Published: 26 Jun 2026, 05:56 UTC

Newsquawk Desk

EU Market Open: Crude benchmarks continue to slip despite halts to the Hormuz evacuation plan; European equities are set to open lower

0:00--:--

- Iran attacked a Singapore-flagged cargo ship on Thursday in the Strait of Hormuz, WSJ reported, citing sources. Separately, the UN shipping agency temporarily paused its evacuation plan for stranded ships and seafarers out of Hormuz after the attack.

- Iran's PGSA said vessels outside PGSA-set routes will not be guaranteed safe passage.

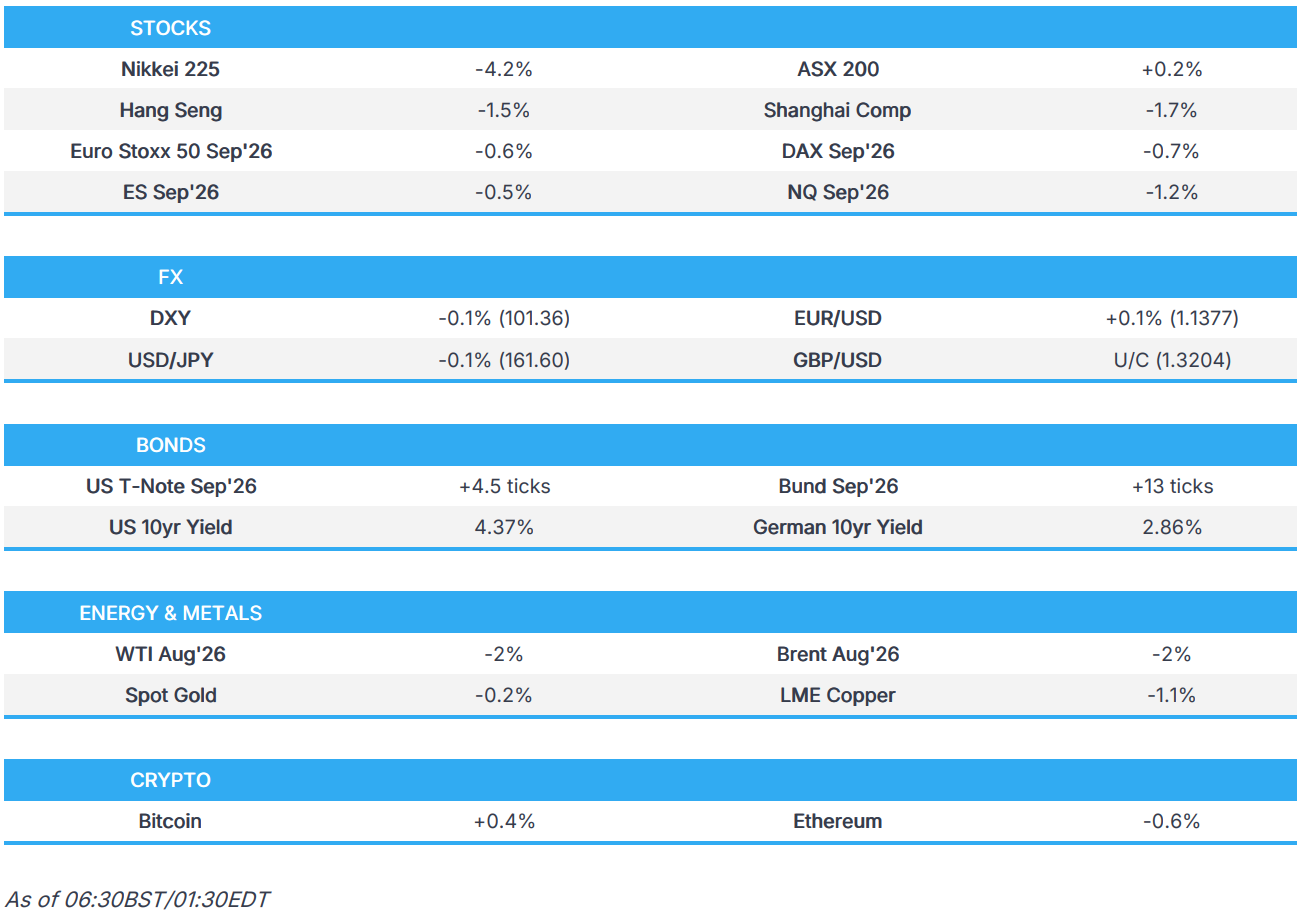

- APAC stocks were broadly on the backfoot, with hefty declines in the tech-heavy KOSPI; European equity futures are indicative of a weak open.

- DXY trades with incremental losses; USD/JPY continues to hold around the 160.60 level.

- Looking ahead, highlights include Swedish PPI (May), US Goods Trade Balance Advance (May), Wholesale Inventories (May), UoM Sentiment Final (Jun), ECB CES (May), Speakers including Kashkari, ECB's Nagel & Vujcic, RBNZ's Bremen, Norges Bank's Bache, and Supply from Italy.

IRAN CONFLICT

- US President Trump said they have a new market coming up called Iran, and that Iran wants to make a deal with them very badly, while he thinks that they will make a deal and stated the Strait is open.

- Iran attacked a Singapore-flagged cargo ship on Thursday in the Strait of Hormuz, according to the WSJ citing US officials. It was separately reported that the UN shipping agency temporarily paused its evacuation plan for stranded ships and seafarers out of Hormuz after the attack. The vessel did not transit under the UN agency's evacuation framework, while the evacuation plan will remain paused until further clarity is obtained.

- Iran's PGSA said vessels outside PGSA-set routes will not be guaranteed safe passage and that consequences arising from passage through unauthorised routes shall be the responsibility of the owner, operator, and vessel commander, while vessels using unauthorised routes will not be covered by insurance on related liabilities.

- IAEA chief Grossi said it's undeniable they have an agreement that the IAEA will have access to Iran for inspection, while he added that they hope to resume their work in Iran soon.

- Saudi Arabia's Foreign Minister held two separate meetings with Qatari and Omani counterparts to discuss the results of the undertaking between the US and Iran regarding regional security and stability, according to IRNA.

- Israeli Embassy in Washington said due to extension in the discussions, negotiations between Israel and Lebanon mediated by the US will continue on Friday for a fourth day, according to a Kan reporter.

- Israeli Energy Minister said the withdrawal from southern Lebanon is not under consideration and would be rejected even if requested by US President Trump, while he stated that Israel does not plan to occupy all of Lebanon, but intends to establish full security control over the entire Gaza Strip.

- US Secretary of State Rubio's pressure on Israel and Lebanon was said to have led to an agreement on a "declaration of intent", according to Al Hadath.

- Israel and Lebanon are discussing a partial withdrawal of the IDF from southern Lebanon, despite the public statements, according to Kann News citing sources, while there are difficulties and the atmosphere is tense, but progress has been made.

- UN said the Lebanon ceasefire is largely holding, though Israeli military operations inside Lebanon continue. It was separately reported that Israel's military conducted airstrikes on Beit Yahun, Lebanon, while Israeli tank movements were reported in Wadi Saluqi and Bint Jbeil, Lebanon.

US TRADE

EQUITIES

- US stocks finished a volatile session mixed as optimism surrounding memory names improved following a strong Micron earnings report, while amplified concerns over hyperscalers' spending limited further upside, and weighed on such names. Despite the incoming Apple price hikes being expected following CEO Cook's recent touting, the announced price increases for MacBook and iPad saw the stock down 6.1%. Mag-7 underperformed the market as debt and equity issuance continued to act as a headwind on the space; meanwhile, the equal-weighted S&P 500 RSP outperformed the market-cap weighted counterpart, rising 0.6%. Participants also digested a US data dump which included a mixed PCE report, personal income & spending beat, initial claims fell W/W, continued claims rose W/W, and Q1 GDP growth revised above expectations.

- SPX -0.01% at 7,358, NDX +0.75% at 29,440, DJI +0.14% at 51,926, RUT +0.71% at 3,008.

- Click here for a detailed summary.

TARIFFS/TRADE

- Bangladesh's PM said in a meeting with Chinese President Xi that they need China's support in implementing their major signature projects and upgradation and modernisation of existing industrial units, while the PM also urged for a reduction in the trade gap.

- US Commerce Department banned sales of Geely (175 HK)-owned Chinese luxury EV Polestar, from 2027 onwards.

NOTABLE HEADLINES

- Fed's Williams (voter) pushed back hitting the 2% inflation target from 2027 to 2028 and reiterated that monetary policy is ‘well positioned’ for the current economy, while he expects inflation to moderate to 3.5% this year. Williams said if Middle East war disruptions are resolved soon, it will lower inflation pressure, and he expects inflation pressures to moderate.

- Fed's Goolsbee (2027 voter) said it is difficult to determine whether inflation pressures are persistent or temporary, while noting inflation is moving in the wrong direction, and some of that is being driven by one-off factors. He added that inflation remains more concerning on the services side and that spending based on expected future gains makes him concerned about potential inflationary pressures. Goolsbee also said there are some signs of improvement in services inflation, but it remains well above where it needs to be, as well as stated that core inflation it is still too high and trending in the wrong direction, while services-driven core CPI is more concerning than inflation driven by goods or oil-related items. Furthermore, he stated that wages are not a particularly good leading indicator for inflation and that inflation could rise before wages do, adding that inflation needs to be monitored closely.

- US President Trump signed an agriculture-related executive order to strengthen US food supply security.

- US President Trump's administration asked OpenAI to restrict the launch of its next model, GPT-5.6, to only a small set of government-approved partners before a wider release due to security concerns, according to a source cited by Axios.

- US House Speaker Johnson said he's sending the bipartisan housing bill to the White House, following his meeting with President Trump.

APAC TRADE

EQUITIES

- APAC stocks were pressured following the choppy performance stateside, where markets were indecisive amid two-way trade in tech, a recent data deluge and a rebound in oil. The overnight deterioration in risk sentiment coincided with renewed selling in tech after Apple raised prices of some products by nearly 20% and with OpenAI leaning towards delaying its IPO until next year.

- ASX 200 was rangebound with the index cushioned as the underperformance in tech, telecoms and healthcare was partially offset by resilience in some defensive stocks.

- Nikkei 225 suffered heavy losses as tech stocks dominated the list of worst performers, with SoftBank down by a double-digit percentage owing to its large exposure to AI and semiconductors.

- KOSPI remained volatile with the slump triggering a sidecar and eventual circuit breaker alongside notable declines in both Samsung Electronics and SK Hynix.

- Hang Seng and Shanghai Comp conformed to the sell-off across the region amid the tech rout.

- US equity futures retreated as the sentiment in Asia further deteriorated amid a tech sell-off.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 futures down 1.0% after the cash market finished with gains of 0.9% on Thursday.

FX

- DXY traded rangebound amid the negative mood in Asia and decline in oil prices, with the greenback also contained after yesterday's choppy performance in which it marginally weakened against peers following a data deluge; that included softer-than-expected headline PCE M/M. Nonetheless, the data was ultimately mixed as Q1 GDP was revised higher and above expectations, personal income and spending topped forecasts, initial jobless claims fell W/W, but continued claims rose, and durable goods declined, albeit not as much as expected. There were also recent comments from Fed's Goolsbee, who continued to stress that core inflation is too high, trending the wrong way, and that services inflation is a little more disturbing.

- EUR/USD was indecisive after recent fluctuations and with few fresh catalysts for the single currency.

- GBP/USD lacked firm conviction after recent mild swings, but attempts to reclaim the 1.3200 status, while pertinent newsflow for the UK remained quiet.

- USD/JPY remained confined to within relatively tight parameters after pulling back from resistance just shy of the 162.00 level, and as the latest Tokyo CPI data mostly matched estimates.

- Antipodeans mildly underperformed amid the risk-off mood and declines in commodity prices.

- PBoC set USD/CNY mid-point at 6.8166 vs exp. 6.8015 (prev. 6.8209).

- Mexican Interest Rate Decision 6.50% vs. Exp. 6.50% (Prev. 6.50%); vote was unanimous. The Governing Board estimates that it will be appropriate to maintain the reference rate at its current level,. It judged that the monetary policy stance is well-suited to face the challenges posed by the macroeconomic environment, including those associated with the international context.

FIXED INCOME

- 10yr UST futures eked mild gains overnight above the 110.00 level after climbing in the aftermath of the US data deluge, with the cooler-than-expected PCE M/M for May the highlight.

- Bund futures edged higher after the prior day's indecision and amid a flight to quality.

- 10yr JGB futures clawed back opening losses with upside seen as risk sentiment deteriorated.

COMMODITIES

- Crude futures pulled back overnight after rebounding yesterday alongside reports that Iran attacked a Singapore-flagged cargo ship in the Strait of Hormuz, which prompted the UN shipping agency to temporarily pause its evacuation plan for stranded ships. Nonetheless, reports overnight suggested increased transit through the strait with several Japanese-related vessels said to have passed through the waterway as part of the now suspended IMO evacuation plan. Moreover, South Korea's Oceans Ministry announced eight more South Korean vessels had exited the Strait of Hormuz, and Saudi Aramco also resumed oil loadings at Ras Tanura.

- Saudi Aramco reopened the Ras Tanura oil loading operations after a prolonged halt, with two supertankers loading oil at Ras Tanura on Friday, while another is awaiting loading, according to shipping data.

- Several Japanese-related vessels passed through the Strait of Hormuz as part of IMO evacuation plans, which have since been suspended following the attack on a cargo ship, according to Mainichi.

- South Korea's Oceans Ministry said eight more South Korean vessels exited the Strait of Hormuz, while South Korean President Lee said three more ships are to leave the Strait of Hormuz over the weekend.

- Spot gold traded indecisively on both sides of the USD 4,000/oz level with the precious metal on course for its fourth consecutive weekly loss.

- Copper futures retreated amid the negative risk appetite as tech selling resumed in Asia.

CRYPTO

- Bitcoin was choppy and rebounded from an early dip with prices reapproaching the USD 60,000 level.

- Binance is to stop providing services to EU clients after failing to obtain a licence, according to FT.

NOTABLE ASIA-PAC HEADLINES

- Samsung Group is said to invest around USD 647bln for 10 years in South Korea, while Samsung Electronics (005930 KS) may invest KRW 300bln in new semiconductor fabs in South Korea.

DATA RECAP

- Japanese Tokyo CPI YY (Jun) 1.7% vs. Exp. 1.7% (Prev. 1.4%)

- Japanese Tokyo CPI Ex. Fresh Food YY (Jun) 1.6% vs. Exp. 1.6% (Prev. 1.3%)

- Japanese Tokyo CPI Ex Food and Energy YY (Jun) 1.9% vs. Exp. 1.8% (Prev. 1.6%)

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian President Zelensky approved a 40-day campaign to "influence" Russia to end the war.

- Power cuts were reported in Russian-held Kherson region, whilst Sevastopol restricted power following drone attacks.

- EU leaders agreed to extend Russian sanctions for 12 months.

OTHER

- North Korean leader Kim oversaw the testing of key weapons, according to KCNA.

- South Korea plans a rapid expansion of drone and anti-drone forces, while it plans to train 500k drone operators.