Published: 11 Jun 2026, 10:10 UTC

Newsquawk Desk

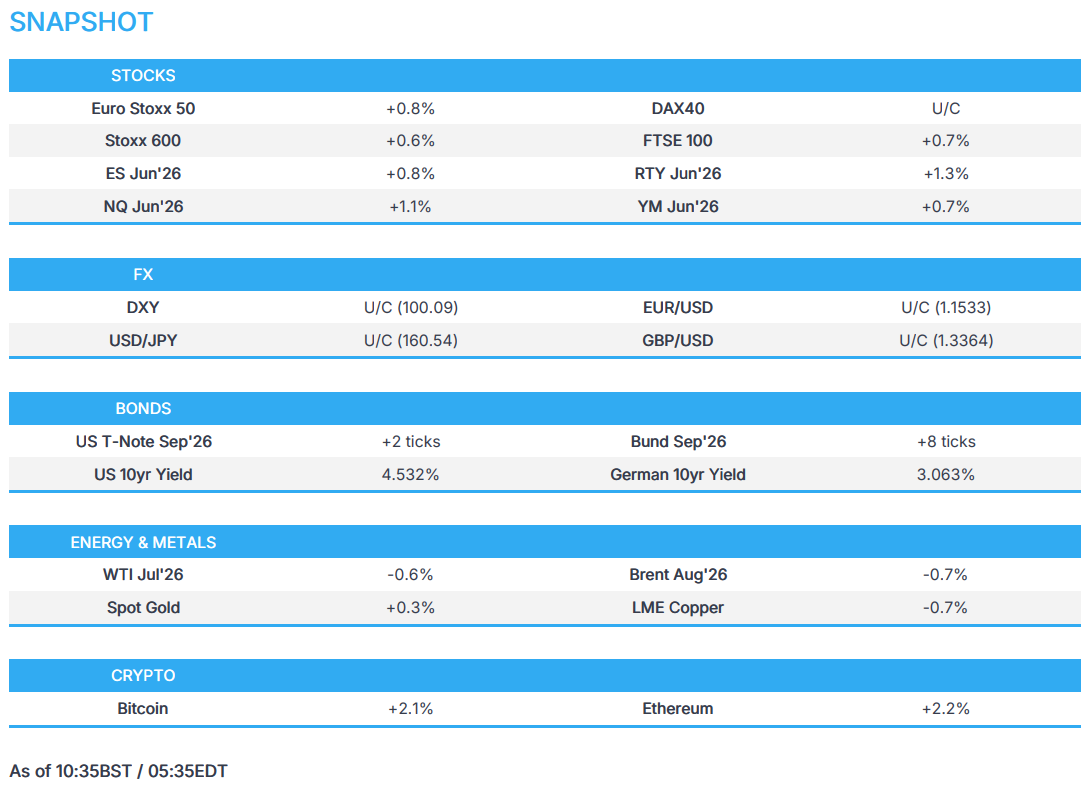

US Market Open: Energy benchmarks weaker as US-Iran diplomacy continues, ECB and US PPI due

0:00--:--

- The US and Iran exchanged another round of strikes overnight, resulting in Iran announcing the complete closure of the Strait of Hormuz, effective immediately, and threatening to hit any vessel crossing the Hormuz.

- However, an Iranian source told Reuters that Iran and the US are still in negotiations over a preliminary deal, which includes a mechanism for unfreezing funds.

- US equity futures pare Wednesday's losses ahead of SPCX IPO pricing.

- DXY flips across the 100.00 handle; EUR muted ahead of ECB policy announcement.

- Fixed income muted, US 10yr remains above 4.50% with PPI ahead.

- Crude futures reverse earlier gains amid positive reports of continued US-Iran negotiations.

- Looking ahead, highlights include US PPI (May), Jobless Claims (May/30), ECB Policy Announcement (Jun), CBRT Policy Announcement (Jun), OPEC MOMR (Jun), Comments from ECB President Lagarde, Supply from the US and Earnings from Adobe.

IRAN CONFLICT

- The US carried out fresh strikes against Iran, with US CENTCOM saying that American forces began launching additional self-defence strikes, and then later announcing that it completed the strikes, targeting Iranian military surveillance capabilities, communication systems and air defence sites across Iran. In response, Iran's military command centre announced the Strait of Hormuz would be closed to all vessels, effective immediately, and threatened to hit any vessels crossing the strait. Iran's IRGC also said it launched two waves of retaliatory strikes, hitting and destroying 18 key military targets in US bases in Kuwait and Bahrain.

- Following the overnight strikes, an Iranian source told Reuters that Iran and the US are still in negotiations over a preliminary deal, which includes a mechanism for unfreezing funds. This followed commentary by the Pakistani Foreign Minister stating that we remain engaged with a degree of optimism. The minister added that channels of communication remain open and Pakistan and Qatar remain engaged in mediation efforts. To add, CNN reported first, citing a source, stating that US-Iran talks still continue despite US-Iran military exchange.

- US President Trump said on Wednesday evening that fighter jets were operating over the skies of Iran, and he spoke directly with Iranian officials. Trump added that Iranians asked him to stop bombing, while he said the bombing will stop shortly, but left the option open for more strikes. Trump also stated that Israelis were not involved in Iran strikes and that the US fired 49 Tomahawk missiles, as well as noting that Iran must choose between war or a new deal and warned 'we'll bomb them to rubble tomorrow night' if there is no deal.

- Tasnim cited a reliable source stating that Trump's claim that Iranian officials spoke with him directly and wanted the bombing to stop is completely false, while the source added that no contact has been established with Trump and that Iran responds to aggression with military action.

- US President Trump held a Situation Room meeting on Iran strike options, while sources said one option Trump was considering was launching an operation that is big in scale but short in duration, according to Axios. However, NYT later reported that officials held a Situation Room meeting regarding the Epstein files and that the meeting was held without Trump.

- US Secretary of War Hegseth said Central Command would be busy overnight and that the US would hit Iran hard, with the US to bomb key facilities in Iran, and strikes would be strong and clear.

- IRGC Navy said vessels approaching the Strait of Hormuz is considered cooperation with the enemy and "We warn that no vessel should leave its anchorage in the Persian Gulf and the Sea of Oman", ISNA reported.

- Iran said applicants who have received a transit permit are asked to be patient and await further guidance from the PGSA, IRIB reported and repeated that the Strait remains closed until further notice.

- UKMTO received a report of an incident 21NM Northeast of Sohar, Oman. Iran's Sirik Governor later said the US projectile hit a cargo boat in the Gulf of Oman.

- A 7th vessel carrying Qatari LNG is understood to have transited the Strait of Hormuz, Kpler's Bakr reported.

- India's embassy within Oman said they were informed on Thursday of an incident that involved a vessel in proximity to the Shinas port.

- Israeli airstrike targets a facility in Western Bekaa, central Lebanon, Al Hadath reported.

- Israeli airstrikes reported on towns in southern Lebanon, Al Mayadeen reported.**

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.6%) trade with broad gains despite another round of US-Iran strikes. The US targeted Iranian military surveillance capabilities, communication systems and air defence sites across Iran, while Iran's IRGC said it launched two waves of retaliatory strikes, hitting and destroying 18 key military targets in US bases in Kuwait and Bahrain. Germany's DAX 40 (U/C) underperforms, weighed on by losses in SAP (-4.4%) following Oracle's earnings (see more below).

- European sectors trade mixed. Utilities (+1.3%) tops the list, with Energy (+1.2%) and Banks (+1.2%) round out the top 3. Autos (-0.4%), Real Estate (-0.4%) and Telecoms (-1.0%) are the underperformers.

- US equity futures rebound sharply following Wednesday's losses, with the RTY (+1.3%) leading gains. Oracle (-6.8% pre-market) is lower post-earnings, which is weighing on European peers, as plans to raise additional financing (c. USD 40bln through debt and equity financing) for its AI buildout clouded better-than-expected results and a higher profit forecast.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed against the Buck in relatively thin trade into the ECB meeting and US PPI.

- A busy morning in terms of newsflow, has not translated into price action/vol for G10s which are mixed against the flat Buck. Gradual weakness in Crude benchmarks seen among slew of optimistic US-Iran updates (see feed from 08:21-38 BST), did little to move DXY from its 100.00 handle despite Brent edging to session lows under USD 92/bbl. In short, it appears negotiations continue despite the recent exchange of fire. The Greenback seems less sensitive to geopolitical headlines as markets interpret recent US data with PPI ahead.

- CAD is the worst G10 performers as energy weakness pressures the Loonie. On Wednesday, the BoC held rates at 2.25% with some dovish undertones. Although release and accompanying remarks from Macklem/Rogers were a repeat from April, ING notes its use of language such as “excess supply” and “looking through” inflation may have offered the Loonie. Amid the recent weakness in energy benchmarks, USD/CAD could approach the 1.40 level should US PPI print hot.

- The main EUR event today will be the ECB meeting, where the Governing Council is expected to hike by 25bps, taking the Deposit Rate to 2.25%. This is justified by the assessment that the ECB is past the March baseline and is closer to the adverse scenario. Attention will be on language regarding a July move, where interest rate futures currently assign a 30% probability of tightening. EUR has been moving lower on account for recent USD upside as mentioned above. EUR/USD trades within recent parameters in the middle of a 1.15-16 band. If the ECB indicates further tightening, that could see the pair test resistance at 1.1570/80, whereas a dovish council may see recent lows of 1.15 tested, in conjunction with hot US PPI.

FIXED INCOME

- Global fixed benchmarks are trading tentatively on either side of the unchanged mark. This comes amidst another US strike on Iranian military targets, which led to retaliation from the Iranians. This led energy higher overnight, but then came off best levels as CENTCOM announced the latest bout of attacks are completed. Thereafter, energy benchmarks turned negative after CNN reported that US-Iran talks are continuing. This helped global fixed paper to clamber off worst levels, with the complex generally sitting towards highs.

- USTs (+2 ticks) trade towards the upper end of a 108-27 to 109-06+ range. The trough of the day was formed overnight, which coincided with the peaks in the energy complex. Thereafter, US paper clambered off worst levels, as the geopolitical environment eased. Domestically, focus will be on the US PPI report, which, together with Wednesday's broadly in-line CPI report, will be used as a key determinant for next week’s Fed policy announcement. The policy rate is unlikely to be adjusted, but focus will be on comments pertaining to the easing bias removal. Also on the docket today is a 30yr auction, which follows on from a decent 3yr outing and a strong 10yr auction. This notably comes despite the ongoing volatility and hawkish Fed repricing.

- Bunds (+9 ticks) are trading towards the upper end of a 124.88 to 125.29 range, currently driven by events in the Middle East, though focus will come back to Europe where the ECB is set to deliver a 25bps hike this afternoon. Given markets widely expect a hike, focus will be on the accompanying statement and President Lagarde to see if/how hawkish the Bank shifts. The likelihood is that Lagarde will keep optionality; ING opines that she will want to avoid “sounding too dovish”.

- Gilts (-3 ticks) are essentially flat and trade within a 87.39 to 87.60 range. Ultimately, moving at the whim of geopolitical developments. Domestic newsflow has been light, with some focus on Burnham comments where he suggested he would support Waspi Women, a compensation scheme believed to cost upwards of GBP 10bln. With the UK newsflow light, Gilts will likely take leads from this afternoon’s US PPI and ECB announcement.

- UK sells GBP 5.0bln 2029 Gilt: b/c 3.60x (prev. 3.35x), average yield 4.419% (prev. 4.238%), tail 0.2bps (prev. 0.2bps).

- Italy sells EUR 4.0bln vs exp. EUR 3.5-4.0bln 3.00% 2029 BTP: b/c 1.62x, average yield 3.03%.

COMMODITIES

- The US carried out fresh strikes against Iran, with US CENTCOM saying that American forces began launching additional self-defence strikes, and then later announcing that it completed the strikes, targeting Iranian military surveillance capabilities, communication systems and air defence sites across Iran. In response, Iran's shut the Strait of Hormuz and launched its own attack on some Gulf nations.

- Despite these strikes, an Iranian source tells Reuters that Iran and the US are still in negotiations over a preliminary deal, including a mechanism over unfreezing funds, while the Pakistan Foreign Minister said they remain engaged with a degree of optimism. Prior to that, CNN sources outlined that US-Iran talks continue, despite the US-Iran military exchange.

- Crude futures have completely pared the earlier gains. WTI Jul'26 reversed at the 50-SMA (USD 93.48/bbl) and currently trades at the lower end of its USD 88.77-93.64/bbl range. For Brent Aug'26, the benchmark has slipped below USD 92/bbl (USD 91.72-95.50/bbl range).

- Precious metals rebound following the drop in the last few days, action driven by several previously discussed factors. Spot gold dipped below the March 26th low of USD 4099/oz in Wednesday's session and extended to a trough of USD 4024/oz early in the Asia-Pac day. Since then, the yellow metal has bid higher and now trades at the upper end of its USD 4024-4118/oz range.

- 3M LME Copper gapped lower at the start of trade, following the selloff in APAC equities, but has since oscillated in a USD 13.39k-13.52k/t range.

- Japan's PM Takaichi said that she expects to secure 100% of crude in July, without passing the Strait of Hormuz.

- Shanghai Futures Exchange has adjusted daily price-limit bands and trading margin ratios for gold and silver futures contracts

TRADE/TARIFFS

- China abruptly cancelled two important diplomatic meetings with the EU this month, amid increasing tensions regarding surging Chinese exports to the EU, according to the FT.

NOTABLE EUROPEAN HEADLINES

- France and Germany are discussing proposals for a radical overhaul of the EU’s diplomatic service in an attempt to improve the response to geopolitical crises, according to FT.

NOTABLE EUROPEAN DATA RECAP

- UK RICS House Price Balance (May) -35 vs Exp. -32 (Prev. -34).

- Swedish CPIF MoM Final (May) M/M 0.9% vs. Exp. 0.9% (Prev. -0.6%).

- Swedish CPIF YoY Final (May) Y/Y 1.5% vs. Exp. 1.5% (Prev. 0.8%).

NOTABLE US HEADLINES

- BofA Total Card Spending (w/e 6th Jun) +6.1% (prev. +5.2% W/W, +4.8% in Apr); entertainment, clothing, HI, furniture and transit saw the biggest acceleration.

CRYPTO

- Bitcoin has steadied above USD 60k, currently trading in a USD 61.45k-62.97k range, following the selloff as investors rotate out of crypto ahead of the SpaceX IPO.

APAC TRADE

- APAC stocks declined in a continuation of the recent tech reversal, and as the US conducted strikes on Iran for a second consecutive day, which prompted Iran to retaliate by targeting US bases in the region and ships near the Strait of Hormuz. Iran also declared the waterway closed to all vessels. However, stocks then gradually pared losses given that the fresh strikes were widely telegraphed beforehand and with relief also seen after CENTCOM announced that US forces completed the strikes.

- ASX 200 was pressured with the downside led by underperformance in tech and the top-weighted financials sector, although losses were stemmed by resilience in energy and defensives.

- Nikkei 225 slumped at the open owing to the fresh hostilities in the Middle East, with headwinds seen amid higher oil prices and upside in yields, although the index then staged a recovery and returned to flat territory before a renewed bout of selling persisted.

- Hang Seng and Shanghai Comp followed suit to the weakness across global markets, with several tech stocks clustered among the list of worst performers.

NOTABLE ASIA-PAC HEADLINES

- Japan PM Takaichi and US President Trump are arranging a meeting during the G7, Nikkei reported.

- Japanese Chief Cabinet Secretary Kihara said he doesn't think BoJ Governor Ueda's temporary hospitalisation will affect the BoJ's policy conduct and cooperation with the government.

- PBoC Governor Pan reiterated the depth and breadth of China's financial market, provide key allocation opportunities for overseas institutional investors.

NOTABLE APAC DATA RECAP

- Australian Consumer Inflation Expectations (Jun) 5.5% (Prev. 5.6%).