Published: 17 Jun 2026, 10:20 UTC

Newsquawk Desk

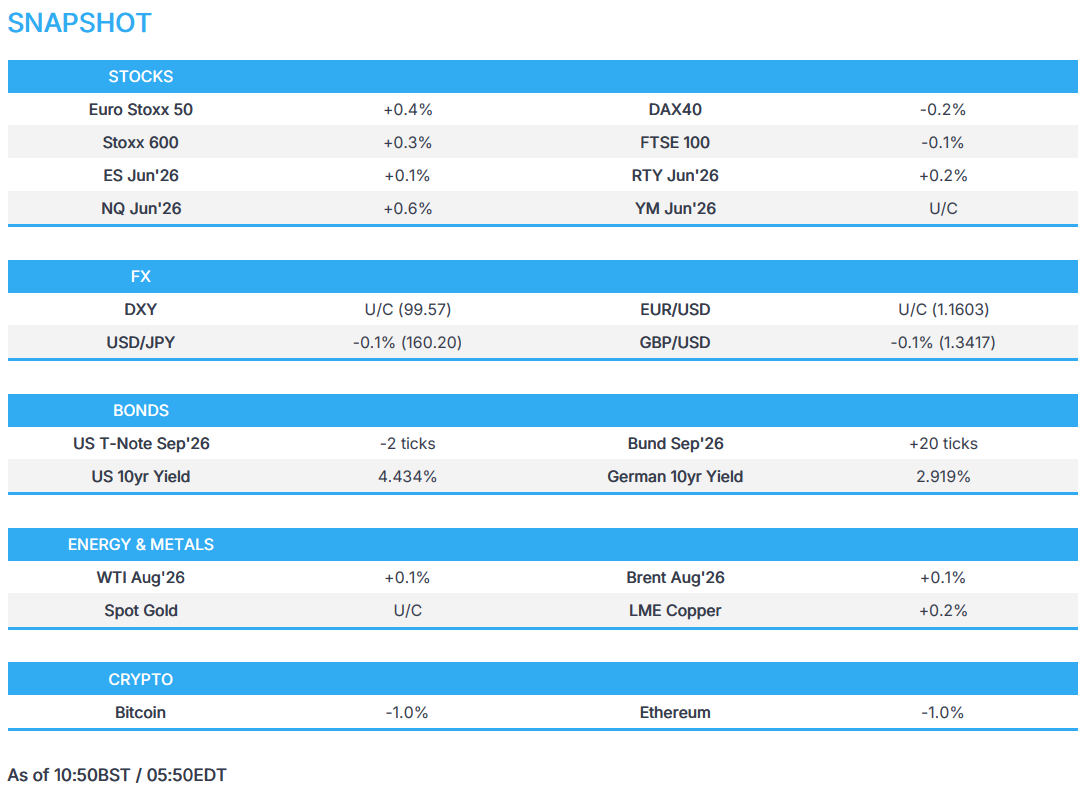

US Market Open: US equity futures gain, GBP weaker after cooler than exp. CPI, USD benefits into FOMC

0:00--:--

- An informed source told Tasnim that Bloomberg's alleged text of the US-Iran MoU is not accurate, but that the finalised text will be published after the signing on Friday. However, it was initially stated that it would not be published.

- US equity futures gain steadily; Germany's DAX 40 underperforms, weighed by BMW's guidance cut.

- DXY flat, G10s mixed; SEK softer despite Riksbank forecasts of a greater chance of a rate hike.

- Fixed income muted, while gilts outperform following cooler-than-expected CPI; Fed announcement ahead.

- Energy benchmarks contained in narrow ranges, as the focus remains on the US-Iran MoU signing.

- Looking ahead, highlights include US Retail Sales (May), Atlanta Fed GDP (Q2), New Zealand GDP (Q1), Fed Policy Announcement, BCB Policy Announcement, Speakers including ECB's Lagarde & Fed's Warsh.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.3%) start Wednesday's trade mixed, with outperformance in the AEX (+0.7%) while the DAX 40 (-0.2%) lags after BMW cut guidance. Geopolitical newsflow has been light thus far as markets await for the official MoU signing on Friday.

- European sectors also lack a clear bias. Technology (+1.2%) and Banks (+0.8%) top the sector pile. Autos (-2.1%) is the worst-performing sector this morning, primarily driven by updated guidance from BMW. The Co. cut its operating auto margin to 1-3% (prev. 4-6%) and said it would intensify cost-cutting, with a negative one-off in the H2'26. Analysts at Deutsche Bank and Jefferies both said the outlook cut was significantly larger than expected, which has resulted in the Co.'s shares slumping as much as 11%. This has dragged peers lower with it (Volkswagen -2.4%, Mercedes-Benz -3.0%)

- US equity futures are muted, except for the NQ (+0.6%). Intel (+4.1%) announced that its 18A manufacturing process has entered risk (i.e. early) production, with the chipmaker seeing strong demand for its central processors.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is on a modestly firmer footing after softening on Monday alongside a decline in yields and lower oil prices. Focus today is overwhelmingly on Warsh’s first FOMC meeting as chair, where the committee is widely expected to keep the federal funds rate unchanged at 3.50-3.75%. Within the meeting, attention will be on language surrounding the easing bias, and the dot plots, which ING believes a removal of the bias alongside a cut to the 2026 dot plot, would support the Buck. Alongside these points, Warsh’s communication will be closely monitored. (Full Fed preview in the Newsquawk Research suite). DXY lacks direction, trading unchanged and supported just above 99.50.

- GBP is a touch lower. In short, a cooler than expected UK CPI print, which falls beneath BoE forecasts on both a headline and core basis, services were also cooler than BoE forecast, but in line/hotter than analyst forecasts, depending on which data vendor is cited. GBP weakened post-data; Cable fell as much as 20 pips to a 1.3408 trough before paring modestly. The pair dipped below its 200DMA at 1.3418.

- Two-way action seen in SEK, which is modestly softer post-announcement despite the forecasts implying a greater chance of a 2026 hike. Pressure that is a function of the fact that the forecasts and statement are based on information up to the 11th of June, as such the fall in energy benchmarks seen in the last few sessions on the US-Iran MOU progress is not accounted for, and therefore the hawkish tilt to the policy forecast is likely to be unwound in the next meeting, if the MOU holds and the energy retreat sticks and/or extends. We may get more details from Governor Thedeen at 10:00BST, and the Minutes on the 24th of June.

FIXED INCOME

- Global fixed benchmarks are mixed, with USTs a couple of ticks lower whilst Bunds and Gilts gain; the latter outperforms after the UK’s inflation held steady in May. Geopolitical updates have been lacking today, with all eyes on the US-Iran deal signing on Friday. However, Iran’s Tasnim, citing a source, suggested that the text will not be published after the signing on Friday. Though, this was later corrected and it will be released.

- USTs (-2 ticks) hold within a 109-26+ to 109-30+ range. Markets are ultimately on tenterhooks ahead of the Fed policy announcement, which will see the debut of Kevin Warsh as Chair. Policy rates are expected to remain unchanged, so focus will be on whether the easing bias will be removed from the statement. Dot plots are seen to show higher inflation and a more cautious policy path, with the new Chair interestingly not expected to publish a personal dot plot. At the presser, traders will eye whether he attempts to push a dovish agenda and how he contrasts to his fellow board members. From a yield point, Warsh will be eyed for any hints to his thinking on the Fed balance sheet; should markets be guided to faster unwinding of the Fed’s balance sheet, a steeper curve could be expected.

- Bunds (+20 ticks) trade firmer this morning, continuing recent price action. Domestically, the release of the ECB Wage Tracker had little impact on German paper, where the 2026 quarterly figure rose slightly from the prior. Focus ahead turns to the EZ Final Inflation metrics for May, which are expected to remain unrevised. From a yield perspective, the German 10yr has now slipped below the 3.00% mark (current 2.93%), and now approaching levels not seen since early April.

- Gilts (+57 ticks) outperform vs peers following the region’s inflation report. In brief, a cooler-than-expected print on both a headline and core basis. A series that reduces the odds of a hawkish surprise at the June BoE. However, the as-expected/slightly-hotter (depending on the consensus provider) services figure will be a point of concern for policymakers and may well be enough to keep some dissenters in play, even given the significant energy benchmark moderation in recent days. The report will not have any impact on the policy decision at Thursday's meeting (BoE to hold), but could push the vote split a bit more dovish vs consensus; analysts saw a range between 8-1 to 6-3 before the inflation print and recent energy moderation on US-Iran progress.

- Germany sells EUR 2.107bln vs exp. EUR 2.5bln 3.40% 2047 and 1.80% 2053 Bund.

- Australia sells AUD 300mln 4.75% June 2054 bonds b/c 2.46, avg yield 5.3040%.

COMMODITIES

- Crude futures are essentially incrementally firmer, hovering at 3-month lows, as markets await the US-Iran MoU signing in Switzerland. Details of the deal remain light; however, Reuters did shine some light on a point of the draft MoU: the rehabilitation and economic development of Iran. The report stated that a USD 300bln private fund is being designed to trigger investment into Iran. The report added that commitments have already exceeded USD 150bln across 5 regions, while the fund will not contain US government money or grants.

- Energy benchmarks are relatively contained. WTI Aug'26 oscillates in a USD 74.09-76.06 range while Brent Aug'26 rotates in a 77.75-79.57/bbl band.

- Spot gold has come off slightly ahead of the FOMC meeting, in which a hold is expected. Focus will lie in the press conference, in which Fed Chair Warsh is delivering his first post-policy conference in his new role. The yellow metal currently trades at the lower end of its narrow USD 4318-4350/oz range.

- 3M LME Copper flips either side of the USD 13.8k/t handle as market risk is subdued.

- US Private Inventory Data (bbls): Crude -8.3mln (exp. -4.5mln), Distillates -0.5mln (exp. -0.2mln), Gasoline +2.5mln (exp. -1.4mln), Cushing -1.5mln.

- IEA OMR (Jun): World oil demand falling by 1.1mln BPD in 2026 on the Iran War (prev. forecast 420k BPD fall); sees total world oil supply 920k BPD lower than demand in 2026 (prev. forecast 1.7mln BPD lower).

- TotalEnergies (TTE FP) says its Saudi Arabian refinery was hit by three drones but is still only running at 70% and "probably" will not be repaired until early 2027.

- Tanker Trackers reported that two Iranian supertankers carrying a total of 3.8mln barrels of crude oil passed through the US blockade.

- Two US Senate Democrats are calling for US Energy Secretary Wright to abandon efforts to build a West Coast SPR, CNN reported. Democrats warned that establishing it this fiscal year would flout the law and usurp congressional authority.

TRADE/TARIFFS

- The US delayed the blacklisting of China's DeepSeek and over 100 Chinese firms deemed national security risks, to avoid escalating tensions with Beijing, according to sources cited by Reuters.

NOTABLE EUROPEAN DATA RECAP

- UK Inflation Rate YoY (May) Y/Y 2.8% vs. Exp. 3% (Prev. 2.8%); Services 3.7% (exp. 3.7%, prev. 3.2%).

- UK Inflation Rate MoM (May) M/M 0.2% (Prev. 0.7%).

- UK Core Inflation Rate YoY (May) Y/Y 2.6% vs. Exp. 2.7% (Prev. 2.5%, Low. 2.6%, High. 3.0%).

- UK Core Inflation Rate MoM (May) M/M 0.3% (Prev. 0.7%).

- EU Inflation Rate YoY Final (May) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3%, Low. 3.2%, High. 3.2%).

- EU Inflation Rate MoM Final (May) M/M 0.1% vs. Exp. 0.1% (Prev. 1%, Low. 0.1%, High. 0.1%).

- EU Core Inflation Rate YoY Final (May) Y/Y 2.6% vs. Exp. 2.5% (Prev. 2.2%).

- ECB Wage Tracker: 2026 Quarterly +2.604% (prev. +2.597% Y/Y); Annual +2.281% (prev. +3.193%).

CENTRAL BANKS

- The Riksbank left rates unchanged at 1.75%, as expected, stating probability of a hike in 2026 has increased relative to the March assessment. The Bank stated that the range of potential outcomes for what can happen going forward is wide and the Riksbank is highly prepared to adjust monetary policy.

NOTABLE US HEADLINES

- US admin officials weighed how to structure government stakes in major AI companies, according to Semafor. Treasury Secretary Bessent favoured using equity in AI firms to seed Trump Accounts.

- US President Trump's administration considered requiring Anthropic to obtain government approval before allowing foreign nationals access to its most advanced AI models, as officials weigh new export control measures for AI tech.

- The US Trump administration's federal spending reviews reportedly slowed the government's attempts to reduce the spread of the New World screwworm, Politico reported citing sources.

GEOPOLITICS

MIDDLE EAST

- An informed source told Tasnim that Bloomberg's alleged text about the US-Iran MoU is not accurate, adding that the text of the memorandum, based on the agreement of the parties, will not be published after it is signed on Friday. However, this was later corrected, stating that the text will be released after the signing on Friday.

- US Defence Secretary Hegseth and CIA Director Ratcliffe were among the “most pessimistic” about whether the Iranians would honour their commitments to make substantive concessions on their nuclear program, according to CNN.

- A US senior official was said to have dismissed as "preposterous", the reports of side deals in which Gulf states such as the UAE and Qatar could unfreeze Iranian funds they hold, according to Axios.

- The US Senate voted 48-47 to narrowly block a new bid to rein in Trump's war powers.

- Trump administration officials were reported to be discussing ideas to kick-start oil tanker traffic through the Strait of Hormuz, including offering a fee-based “VIP pass” naval escort through the waterway, according to people familiar with the discussions cited by POLITICO.

- US officials told a CNN reporter that Iran's Supreme Leader has given his tacit approval of the MOU, and that there are internal discussions over whether he could issue a statement ahead of Friday's formal signing ceremony in Switzerland. It was separately reported that US officials downplayed the Iran agreement texts and said that the text omits key back-channel commitments, according to CNN.

- Israeli artillery shelling reported in southern Lebanon, according to SNN.

- Al Jazeera correspondent reported that 10 rockets were fired towards Israeli forces in the vicinity of Kfar Tebnit town in the Nabatieh district of southern Lebanon.

OTHER

- Advisor to US President Trump Massad Boulos is looking to broker a power-sharing agreement between rival administrations in east and west Libya, the FT reported.

CRYPTO

- Bitcoin slips back below the USD 65k handle as the market finds resistance at the 20-SMA.

APAC TRADE

- APAC stocks ultimately traded mixed, albeit at an improvement from the initial losses seen following the subdued lead from Wall St, where most major indices finished in the red amid renewed tech selling.

- ASX 200 shrugged off early weakness and edged mild gains with upside led by mining, materials and tech, although further upside in the index is capped by losses in energy and the defensive sectors.

- Nikkei 225 clawed back initial losses and printed a fresh all-time high after briefly topping the 70,000 level.

- Hang Seng and Shanghai Comp lagged amid losses in auto names and aluminium producers, while they also failed to benefit from a report that the US delayed blacklisting China's DeepSeek and over 100 Chinese firms deemed national security risks. There was also little reaction seen to the PBoC's announcement to add overnight reverse repo instruments and to increase overnight reverse repo operations, as it seeks to improve the efficiency of interest rate transmission.

NOTABLE ASIA-PAC HEADLINES

- PBoC Governor Pan said they will allow overseas institutions to access yuan liquidity and will add overnight reverse repo instruments at the appropriate time, while he added they will increase overnight reverse repo operations and improve the efficiency of interest rate transmission. Pan also stated that six banks are authorised to conduct offshore foreign exchange transactions in the Shanghai Free Trade Zone, and commented that it is difficult and unnecessary for China's credit growth to maintain its previous pace.

- PBoC announces an adjustment to the temporary overnight reverse repurchase and outright repurchase agreement time which is to be set between 15:00-15:30 local time (08:00-08:30BST/03:00-03:30EDT). PBoC seeks to ensure flexible and efficient use of temporary overnight reverse and outright repurchase agreements in the open market. Furthermore, PBoC said operating rates will be set at the 7-day reverse repurchase rate in the open market minus 25bps and plus 25bps, respectively, and that it will act when the money market overnight rate remains consistently below or above the respective operation rates of the tools.

- Chinese Vice Premier He Lifeng said they will step up financial supervision and will vigorously and orderly advance resolution of local government debt, while He added they will issue CNY 300bln special bonds to replenish the capital of financial institutions and that the financial sector will be opened up further.

- China's financial regulator said they will increase regulatory cooperation in emerging areas and will strengthen efforts to avert systemic financial risks. The regulator will also strictly curb unlawful financial activities and address risks in small and medium-sized financial institutions effectively and orderly, while China is to steer financial resources towards emerging and future industries.

- Senior leaders of Japan's ruling party said to have proposed cutting the consumption tax on food to 1% from April 2027 for a two-year period.

NOTABLE APAC DATA RECAP

- Japanese Balance of Trade (May) -378.7B vs. Exp. -564.6B (Prev. 301.9B).

- Japanese Exports YY (May) 17.0% vs. Exp. 16.2% (Prev. 14.8%).

- Japanese Imports YY (May) 12.5% vs. Exp. 12.8% (Prev. 9.7%).