag amid energy/political related headwinds.

- DXY continues to perform well, vaulting 50,100 and 200 DMAs over the past two sessions amid a mix of hot US inflation data, resilient jobs data/retail sales and exponentially firm oil prices. The session ahead is absent of major data/speakers, and as such, the Greenback will likely be dictated by incoming geopolitical headlines. As a reminder, Warsh today officially takes the title of Fed Chair, while Powell becomes governor and Miran steps down. MUFG in its morning note said "This week has seen the rolling correlation between DXY and the 2-year US-DXY rates spread strengthen notably, which points to scope for US dollar strength to extend further if rate hike pricing momentum continues”.

- Once again, the centre of attention continues to be UK political developments, as markets increasingly price in the possibility of a left-leaning Burnham premiership after he announced his running in an engineered Makerfield by-election. (See 07:35 BST analysis). Sterling has weakened since the announcement on Thursday evening, but losses are somewhat limited given the continued uncertainty about whether the Manchester Mayor would be able to 1) Succeed in winning the by-election, 2) Beat incumbent Starmer in a leadership challenge. Elsewhere, keep an eye on a potential announcement on a support package for bills next week, after Housing Secretary Steve Reed touted it this morning. GBP/USD fell to a 1.3328 low where it found support.

FIXED INCOME

- Global benchmarks are down, dragged lower early in the week as markets digested hotter-than-expected CPI/PPI, the prolonged Iran conflict (higher energy prices), with fears also exacerbated by the turmoil in the UK’s Labour Party. Markets remain on tenterhooks given the mentioned factors, and this has been reflected in market pricing across several major central banks. Traders now assign a 70% chance of a 25bps hike by year-end and fully priced in for July 2027.

- USTs are currently down by 16+ ticks, and trading at the bottom end of a 109-16 to 109-29+ range. Attention over the past day has been on the Trump-Xi meeting, where initial commentary suggested positive developments; President Trump stated that many problems with China were “settled”. Focus now shifts from China, and back to Iran, where no progress has been made. Some reports have touted that Trump may look to immediately strike Iran after his China visit, to force Iran into a deal. If enacted, there is a risk that Iran chooses to restart strikes on US allies in the Middle East, leading to another spike in energy prices, hence filtering through into US yields.

- Bunds follow the negative action seen across peers, and trade at the bottom end of a 124.58 to 125.03 range. Whilst yields are firmer across the curve today, levels remain within familiar levels; 10yr holds around 3.108% vs a near-term high of 3.133%. As it stands, the belly of the curve is outperforming; however, traders may soon begin to factor in weaker economic growth across the EZ, which may see medium-term yields begin turning lower.

- Gilts underperform vs peers and are currently off by 137 ticks; holding at the bottom of an 85.44-85.85, a trough amongst the contract low. Ultimately, following peers, but the move also exacerbated by domestic politics. A full review is on the Newsquawk feed at 07:35 BST, but in brief: Labour MP for Makerfield announce he is willing to stand aside and spark a by-election, to allow current Greater Manchester Mayor Burnham to run and then, if successful, to challenge for the Labour leadership and, by association, the role of Prime Minister. For reference, Burnham was touted as the “least” market-friendly outcome by a recent FT fund manager survey.

- Australia sells AUD 1bln 1.00% December 2030 bonds b/c 3.69, avg yield 4.7049%.

COMMODITIES

- Geopolitical risk has heightened as US President Trump returns from his trip to Beijing and refocuses on the Iran situation. As a reminder, reports yesterday via Axios suggested US President Trump's team is now discussing options for military escalation to break the deadlock. Axios added that US officials said Trump could make his next move immediately after his trip to China. Options reportedly include 1) resumption of "Project Freedom," with the Navy attempting to break the logjam in the Strait of Hormuz, 2) the launch of a new bombing campaign focusing on Iranian infrastructure. Meanwhile, Israeli officials cited by Axios said they'll be on high alert this weekend in case Trump decides to resume the war.

- In terms of more recent updates, Trump warned it is “just a question of time” regarding Iran and said he will not be “much more patient” with Tehran, while reiterating that the US is monitoring Iran’s enriched uranium and could strike again if necessary, although he would prefer a diplomatic outcome. Trump added that he discussed Iran with Chinese President Xi and both sides agreed the war should end, with China later confirming the leaders reached new consensuses and calling for a comprehensive and lasting ceasefire alongside dialogue on Tehran’s nuclear programme. However, reports suggested that Washington informed Israel that Trump could still authorise fresh strikes inside Iran, while the Tehran Times reported the US formally rejected Iran’s 14-point proposal and maintained its hardline nuclear stance.

- In the European morning, an uptick in crude and a leg lower in sentiment coincided with comments from Iranian Foreign Minister Araghchi, who noted contradictory messages from the US remain the main issue. On the supply side, it’s also worth noting that the UAE announces accelerated pipeline construction to bypass the Strait of Hormuz. Nonetheless, WTI Jul rose above USD 100/bbl to currently trade towards the top end of a USD 97.23-100.93/bbl range, while its Brent Jul counterpart resides at the upper end of a 106.26-109.68/bbl parameter. Dutch TTF front-month trades higher by just shy of 3% at the time of writing, north of EUR 49.MWh, vs an earlier low of around EUR 47.60/MWh.

- Precious and base metals are softer across the board, given the energy-induced strength in the USD. Spot gold trades in a USD 4,532-4,665/oz, while Spot silver sees deep losses for a second straight session as it continues to recoil from a recent rally, with prices hitting a USD 77.66/oz low vs USD 83.88/oz intraday high, and after hitting a USD 89.37/oz peak on Wednesday. 3M LME copper continues to pull back from record levels, dipping under USD 14,000/t to trade in a current USD 13,586.00- 13,961.03/t range.

- UAE is to complete the construction of a new West-East pipeline project in 2027, Bloomberg reported. The ADNOC Chairman later said they are reviewing progress on the new West-East Pipeline (c. 1.5mln BPD, when complete), set to double the co.'s export capacity via Fujairah.

- Abu Dhabi backs USD 13bln US gas plant as Middle East supplies falter, according to FT.

- Japan's METI met and confirmed that, at the next meeting, they will deepen consideration on the diversification of oil procurement sources and improve the domestic supply system and future oil reserves, Nikkei reported.

TRADE/TARIFFS

- US President Trump said they have gotten along well with Chinese President Xi and have a very good relationship with China, while he added Xi is a tremendous and strong leader, and that he would like to see US companies do more business in China. Trump said he spoke to Xi strongly about trade and intellectual property, as well as noted that China will open the country in stages and that it would be good for US companies. Furthermore, Trump said China is going to be buying a lot of farm products, as well as stated that he asked China about using Visa (V), and maybe the China Visa ban will come off.

- Chinese President Xi said the US and China agreed to enhance talks on regional issues, Chinese State media reported. The two sides reached an important consensus and agreed to stabilise trade relations.

- China's Foreign Ministry said US President Trump and Chinese President Xi reached a series of new consensuses, while it added that the war should not continue and that China is to contribute to Middle East peace. It also said a comprehensive and lasting ceasefire should be reached as soon as possible, and urged solving the Iranian nuclear issue through dialogue.

- US President Trump posted that Chinese President Xi congratulated him on so many tremendous successes in such a short period of time, while Trump added that the US was in decline two years ago, but is now the hottest nation.

- USTR Greer said they had a lot of successes in rebalancing trade with China and expect to see an agreement for double-digit billions of dollars of agricultural sales to China coming out of the summit. Greer said China is fulfilling its promises on soybean purchases and that China knows there is going to be a certain level of US tariffs on Chinese goods. Furthermore, he cannot commit to a given rate of tariff on Chinese goods and will release findings of trade investigations in weeks, while he stated purchases of NVIDIA H200 chips will be a sovereign decision by China, and that chip export controls were not a major topic in the meeting.

NOTABLE EUROPEAN HEADLINES

- UK Labour NEC decision on allowing Burnham to run in the Makerfield by-election is not as clear cut as many are reporting, according to GB News' Harwood. The vote is said to be on a "knife edge", sources say "everyone is wavering".

- German Economic Ministry said current indicators suggest a significant slowdown in Q2 GDP growth.

NOTABLE EUROPEAN DATA RECAP

- Italian Inflation Rate YoY Final (Apr) Y/Y 2.7% vs. Exp. 2.8% (Prev. 1.7%).

- Italian Inflation Rate MoM Final (Apr) M/M 1.1% vs. Exp. 1.2% (Prev. 0.5%).

CENTRAL BANKS

- Fed's Barr (voter) said smaller Fed balance sheets would likely increase Fed interventions and that reducing liquidity rules to shrink the Fed balance sheet is not a good idea. Barr stated that lowering the liquidity requirement would simply increase stability risks, and if anything, the liquidity requirement should go up, not down. Furthermore, he said they are not in a recession, but there's been little job creation, while he hasn't decided on what to do at the June FOMC meeting.

- Fed's Williams (voter) said Fed independence delivers better economic outcomes, and it is not time to worry about Fed independence, with staff focused on the mission. Williams said the context matters for inflation given its persistence above target, while he is not surprised to see near-term inflation expectations rise and is seeing pretty stable longer-term inflation expectations. Williams noted there is a lot of uncertainty around energy price outlook and that the job market is not "hot" but also not slowing dramatically, while he added that monetary policy is mildly restrictive and he doesn't see any reason to hike or cut rates right now.

NOTABLE US HEADLINES

- BofA weekly flow data shows USD 20.5bln into stocks, USD 28.1bln into bonds, USD 5.8bln into cash, USD 2.0bln into gold and USD 1.3bln out of crypto. Bull & Bear Indicator rose to 7.6 (from 7.2).

GEOPOLITICS

MIDDLE EAST

- US President Trump said it's just a question of time regarding Iran, while he also stated that current Iranian leaders are more reasonable and Iran has a lot of inner turmoil, but added that he is not going to be much more patient with Iran, according to a Fox News Interview. Trump also stated that Iran's enriched uranium could be entombed, but would rather get it, as well as stated that they have their eyes on Iran's enriched uranium and could bomb it again, but he would rather get it. Trump separately commented that he discussed Iran with Chinese President Xi, and they feel very similar about how they want to end the Iran war.

- US has rejected Iran's 14-point proposal, Tehran Time reported citing sources. According to the information, the US government has responded to Iran's written proposal regarding the end of the war.

- "Perhaps another of the Confidence Building Measures (CBM) between US and Iran is in the play", Pakistani Journalist Mallick posted.

- Iranian Foreign Minister Araghchi said contradictory messages from the US remain the main issue. He added that there is no military solution, and thinks the US needs to understand that fact. They have tested us at least twice and have now concluded that there is no military solution.

- Iranian Foreign Minister Araghchi said at the BRICS meeting that the US empire is in decline and Iran will never bow to pressure, according to Press TV.

- Iranian Foreign Minister Araghchi said evidence shows that the UAE made American bases available for operations against Iran, provided its airspace and territory for those operations

- Iranian Parliamentary Speaker Ghalibaf warned that US efforts at sustaining military escalation near the Strait of Hormuz could trigger a fresh global financial crisis at a time when US national debt already stands at a whopping USD 39tln.

- Iran's Ambassador to Belarus criticised the US negotiation stance and said US President Trump's excessive ambitions hinder US-Iran talks, according to TASS.

- UAE attempted to get Saudi Arabia and Qatar to coordinate on a military response to Iran's airstrikes, Bloomberg reported citing sources.

- Qatar's Foreign Ministry told Al Arabiya it had shot down several Iranian drones near its airspace, while it stressed the need to open the Strait of Hormuz in its contacts with the Islamic Republic.

- Israel has commenced strikes on Hezbollah in the Tyre region of Lebanon.

- Israeli army detected rocket launches from Lebanon towards Israeli territory, while Israeli artillery shelling was reported on the town of Nabatieh al-Fawqa in southern Lebanon.

RUSSIA-UKRAINE

- Commander of Ukrainian drone forces said drones struck Russian oil refinery in the Ryazan region.

OTHER

- US Secretary of State Rubio said China's preference is probably to get Taiwan willingly and that there will be some agricultural purchases from China, while Rubio hoped to get a positive response from China regarding the case of Jimmy Lai and others.

- CIA Director delivered a message from US President Trump that the US is prepared to engage on economic and security issues if Cuba makes fundamental changes, according to a CIA official.

CRYPTO

- Bitcoin pulled back below USD 81k amid sour risk tone.

APAC TRADE

- APAC stocks were mostly subdued after failing to sustain the early momentum that was spurred by the gains on Wall St, where tech outperformed, and sentiment was underpinned amid constructive headlines from the Trump-Xi summit, while the souring of risk sentiment coincided with higher oil prices and yields amid risk that the geopolitical situation in Iran could escalate when US President Trump returns from Beijing.

- ASX 200 lacked direction as strength in tech and financials was offset by losses in mining, materials, resources and utilities.

- Nikkei 225 swung between gains and losses but ultimately continued its pullback from the recent peak amid oil-related headwinds and after hot PPI data further supported the case for a rate hike at next month's BoJ meeting.

- Hang Seng and Shanghai Comp were mixed despite the recent constructive headlines from the Trump-Xi summit, while the leaders are meeting again today in a restricted working lunch session prior to US President Trump's return to the US. Furthermore, sentiment was not helped by recent disappointing lending and aggregate financing data from China for April, which showed a surprise contraction in loans.

NOTABLE ASIA-PAC HEADLINES

- Japan's Minister for Economy, Trade and Industry Akazawa said they can tap FY26 budget reserves if the Middle East impact lasts. However, it was also reported that Japanese Finance Minister Katayama said they are not in a situation where an extra budget is needed, while she stated they have JPY 1tln in reserve funds in the FY26 budget, but added there's no immediate need for an extra budget.

NOTABLE APAC DATA RECAP

- Japanese PPI MM (Apr) 2.3% vs Exp. 0.7% (Prev. 0.8%, Rev. 1.0%).

- Japanese PPI YY (Apr) 4.9% vs. Exp. 3.0% (Prev. 2.6%, Rev. 2.9%).