Published: 24 Jun 2026, 10:10 UTC

Newsquawk Desk

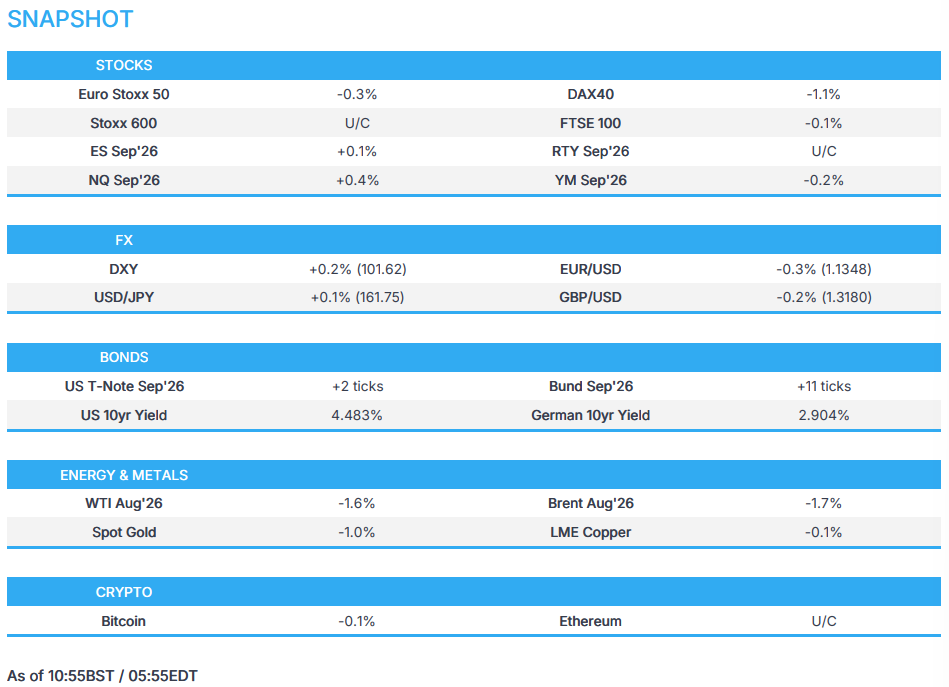

US Market Open: US equity futures steady into Micron earnings; USD and Fixed Income benefit from haven demand

0:00--:--

- Pakistan's Foreign Ministry said it is conducting communications between the US and Iran to effectively implement the MoU and that technical talks will continue next week, potentially on Monday or Tuesday.

- US equity futures hold steady ahead of Micron earnings after-hours, with focus on guidance.

- DXY continues to gain, reaching new levels not seen since May 2025; Antipodeans underperform, with AUD softer amid cooler-than-expected inflation.

- Fixed income benchmarks firmer as it returns as a haven instrument.

- Crude continues to extend lower; spot gold slips below USD 4100/oz and nears a new YTD low.

- Looking ahead, highlights include BoC Minutes (Jun), Fed Bank Stress Test Report, Speakers including BoE's Breeden & Dhingra, BoC's Rogers, ECB's Cipollone, Supply from the US, Earnings from Micron.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 U/C) start Wednesday's trade broadly lower, with the AEX (+0.3%) outperforming as tech names steady from Tuesday's selloff. Germany's DAX 40 (-0.9%) is the clear underperformer, as Rheinmetall weighs on the index. The FT reported that Germany will scrap plans to build Rheinmetall's F126 frigates and instead purchase 8 Meko A-200 frigates from TKMS. Rheinmetall (-14%) has taken a hit following this news, while TKMS (+9.4%) benefits.

- European sectors print a mixed picture. Real Estate (+2.2%) is the clear outperformer, with Food, Beverages & Tobacco (+1.1%) and Consumer Products (+1.2%) rounding out the top 3. Media (-1.3%), Construction (-0.7%) and Energy (-0.6%) are the sector laggards.

- US equity futures are mixed but holding steady following Tuesday's selloff. FedEx (-6.6%) slips pre-market after weaker-than-expected profit guidance overshadowed strong Q4 results. Looking ahead, Micron (+4.3% pre-market) earnings after-hours, with EPS expected at USD 20.57, with revenue expected at USD 35.56bln. With Micron consistently beating revenue estimates, focus will be on its guidance.

- Alphabet (GOOGL) is to replace Verizon (VZ) in the DJIA, effective before the open of trading on June 29th.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are weaker against the Buck as the risk-off mood continues into Micron earnings this evening. Antipodeans lag, as the Aussie digests mixed CPI, JPY fluctuates either side of unchanged, and EMs are getting hit.

- Markets are reluctant to buy the dip in equities after losses on Tuesday. As such, the Buck continues to firm as the preferred haven, with USD outperformance vs Scandis and Antipodeans with liquidity lower. Traditional havens fare better against the Buck, JPY steady at the lower end of its recent ranges, while CHF continues its downward trend. For US-specifics, the highlight of the session will be the Fed Bank Stress Test Report alongside Micron earnings - both due after the close. DXY trades at the upper end of its 101.35-101.68 range, higher by 0.2%.

- Aussie data was mixed, CPI in May cooled below expectations, and the trimmed mean firming in line with most forecasts to 0.4% M/M and 3.6% Y/Y. The report noted housing was the main inflation pressure point, and Westpac analysis notes price pressures are broadening, particularly within services. As such, with the recent energy related prices pressures set to linger, the RBA will be keenly monitoring signs of sticky inflation with the bank widely expected to have concluded tightening. AUD faring better than Kiwi (AUD/NZD +0.1%), but lower against the Buck as the mixed data does not provide a bias towards any future easing/tightening; Labour market data ahead.

- EUR and GBP are lacklustre and tracking the firmer Buck. Domestic catalysts light for both regions, though some continued incrementally optimistic updates from a likely incoming Burnham premiership which has helped GBP. EUR/GBP trades a whisker away from the 200 week moving average @ 0.8602 which is also the session low. For the EUR, recent Governing Council commentary remains hawkish, though nothing deviating too much from the Statement at June’s meeting.

- Barclays sees a moderate dollar-buying by month-end against most majors, with a weak sign on USDJPY.

FIXED INCOME

- Global fixed income benchmarks are slightly firmer, as energy prices continue to pull back and investors seemingly return to see bonds as a haven following the recent tech sell-off.

- USTs (+2 ticks) return to gains after pulling back from a 109-17+ top in Tuesday's session, currently trading at the top end of a 109-09+ to 109-15 range. The US data docket is light today, ahead of Thursday's busy day (PCE, GDP, initial jobless claims, durable goods). On the supply front, the US is to sell USD 70bln 5-year notes. The auction benefits from a combination of higher outright yields, reduced geopolitical uncertainty and a more hawkish Federal Reserve. The key question will be whether the improved backdrop can bring direct bidders back into the sector while maintaining the strong indirect demand seen at the previous auction.

- Bunds (+11 ticks) have been seen as attractive in recent sessions. Analysts see value in long-end German debt, with UBS stating that yields should be capped given any further hike by the ECB is expected to be quickly reversed as it would worsen the trade-off to growth, while rates strategists at Commerzbank say Bunds remain better supported as tech stocks struggle and worries of an AI-bubble. The German IFO data was mixed, with current conditions beating estimates while expectations came in soft; however, no move resulted. German 10yr yield has now returned to 2.90%, with Bunds currently trading at the top end of its 126.67-126.98 range.

- Gilts (+18 ticks) outperform, supported by the lower energy prices and the removal of some political risk premium after Starmer's chief secretary (and former chancellor) Jones said he will not contest against Burnham for the top job. Jones also thinks the bond market can be content with Burnham as PM. Analysts at ING see limited upward risk in terms of rates, but state that political uncertainties are likely to keep upward pressure on gilts, especially the longer end. UK 10yr gilts currently in a 89.33-89.64 range.

- Germany sells EUR 1.785bln vs exp. EUR 2bln 4.00% 2037 and 3.40% 2047 Bund.

- The UK sells GBP 4.25bln 4.125% 2031 Treasury Gilt: b/c 3.47x (prev. 3.36x), average yield 4.284% (prev. 4.651%), tail 0.1bps (prev. 0.2bps).

- Italy sells EUR 2.5bln vs exp. EUR 2-2.5bln 2.20% 2028 BTP and EUR 1.75bln vs exp. EUR 1.5-1.75bln 2.40% 2039 BTPei Auctions.

COMMODITIES

- In geopolitics, the US and Iran are continuing to finalise an agreement within the 60-day negotiation period. Amidst the talks, US President Trump reiterated that they are making a deal with Iran and will see how it goes. Currently, there are conflicting remarks made by US and Iranian officials. There appears to be disagreements surrounding the inspection of Iranian nuclear sites, and on potential tolling of the Strait of Hormuz.

- WTI and Brent are continuing to decline, posting losses of c. 2%. This comes amidst the continued flow of ships traversing through the Strait of Hormuz, albeit still remaining far below pre-war levels. From an oil perspective, estimates suggest that around 6-7mln bpd of oil went through the Strait in the past few days (vs 20mln bpd pre-war). Elsewhere, focus has also been on comments via the Russian Deputy PM Novak, who stated that the country is mulling a diesel export ban, to help ease domestic shortages. Brent Aug’26 currently trades at the bottom end of a 75.53-77.00/bbl range.

- Dutch TTF remains fairly steady, despite the Hormuz flows as focus remains on the heatwave across most of Europe. Attention has also been on French nuclear reactors, which typically need to be shut if the plant cannot cool itself efficiently. Already some EDF reactors have had to shut or taper output, but on the whole France’s national power grid operator said France has enough capacity to meet recent demand.

- Spot gold continues to extend on Tuesday’s losses, and has made a WTD trough at 4,050.47/oz (vs USD 4,115/oz peak). Action which is a continuation of recent losses, stemming from the hawkish repricing at the Fed, stronger USD/higher yields and as sell-side banks continue to trim their PT for the yellow-metal. 3M LME copper trades at the lower end of a USD 13,358-13,483.1/t range.

- US Private Inventory Data (bbls): Crude -0.8mln (exp. -5.0mln), Distillates +1.4mln (exp. -0.4mln), Gasoline +1.2mln (exp. -0.4mln), Cushing -1.0mln.

- US President Trump commented that the big oil companies are not dropping their prices at the pump commensurate with the lower prices they are paying for oil and customers are being 'gouged', while he has instructed the DoJ to look into this and stated that gasoline prices better start going down a lot faster than he is seeing.

- Qatar's PM and Foreign Minister said that the country will resume normal LNG output within weeks, according to the FT.

- Jera Chairman said that restoring Qatar’s LNG facilities, which were damaged during the Iran war, may likely take more than two or three years.

TRADE/TARIFFS

- Brazil will maintain its scheduled tariff hikes on imported electric and hybrid vehicles, with a 35% import tax on assembled and semi-assembled EVs taking effect in July, while disassembled vehicles will face the same rate from January 1st, 2027. Brazil will also introduce additional zero-duty import quotas for disassembled and semi-assembled EVs starting July 1st, providing limited relief for automakers amid higher import barriers.

NOTABLE EUROPEAN HEADLINES

- UK MP Jones said that while he has the 81 seats required to run, he will not contest against Burnham for Labour leadership, Sky News reported. Jones further said he thinks traders "can be content" with Burnham as PM and added that he thinks there is room to "borrow a little more", and things (referring to investment) can be done differently, without "broad brush" borrowing and spending.

- Germany confirmed earlier reports that it will abandon plans to build 6 Rheinmetall (RHM GY) F126 frigates, and instead intends to buy 8 smaller Meko A-200 frigates from TKMS (TKMS GY).

NOTABLE EUROPEAN DATA RECAP

- German Ifo Business Climate (Jun) 85.6 vs. Exp. 85.6 (Prev. 84.9, Low. 85.1, High. 87.0).

- German Ifo Expectations (Jun) 84.1 vs. Exp. 85 (Prev. 83.8).

- German Ifo Current Conditions (Jun) 87.0 vs. Exp. 86 (Prev. 86.1).

CENTRAL BANKS

- BoJ's Ueda said the timing and pace of future hikes will be decided by scrutinising the likelihood of baseline forecasts materialising, as well as risks. He added that there is risks that underlying inflation may overshoot 2%, but that Japan's economy is recovering moderately albeit with some weakness. Financial environment remains accommodative after recent rate hike; continues to support economic activity.

- BoJ Summary of Opinions from the June meeting noted a member said it has become more appropriate to adjust the degree of monetary support as FX moves are pushing up import prices, and a member said it is appropriate to continue raising interest rates as financial conditions are accommodative. There was also the opinion that even after a June rate hike, the BoJ must maintain its stance of proceeding with further rate hikes if the economy and prices move in line with forecasts. The Summary of Opinions also stated they must push up the BoJ's policy rate closer to the neutral rate as soon as possible and to near neutral at an early date to avoid big and sharp rate hikes in the future. Furthermore, a member said Japan's neutral rate is seen at around 2%, and the BoJ must raise its rates once every few months, while a member said there was no reason for the BoJ to halt a reduction in its JGB purchases.

- RBA’s Hauser said that there have been important economic developments since May and not least the chance of a US-Iran deal. Hauser said the RBA took proactive policy action to reduce excessive capacity pressures through rate hikes, while timely policy steps to reduce inflation could have lower unemployment costs. The RBA still has work to do to reduce inflation, which remains far too high.

- Riksbank Minutes (Jun): Governor Thedeen said it is reasonable to indicate that it is now somewhat more likely that we will raise the policy rate in the future. I think that this forecast is still reasonable, given the signals now coming with regard to a solution to the war between Iran and the United States.

NOTABLE US HEADLINES

- The US Senate voted 50-48 to pass a resolution to halt the Iran war unless US President Trump gets approval from Congress. However, the White House said Congress resolutions on Iran are non-binding and won't be sent to President Trump, while Trump criticised the Senate passage of the Iran war powers resolution, which he claimed provides aid and comfort for the enemy.

- US President Trump plans to sign the housing bill in the Capitol on Wednesday, while the US House voted 358-32 in favour of the bipartisan bill to spur construction of affordable housing amid severe shortages.

- US Treasury Secretary Bessent said inflation will return to the target, and he is confident Fed Chair Warsh will optimise the path for the economy. Bessent also stated that the US housing issue is a conundrum affected by rate-lock owners, and will take lower rates and more supply.

GEOPOLITICS

MIDDLE EAST

- Pakistan's Foreign Ministry said it is conducting communications between US and Iran to effectively implement the MoU and that technical talks will continue next week; potentially Monday or Tuesday.

- Israel and Lebanon are in talks on a US-supported pilot project involving the withdrawal of Israeli troops from some parts of southern Lebanon and hand it over to Lebanese forces, according to several Israeli officials.

- Iranian Parliament Speaker Ghalibaf said Iran extends its hand of brotherhood and cooperation to all countries in the region and is ready to establish security agreements with all countries in the Middle East.

- Iranian senior commander said Iran's military has shifted to an aggressive doctrine.

- Oman established a temporary shipping lane in the Strait of Hormuz, according to IRNA. Furthermore, the Maritime Security Center in Muscat said Oman coordinates with the IMO for ships to pass through the Strait of Hormuz "without fees", according to Al Jazeera.

- Israeli Military reportedly preparing for redeployment in southern Lebanon, Al Hadath reported citing Maariv.

- Israeli tanks advanced towards Beit Yahoun in Lebanon, with heavy gunfire reported near Beit Yahoun and Kounin, while it was also reported that Israeli strikes hit the Lebanese coastal city of Tyre. Furthermore, Israeli fighter jets reportedly attacked a school in the At-Tuffah neighbourhood in eastern Gaza, and Israeli military entered Syria's Quneitra province.

RUSSIA-UKRAINE

- Russia is reportedly considering a new wave of mobilisation as early as October 2026.

- Russia gas plant in Orenburg was targeted overnight by drones, Kyiv Post reported.

OTHER

- North Korea leader Kim Jong-un said North Korea will build two Choe Hyon-class warships annually over the next five years, as it advances the nuclearisation and strategic expansion of its navy, while Kim said they will equip their destroyers with nuclear weapons.

CRYPTO

- Bitcoin consolidates in a narrow USD 62.37k-63.04k/t range after falling in Tuesday's session amid the risk-off tone.

APAC TRADE

- APAC stocks saw mixed price action as the initial rebound from the prior day's tech-driven sell-off gradually waned in the absence of any fresh major catalysts.

- ASX 200 traded rangebound as strength in tech and defensives was counterbalanced by losses in mining and energy following the recent declines in underlying commodity prices, while inflation data was mixed and would likely have little bearing on monetary policy.

- Nikkei 225 failed to sustain early gains and dipped back beneath the 70,000 level, while Services PPI data printed in line with forecasts and the BoJ Summary of Opinions showed members continued to advocate for further rate increases.

- Hang Seng and Shanghai Comp were indecisive as the attention turned to the WEF in Dalian, where Premier Li said China's economy shows resilience and maintains sound momentum. He stated China remains committed to opening up and will continue to accelerate the large-scale application of new technologies.

NOTABLE ASIA-PAC HEADLINES

- Japan is reportedly looking at ways to streamline the management of its USD 1.3tln FX reserves to increase returns and help state finances, Reuters reported.

- A draft proposal of 1% consumption tax was presented and will reportedly be implemented from April 2027, FNN reported. The proposal faces significant resistance from opposition parties, with DPP representative Furukawa stating they have no intention of cooperating, leaving the prospect of a June agreement uncertain.

- Chinese Premier Li said China's economy shows resilience and maintains sound momentum, while he noted four key words for the economy including stability, innovation, dynamism and integration. Li also stated that China remains committed to opening up, as well as noted that China's AI sector sees explosive growth, and they will continue to accelerate the large-scale application of new technologies.

NOTABLE APAC DATA RECAP

- Australian Inflation Rate YoY (May) Y/Y 4.0% vs. Exp. 4.3% (Prev. 4.2%, Low. 3.8%%, High. 4.9%).

- Australian Inflation Rate MoM (May) M/M -0.7% vs. Exp. -0.4% (Prev. 0.4%).

- Australian RBA Trimmed Mean CPI YoY (May) Y/Y 3.6% vs. Exp. 3.5% (Prev. 3.4%).

- Australian RBA Trimmed Mean CPI MoM (May) M/M 0.4% vs. Exp. 0.3% (Prev. 0.3%).

- Japanese Services PPI YY (May) 3.3% vs Exp. 3.3% (Prev. 3.0, Rev. 3.3%).