Published: 2 Jun 2026, 10:20 UTC

Newsquawk Desk

US Market Open: Equities broadly supported following constructive US-Iran comments

0:00--:--

- US President Trump told ABC News he thinks he will have an agreement with Iran to extend the ceasefire and reopen the Strait of Hormuz over the next week.

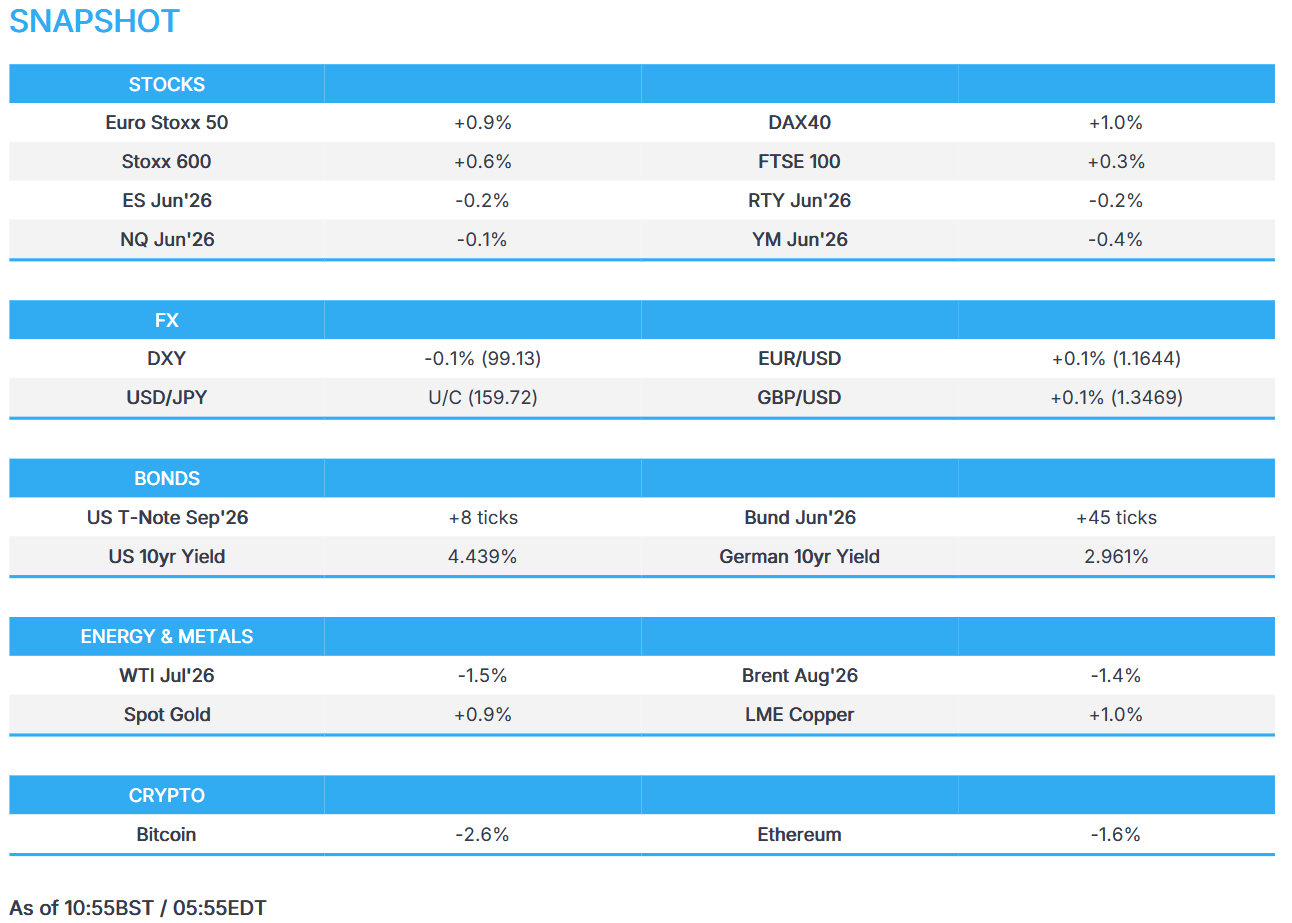

- US equity futures lack direction just shy of ATHs, while European bourses reverse Monday's losses.

- Global benchmarks benefit from lower energy prices, JGBs outperform following a solid 10yr auction.

- DXY muted, EUR directionless as EZ CPI surpasses 3%.

- Crude (Brent -1.4%) falls over renewed hopes of an Iran resolution.

- Looking ahead, highlights include US JOLTs Job Openings (Apr), RCM/TIPP Economic Optimism, New Zealand Export/Import Prices (Q1), NBP Policy Announcement (Jun). Speakers include Fed’s Hammack, BoE’s Bailey & Greene, ECB’s Vujcic. Earnings from Dollar General, Palo Alto & ULTA Beauty.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.7%) start Tuesday’s trade with broad gains after raised hopes of an imminent US-Iran deal. US President Trump said negotiations with Tehran were continuing and signalled expectations of a deal to extend the ceasefire and reopen Hormuz "over the next week". Furthermore, Trump also claimed Israel and Hezbollah had agreed to stop shooting, which further weighed on energy prices and boosted the global risk tone.

- European sectors highlight the positive bias. Technology (+2.7%) tops the sector pile, with Basic Resources (+2.2%) following closely behind as metals surge amid worries of a tighter global supply. Energy (-0.7%), Healthcare (-0.6%) and Food, Beverages & Tobacco (-0.4%) are the only sectors printing modest losses.

- US equity futures (ES -0.2%, NQ -0.1%, RTY -0.2%) trade with very modest losses as prices continue to grind to new ATHs daily.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed but mostly stronger against the Buck as energy benchmarks pull back alongside more constructive Gulf headlines.

- The Buck trades a touch lower after pressure seen in the early European morning attempted to push the Dollar index to the 99.00 level. Markets are generally more risk-on after headlines overnight were more constructive than those seen on Monday. See 08:20 BST headline for geopolitical specifics. US domestic newsflow has been light. Today sees the release of JOLTS job openings. The figure is expected to be broadly unchanged from the March figure. DXY trades 0.1% lower within a 99.05-9922 range.

- EUR is a touch firmer against the weaker Buck in a reaction you would expect to see in response to the recent geopolitical headlines. The EZ Inflation report held a hawkish skew, with the energy component and Services jumping. The single currency was little moved on the report, given it ultimately plays in favour of a hike in June, which is ultimately fully priced in.

- JPY is incrementally lower vs the USD. Japan saw strong demand at its 10yr auction overnight, where demand rose beyond the 12-month average despite the BoJ slated to hike rates in two weeks. JPY saw modest strength on the results, though it proved fleeting with USD/JPY rangebound given the various fiscal/Terms of Trade headwinds. In a note this morning, ING wrote "The risk of new intervention does look a bit underpriced, considering Japanese authorities have remained rather hawkish with their intervention narrative." Katayama was on the wires overnight, she said: "Closely coordinating with the US on FX."

FIXED INCOME

- Global fixed benchmarks are stronger across the board, facilitated by a pullback in energy prices after some positive-leaning geopolitical newsflow. In brief, President Trump suggested that talks with Iran are continuing at a rapid pace, adding that he thinks an agreement will be made with Iran to extend the ceasefire over the next week.

- As for price action, USTs benefit from the lower energy prices this morning, with gains of c. 8 ticks at pixel time; currently holds at the upper end of a 109-22 to 109-30 range (vs Monday’s trough of 109-09+). From a yield perspective, rates at the belly of the curve are underperforming vs short-dated rates, signalling that traders remain uncertain about near-term geopolitical progress. The 10yr (4.43%) now resides back towards recent troughs, and another leg lower could see a test of the low from 12 May at 4.41%. Focus ahead turns to US JOLTS.

- Bunds (+50 ticks) and Gilts (+60 ticks) also extend higher, following the geopolitical risk tone. For the EZ specifically, a hawkish inflation report out of the EZ (Services at 3.5% from 3.00%, and Core Y/Y topped expectations), led to some mild pressure in German paper.

- JGBs (+92 ticks) are outperforming vs peer, boosted by the geopolitical tone and a solid 10yr Japanese auction. Whilst the b/c and avg. yield were not so good, the lowest accepted price fell to 98.01 (prev. 98.86), indicating some solid demand for the paper. The 10yr knee-jerked higher following the sale, before then gradually moving higher as other investors also bought debt. As it stands, the 10yr (2.57%) now resides at levels not seen since 13 May 2026.

- Germany sells EUR 3.857bln vs exp. EUR 5bln 2.50% 2028 Schatz: b/c 1.58x (prev. 1.4x), average yield 2.59% (prev. 2.70%), retention 22.86% (prev. 22.8%).

- UK sells GBP 3.25bln 4.625% 2037 Green Gilt: b/c 3.63x, average yield 4.975%, tail 0.2bps.

- Japan sells JPY 1.98tln 10yr JGBs, b/c 3.53x (prev. 3.90x, 12-month avg. 3.35x), average yield 2.649% (prev. 2.540%).

COMMODITIES

- Crude futures are subdued this European morning as the complex takes a breather from yesterday’s surge, with upside capped by constructive comments from US President Trump. To recap, US President Trump said talks with Iran were continuing at a rapid pace and that he believes an agreement to extend the ceasefire and reopen the Strait of Hormuz could be reached within the next week. That being said, it was reported this morning that Iran’s final text is still being discussed in Tehran and no response has been sent yet; Mehr News reported, citing sources. Meanwhile, a senior Iranian official said renewed war with the US is 'inevitable', Arab News reported, citing state TV. Elsewhere, Lebanon emerged as a major issue, with Iran warning that continued Israeli actions could impact negotiations.

- WTI and Brent front-month futures trade softer by some 2% and 1.8% respectively, at the time of writing after the benchmarks settled higher by USD 4.80/bbl and USD 3.86/bbl, respectively, on Monday. Benchmarks have held a negative bias throughout the European morning. WTI Jul resides towards the bottom end of a USD 90.15-92.65/bbl range, Brent Aug trades in a USD 90.66-92.85/bbl range. Dutch TTF trades -2.5% within the recent EUR 47-48/MWh range.

- Spot gold is slightly firmer as the USD remains subdued by oil prices, with the yellow metal in a USD 4,463-4,541/oz range, within yesterday’s USD 4,447-4,546/oz range. Spot silver similarly rebounds but tops yesterday’s high (USD 76.29/oz) to currently trade towards the top end of a USD 74.48-76.93/oz range.

- Base metals are firmer across the board amid the softer USD and softer oil prices, coupled with a firm performance across Chinese markets overnight. 3M LME copper resides in a narrow USD 13,821.53-13,992.22/t range at the time of writing.

- The IEA’s oil division chief said oil supplies from the US, Brazil, Argentina and Venezuela have exceeded expectations, but output from the Americas can only marginally offset supplies lost East of Suez.

- UAE's ADNOC executive said China’s demand is starting to come back, and "teapot" refineries are showing appetite.

TRADE/TARIFFS

- White House released a Fact Sheet stating President Trump signed a Proclamation adjusting certain metals tariffs to more effectively address national security threats and spur investment. The Proclamation adjusts the tariffs on agricultural equipment, like combines and harvesters, as well as certain other equipment, from 25% to 15%, while it expands the category of industrial equipment subject to a 15% tariff to include mobile industrial equipment, like bulldozers and forklifts, when imported from trade deal countries that are entitled to such treatment. It also encourages foreign companies to use more US steel and aluminium by allowing them to qualify for a 10% duty rate if their capital equipment includes at least 85% US melted and poured or smelted and cast steel or aluminium by weight.

- US Trade Representative said they determined that Brazil has performed unreasonable acts under Section 301 and that the acts are actionable, while the US continues to engage with Brazil to seek a resolution, and the US will hold a hearing about proposed action on June 6th. USTR later proposed to impose tariffs of 25% on all imports from Brazil, except for goods that are subject to Section 232 national security tariffs.

- European Parliament’s Trade Committee voted in favour of legislation to remove EU duties on several US goods imports.

NOTABLE EUROPEAN HEADLINES

- EU is weighing fiscal flexibility for energy costs, while the proposal would allow countries budgetary leeway to cushion energy costs, according to Bloomberg.

- US is in talks to expand nuclear weapon deployments in Europe, according to FT.

- UK Labour leader candidate Andy Burnham said he rules out an early General Election if he is elected to replace PM Starmer, Bloomberg reported citing his spokesperson.

- UK's Ofgem is seeking views on draft guidance to support proportionate supply chain security risk management in the downstream gas and electricity sector.

NOTABLE EUROPEAN DATA RECAP

- EU Inflation Rate YoY Flash (May) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3%, Low. 3%, High. 3.5%); Services 3.5% (prev. 3.00%).

- EU Inflation Rate MoM Flash (May) M/M 0.1% (Prev. 1%).

- EU Core Inflation Rate YoY Flash (May) Y/Y 2.5% vs. Exp. 2.3% (Prev. 2.2%, Low. 2.2%, High. 2.6%).

- EU Core Inflation Rate M/M 0.2% (Prev. 0.90%).

- UK Mortgage Approvals (Apr) 65.94K vs Exp. 62K (Prev. 63.53K).

- UK BoE Consumer Credit (Apr) 1.859B (Prev. 1.895B).

CENTRAL BANKS

- ECB's Rehn says a June rate move would be an insurance hike and that inflation expectations remain unanchored.

- ECB's Simkus said consumer short-term inflation expectations are similar to 2022 and that it is important to react in a timely manner to inflation.

- Rabobank maintains its forecast for a 25bps ECB rate hike next week; expects the ECB to raise rates by another 25bps, likely in September.

- RBA's Harper said stronger than expected domestic demand and re-emergence of capacity constraints have widened the output gap again, and markets are now anticipating that the bank would have to address this, while he added that persistent inflation is a genuine concern and market measures of inflation have gone up, which is a worry.

- Nikkei reported that the BoJ is continuing to call for a June hike, though the government is opting for a "wait-and-see" approach given the risks of risking inflation and a weaker JPY.

- BoJ summary of meeting with investors: one participant said the need for further tapering of bond purchases is not high; participant said there is no need for further tapering of bond buying. One participant said the BoJ should act nimbly, such as conducting emergency bond-buying operations as needed when the bond market destabilises.

GEOPOLITICS

IRAN CONFLICT

- US President Trump told ABC News he thinks he will have an agreement with Iran to extend the ceasefire and reopen the Strait of Hormuz over the next week, while he also stated that a peace agreement with Iran could be better than a military victory. Trump also stated that it's not simple for both sides, but they're getting what they need to get and that he still has to get a few more points.

- US President Trump said he had a very productive call with Israeli PM Netanyahu and that there will be no troops going to Beirut, while he added that Hezbollah agreed that all shooting will stop.

- US President Trump reportedly lashed out at Israeli PM Netanyahu over Israel's escalation in Lebanon in an expletive-laden call on Monday, according to Axios, citing two US officials and a source briefed on the call.

- Iran’s final text is still being discussed in Tehran and no response has been sent yet, Mehr News reported citing sources.

- Iranian Parliament Speaker Ghalibaf said talks will halt if Israeli actions persist in Lebanon, and warned that Iran will confront Israel if atrocities in Lebanon continue.

- A senior Iranian official said a renewed war with US 'inevitable', Arab News reported citing state TV.

- Iran's IRGC reported targeting a US-owned commercial vessel with a cruise missile, according to Al Jazeera.

- Iran's IRGC said 24 ships passed through the Strait of Hormuz in the last 24 hours after obtaining permission from Iran, Nour News reported.

- "A number of vessel owners are saying that they are no longer receiving IRGC threats via the radio, which wasn’t the case a few weeks back. But still the confidence level in crossing is low", Kpler's Bakr posted.

- Lebanon officials said Hezbollah and Israel agreed to the US proposal for mutual cessation of hostilities. Israel will stop strikes on Beirut southern suburbs under the proposed agreement, Press TV reported.

- Israeli airstrikes target sites in southern Lebanon, Sky News Arabia reported.

- Source close to Yemen's Houthis emphasised they will not allow Lebanon to be attacked and Hezbollah to fight alone, according to SNN.

RUSSIA-UKRAINE

- Russia's Kremlin said systematic strikes against Ukrainian military infrastructure are being carried out, however reiterated that it is ready to achieve its aims in Ukraine through diplomacy.

- Explosions were reported in Kyiv, and a witness said the city sustained a large-scale air bombardment, while Ukraine's air force said it detected missiles headed towards the Sumy region and Kyiv, as well as UAVs that were headed towards Zaporizhzhia from the south.

- Air raid sirens were activated in Ukraine's Kyiv, while authorities urged residents to seek shelter.

- Ukraine’s military said it has struck Russia’s Ilsky oil refinery (132k-138k BPD).

CRYPTO

- Bitcoin slipped below USD 70k for the first time in nearly two months following Strategy's (MSTR) USD 2.5mln token sale.

APAC TRADE

- APAC stocks were mixed following the choppy performance stateside, where the major indices ultimately finished mostly higher amid tech strength and mixed geopolitical updates.

- ASX 200 was subdued amid weakness in real estate, financials and defensives, while sentiment was also not helped by a slew of mostly weaker-than-expected data releases.

- Nikkei 225 slipped after printing a new all-time high at the open with very few fresh catalysts from Japan, and as the recent mixed geopolitical headlines provide an opportunity to book profits.

- Hang Seng and Shanghai Comp conformed to the mixed picture with the mainland flat, while the Hong Kong benchmark was led higher by strength in the big tech names, with Meituan underpinned post-earnings, while Tencent, Alibaba, Lenovo, Kuaishou, SMIC and JD were all among the top performers.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama refrained from commenting on FX intervention and current FX levels, while she said volatility in oil markets remain and prepared to take appropriate action. Closely coordinating with the US on Forex, and both sides are closely monitoring markets.

NOTABLE APAC DATA RECAP

- South Korean Inflation Rate YoY (May) Y/Y 3.1% (Prev. 2.6%).

- South Korean Inflation Rate MoM (May) M/M 0.5% (Prev. 0.5%).