Published: 4 Jun 2026, 10:35 UTC

Newsquawk Desk

US Market Open: Dollar and Crude pull back, ES and NQ weighed on by AVGO and CRWD earnings

0:00--:--

- An informed source to Al Arabiya said the agreement on the release of frozen Iranian funds in its final stages, but the search continues for a mechanism on frozen funds. However, US President Trump informed the mediators of his refusal to release funds to Iran before signing the agreement.

- Israel and Lebanon agreed to a ceasefire in US-brokered talks, with the ceasefire contingent on Hezbollah's evacuation from the Litani. Despite this, there have been reports of continuing attacks in Southern Lebanon.

- US equities mixed as disappointing AVGO and CRWD earnings weigh on NQ and ES.

- Fixed income benchmarks gain by a handful of ticks ahead of Friday's NFP.

- DXY softened; JPY saw fleeting strength following hawkish BoJ reports, CHF firmer despite softer CPI data.

- Crude slips as efforts for a US-Iran deal continue.

- Looking ahead, highlights include Jobless Claims (May/30), Revelio PLS (May), Chicago Fed Labor Market Indicators Final (May), Speakers include BoE’s Bailey, Fed’s Daly, Bowman & Barkin, Earnings from Docusign, lululemon & Ciena.

IRAN CONFLICT

- US President Trump said they have been hitting Iran pretty hard and Iran negotiations are going well, while he suggested a deal could happen over the weekend and said anything can happen when you are dealing with Iran, but also stated it could go another two or three weeks. Trump also stated he would rather not use the military in Iran, and would rather not wipe Iran out, as well as noted that they are close to signing papers in theory. Furthermore, Trump said they are trying to separate Iran and Lebanon issues, while he responded that in that part of the world, a ceasefire is when you're shooting in a more moderate manner, when questioned about the ceasefire.

- US President Trump told aides privately that he would consider ending the ceasefire with Iran if US troops are killed, according to WSJ.

- An informed source to Al Arabiya said the agreement on the release of frozen Iranian funds in its final stages but the search continues for a mechanism on frozen funds. US President Trump informed the mediators of his refusal to release funds to Iran before signing the agreement. The source notes that the main obstacle relates to the mechanism for disposing of part of the frozen Iranian funds and there is a proposal to create a special fund for depositing frozen Iranian funds that is under discussion.

- Sources noted that the first phase of the interim agreement between the US and Iran involves cessation of direct military operations, phase 2 is a full reopening of maritime traffic, phase 3 includes limited easing of some sanctions and phase 4 includes major issues such as the Iranian nuclear program, according to Al Hadath.

- Pakistani Foreign Minister, on reports of halted US-Iran talks, said "Our dialogue process continues”, Pakistani journalist Mallick posted.

- Israel and Lebanon agreed to a ceasefire in US-brokered talks, with the ceasefire contingent on Hezbollah's evacuation from the Litani, while Lebanese armed forces will take control of pilot zones, and Israel and Lebanon agreed to reconvene negotiations in the week of 22nd June.

- US State Department confirmed Israel and Lebanon agreed to the implementation of a ceasefire and that the sides agreed with guidance of the US to swiftly advance creation of pilot zones in which Lebanese armed forces will take exclusive control of the territory. Israel and Lebanon also reaffirmed they have no hostile intent towards one another and are committed to continuing negotiations.

- Lebanese President said the implementation of the ceasefire could begin within 24 hours of final approval, Arab News reported.

- The Israeli army has begun withdrawing its forces from Dibbin in southern Lebanon, Al Hadath reported.

- Israeli Defence Minister said the IDF will continue its operations on the ground in Lebanon at this stage, Al Hadath reported. "The Lebanese will not return to the south and we will continue to destroy infrastructure."

- Israeli military said fighting in Southern Lebanon continues.

- Israeli airstrikes were reported in several areas in southern Lebanon, according to SNN.

- Hezbollah attacked Israeli positions in southern Lebanon.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.1%) started the European morning on a positive footing, as markets digested positive geopolitical updates from President Trump and a Lebanon-Israel ceasefire. However, markets have since soured amidst reports that Israel were conducting operations in Lebanon, and following the negative action seen across the pond.

- European sectors are mixed. Retail (+1.7%) continues to gain following the earnings by Inditex on Wednesday. Consumer Products & Services (+1.7%) and Travel & Leisure (+1.2%) round out the top 3. The laggards include Telecoms (-1.6%), Media (-1.6%) and Basic Resources (-1.1%).

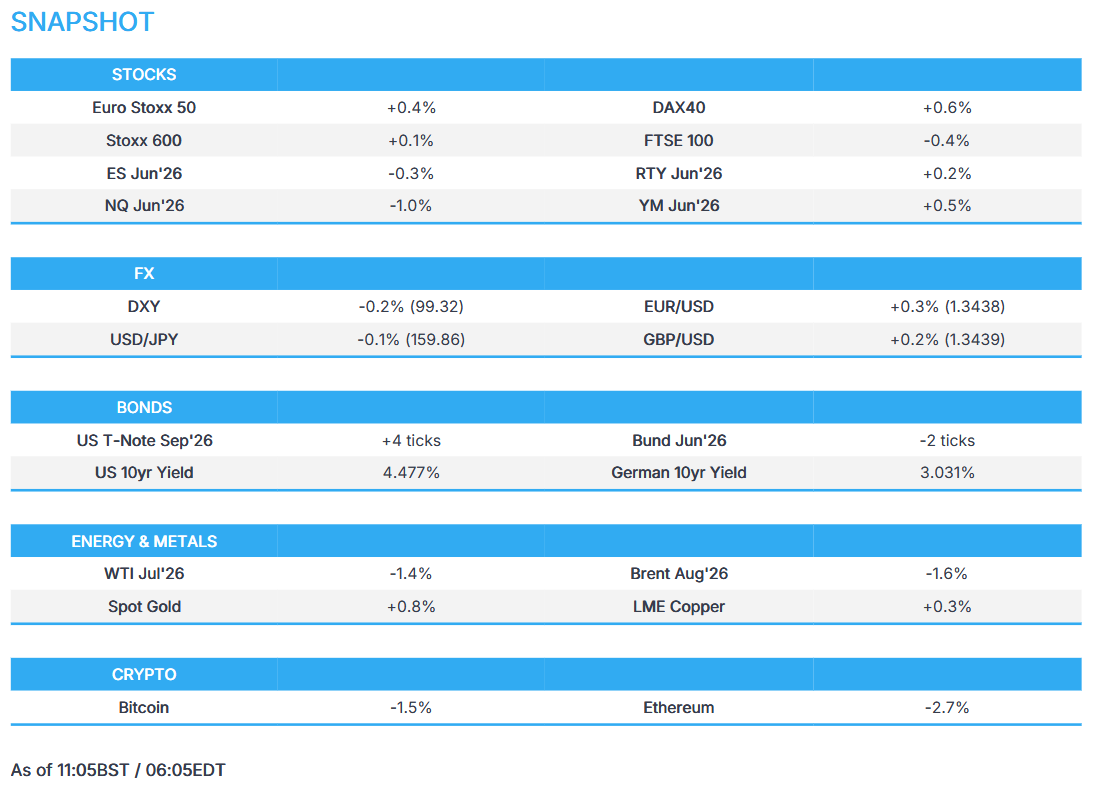

- US equity futures trade mixed, with losses in Broadcom (-12% pre-market) and CrowdStrike (-11% pre-market) weighing on the NQ (-1.0%) and ES (-0.3%), while RTY (+0.3%) and YM (+0.5%) print modest gains.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- The Buck is lower this morning vs initially starting the European morning flat. Not really any geopolitical market-moving headlines overnight; however, the Buck was pushed lower after hawkish BoJ sources (see below). In terms of Fed speak since the close, Williams said he sees no obvious direction for rates and no reason to change them. Logan said higher rates could be needed later this year. Ahead, Daly, Bowman & Barkin are slated to speak.

- JPY is slightly firmer and trading in line with most G10s. Sources told Bloomberg and Reuters that the BoJ would raise rates at the June meeting, with the Bloomberg piece suggesting more tightening was possible in 2026. Markets assign 20bps of tightening in June (80% probability), with an additional 20bps implied by year-end. The BBG report saw a 35-pip move lower in USD/JPY over ten minutes, which ultimately proved fleeting, with Yen fundamentals remaining bearish and two hikes close to being fully priced this year. A strategist at SMBC Nikko Securities said: “Even if the BoJ raises rates in June, any rebound in the yen will be limited”. USD/JPY trades higher by 0.1%, a touch below the 160.00 mark.

- CHF is performing well against the Euro and Buck after CPI metrics from Switzerland. Although a cooler-than-expected report is unlikely to shift the dial for policymakers at the SNB. This is because the headline remains towards the lower half of the 0-2% target band, and the SNB continues to make clear that inflation meets its medium-term stability objective. As such, policy is expected to remain at the ZLB for the foreseeable future. EUR/CHF -0.1% at 0.9181, USDCHF -0.3% at 0.7896.

FIXED INCOME

- Global fixed benchmarks are mixed as energy prices cool a touch after President Trump said Iran negotiations are going well, while he suggested a deal could happen over the weekend. Though noted that it could go another two or three weeks. Separately, reports suggest that Israel and Lebanon agreed to a ceasefire, though recent reports have suggested that the Israeli army is continuing its operations in the region. This uncertainty has led to the tentative action across fixed paper this morning.

- USTs (+4 ticks) are slightly firmer and trade within a narrow 109-12+ to 109-19+ range. Really not much driving the action this morning aside from geopolitics, but domestic data will likely garner some attention later. To recap, ISM Manufacturing & Services indicate a solid activity picture, with labour market reports (ADP/JOLTS) also pushing back on near-term rate cut expectations. Ahead, focus will be on: Jobless Claims (May/30), Revelio PLS (May), and Chicago Fed Labor Market Indicators Final (May).

- JGBs (-20 ticks) are on the back foot this morning for two key reasons: a) hawkish BoJ reports, b) an enhanced-liquidity auction. Delving into the report, Bloomberg first reported that the BoJ is mulling a hike in June, and potentially one more this year. Moreover, a source said that the Bank sees less need to pare back its bond purchasing plans. This was later corroborated by a Reuters piece, where a source said, “Unless there's a severe escalation in the conflict, the BOJ will probably hike rates in June”. Before the sources piece, markets already expected the Bank to hike in June; therefore, the pressure in JGBs this morning stems from comments related to the plans later in the year.

- Bunds and Gilts follow the tentative action seen in USTs, but are lower by a handful of ticks. Domestic updates for EZ have been lacking this morning, but traders will eye Retail Sales. Irrespective of the report, the ECB is set to hike at the June meeting – money markets assign a 96% chance of such a decision; another hike is then priced in for October.

- France sells EUR 13.998bln vs exp. EUR 12-14bln 3.70% 2036, 4.00% 2038, 3.60% 2042, 4.40% 2057 OAT.

- Spain sells EUR 4.973bln vs exp. EUR 4.5-5.5bln 2.35% 2029, 3.10% 2031 and 3.50% 2041 Bono and EUR 0.593bln vs exp. EUR 0.25-0.75bln 2.05% 2039 I/L Bono.

COMMODITIES

- Crude markets are on a softer footing amid ongoing mediation efforts to broker some sort of US-Iran deal following two flare-ups earlier this week. In terms of the major updates, US President Trump said negotiations with Iran were progressing and suggested a deal could come within days, although talks could also continue for several more weeks. Meanwhile, US Secretary of State Rubio said the US is awaiting Iran’s final sign-off on negotiations surrounding Tehran’s nuclear programme. On the other side, Iranian officials outlined a four-stage framework for a potential agreement with the US. The four-stage proposal for a deal with the US includes: 1) Ending the war, 2) tangible measures re. the Strait, 3) sanctions and nuclear issues, 4) the establishment of a supervisory committee. More recently, Al Arabiya reported that the agreement on the release of frozen Iranian funds is in its final stages, albeit the search continues for a mechanism for frozen funds. The sources added that Trump informed the mediators of his refusal to release funds to Iran before signing the agreement. Elsewhere, Israel and Lebanon agreed to implement a US-brokered ceasefire framework and continue negotiations, although since the ceasefire, Hezbollah and IDF continued to exchange fire in the south of Lebanon.

- WTI Jul and Brent Aug futures are subdued in USD 94.06-95.91/bbl and USD 95.61-97.44/bbl ranges, respectively, at the time of writing, with fleeting downside seen on the aforementioned Al Arabiya sources. Dutch TTF ekes mild gains (+0.2%) but trades choppy on either side of EUR 49/MWh. “Positioning data for TTF continues to show that investment funds have been somewhat unfazed by ongoing LNG supply disruptions in the Middle East amid optimism over a resumption of LNG flows through the Strait of Hormuz”, analysts at ING write.

- Spot gold and silver are firmer after yesterday's losses, with the yellow metal finding support this morning at its 200 DMA (USD 4,423/oz) before rebounding to trade in a current USD 4,423-4,484/oz range. Spot silver trades in a USD 72.45-73.91/oz range, still some way off yesterday’s peak at USD 75.33/oz.

- Base metals are mostly lower amid the broader cautious risk tone. 3M LME copper ekes mild gains but remains under USD 14,000/t in a USD 13,701.13- 13,849.00/t at the time of writing.

- Russian Deputy PM Novak said Russia expects to reach its OPEC+ oil production quota this year. The oil market has not yet fully seen the consequences of the Middle East conflict, and stockpiles are being used. There has been no oil production lower than the start of the year due to “unscheduled maintenance” at refineries.

- Russian Deputy PM Novak said OPEC+ countries do not plan to share the UAE's oil output quota.

- Russia's Investment Fund Head Dmitriev said the EU is already going to make a number of concessions to Russia on energy as they need this for survival, TASS reported.

- China to lower retail gasoline prices by CNY 525 per metric ton from June 5th.

TRADE/TARIFFS

- China's MOFCOM said the US abuse of export controls is disrupting stability in the global semiconductor production and supply chain and opposes US trade restrictions on China justified by "forced labour".

NOTABLE EUROPEAN HEADLINES

- UK PM Starmer is considering watering down plans to boost defence spending by GBP 18bln over concerns that they are unaffordable, according to The Times.

NOTABLE EUROPEAN DATA RECAP

- EU Retail Sales MoM (Apr) M/M -0.4% vs. Exp. -0.3% (Prev. -0.1%, Low. -0.5%, High. 0.4%).

- EU Retail Sales YoY (Apr) Y/Y 1.0% (Prev. 1.2%).

- Swiss Inflation Rate YoY (May) Y/Y 0.6% vs. Exp. 0.8% (Prev. 0.6%, Low. 0.7%, High. 1%).

- Swiss Inflation Rate MoM (May) M/M 0.2% vs. Exp. 0.3% (Prev. 0.3%, Low. 0.2%, High. 0.5%).

- Swedish CPIF YoY Prel (May) Y/Y 1.5% vs. Exp. 1.2% (Prev. 0.8%).

- Swedish CPIF MoM Prel (May) M/M 0.9% vs. Exp. 0.6% (Prev. -0.6%).

- Swedish Inflation Rate YoY Prel (May) Y/Y 0.8% vs. Exp. 0.5% (Prev. -0.1%).

- Swedish Inflation Rate MoM Prel (May) M/M 1.0% vs. Exp. 0.7% (Prev. -0.6%).

CENTRAL BANKS

- Fed's Logan (2026 voter) said she is increasingly concerned higher interest rates could be necessary later this year and monetary policy is not restraining the economy, while she added that inflation is taking too long to return to 2%, economic activity remains strong and corporate earnings are 'going gangbusters'. Logan said financial conditions are accommodative, and the labour market is stable, but separately noted that the higher price of gas is feeding through to prices of other goods and services. Furthermore, she stated that mildly restrictive policy is needed and that the current monetary policy looks neutral or loose.

- RBA Governor Bullock said the RBA expects inflation to increase further in the near term and notes flow of data and development since May has not been materially different to our expectations. She notes that inflation is too high, and the board will do what it considers necessary to achieve its mandate of delivering price stability and full employment. Some signs of tightening impact already seen, but full effects to take 1 to 2 years.

- BoJ is said to mull a June rate hike with another possible in 2026 and sees less need to cut bond buys at the same pace in FY27, according to Bloomberg source reported. Reuters then corroborated this report.

NOTABLE US HEADLINES

- US Challenger Job Cuts (May) 97.006K (Prev. 83.387K); May Job Cuts Rise 16% from April, the highest May total since 2020.

- US House backed a resolution curbing Trump's Iran war powers with the House voting 215 to 208 to pass the War Powers resolution.

- US President Trump is to announce nearly USD 700mln in coal support and to use the Defence Production Act for the coal sector, according to Axios.

- US President Trump is expected to nominate acting AG Blanche as Attorney General.

- US Agricultural Secretary Rollins announced additional USDA personnel deployment to South Texas, and urged livestock producers to remain vigilant, while she stated that potential New World screwworm detection is being fully contained and is not a harm to US food supply or safety.

GEOPOLITICS

OTHER

- North Korean leader Kim plans to significantly boost the nation's national nuclear capabilities, according to KCNA.

CRYPTO

- Bitcoin continues to slump and is set for its worst week since the start of 2025, slipping below the USD 63k handle.

APAC TRADE

- APAC stocks were lower following the negative handover from the US, where risk sentiment was weighed on by the recent retaliatory attacks between the US and Iran, as well as weakness in tech stocks.

- ASX 200 was pressured by underperformance in the mining and materials industries, while most sectors were subdued aside from the resilience in defensives.

- Nikkei 225 retreated from record levels and briefly tested the 67,000 level to the downside amid intervention risks following FX comments from Japanese PM Takaichi, while comments from BoJ Governor Ueda signalled the central bank could resume rate normalisation this month. On that front, hawkish BoJ sources noted the central bank is to mull a hike this month, with another possible in 2026.

- Hang Seng and Shanghai Comp conformed to the downbeat mood amid tech-related headwinds and with the PBoC refraining from open market operations for a second consecutive day.

NOTABLE APAC DATA RECAP

- Australian Balance of Trade (Apr) 1.791B vs. Exp. -1.61B (Prev. -1.841B).

- Australian Imports MoM (Apr) M/M 0.8% (Prev. 14.1%).

- Australian Exports MoM (Apr) M/M 7.2% (Prev. -2.7%).