Published: 30 Jun 2026, 10:18 UTC

Newsquawk Desk

US Market Open: NQ set to end Q2 with gains of 24%; Markets await US-Iran talks in Doha

0:00--:--

- US President Trump's envoys Kushner and Witkoff are flying to Doha for talks; Iran believes the trip is focused on ceasefire compliance, and is not there for talks with the US, NYT reported.

- US equity futures are slightly firmer (NQ +0.1%) and set for their biggest quarterly gain in 6 years.

- DXY strengthens, lifting USD/JPY firmly above 162.00; EUR weakness helped by cooler French and German State CPIs.

- Fixed income benchmarks higher but off best levels, with a busy central bank speaker slate ahead.

- Crude benchmarks dip again despite uncertainty over US-Iran talks in Doha.

- Looking ahead, highlights include German Inflation Prelim. (Jun), Canadian GDP (Apr), US JOLTs (May), Speakers include ECB's Schnabel, Cipollone, Rehn & Lane, BoE's Breeden, Earnings from Nike.

EUROPEAN TRADE

EQUITIES

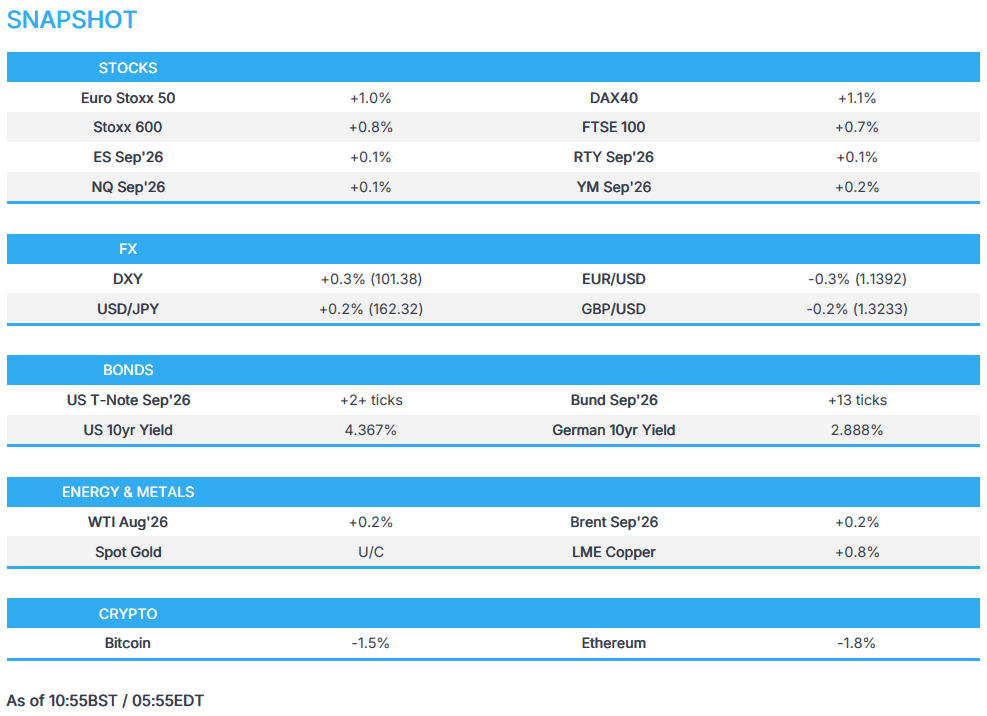

- European bourses (STOXX 600 +0.8%) begin the last day of Q2 entirely in the green, with outperformance in the DAX 40 (+1.1%) and AEX (+0.7%). Many indices are set to have their biggest quarterly gain since the end of 2022, with the STOXX 600 just shy of 10% gains for Q2. Focusing on Germany's DAX, analysts see possible continued underperformance, with any flare-up in EU-China tensions posing a further headwind. Its auto sector has been particularly affected in recent months, with China playing a key role in that narrative.- European sectors highlight the positive bias. Basic Resources (+2.1%), Technology (+1.3%) and Industrial Goods & Services (+1.6%) are the outperformers, while Consumer Products & Services (-0.9%), Food, Beverages & Tobacco (-0.4%) and Telecoms (-0.3%) are the only sectors printing modest losses.

- US equity futures are also firmer across the board, with the NQ's Q2 gains in excess of 24%. The tech/AI story has been the key part of the move higher in recent months and is set to remain a key fundamental driver in the coming months.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Snapshot: G10s are lower against the USD to varying degrees. The CHF, EUR and JPY are all the laggards this morning, to the tune of c. 0.3%, whilst the Antipodeans are faring a little better vs peers.

- DXY is firmer this morning and trades at the upper end of a 101.12 to 101.42 range. No real driver this morning for the index, but comes amidst a tense geopolitical risk-tone and ahead of key US data. The slight strength today can also be explained as a bit of a bounce back, after recent USD strength has faded a touch off recent highs. The high from Monday (101.07) was breached this morning, whereby another bout of strength could see a test of Friday’s high (101.57) and Thursday’s best (101.74).

- EUR/USD is amongst the worst performers this morning, as markets digest the sheer amount of ECB speakers at Sintra. Overall, the bias has been hawkish; namely, President Lagarde and Chief Economist Lane have highlighted that the oil price curve remains elevated, and that could suggest higher costs for the economy. Nonetheless, policymakers have broadly reiterated data dependency and avoided any pre-commitment to July/September. On that front, Reuters sources suggested that given recent energy dynamics, September is now seen as more likely than July for another hike; the source clarified that a rate hike is not off the agenda. As it stands, money markets assign a 32% chance of a hike in July and a 70% chance of a move in September.

- On the data front, the EUR has had dovish German State CPI metrics to contend with. Broadly speaking they are indicative of a cooler Y/Y print, despite mainland consensus for the headline remaining at 2.6%.

- JPY is also amongst the laggards. Overnight, the pair jumped above the 162.00 mark, amidst commentary from Chief Cabinet Secretary Kihara. He initially suggested that he would not comment on FX, which saw the pair breach 162.00. However, a few minutes later, he stated that they are always ready to take necessary action on Forex. The move largely unwound on that jawboning attempt. Thereafter, Finance Minister Katayama also commented. She warned that they will respond appropriately to currency moves at any time as needed, while action could include decisive action as agreed in the joint statement with the US. USD/JPY currently holds within a 161.89-162.41 range.

FIXED INCOME

- Global fixed income benchmarks are firmer across the board, helped by softer energy prices, but also supported by cooler inflation prints in the EZ.

- Bund (+13 ticks) upside initially came following the French inflation data, in which HICP softened to 2%, below the expected 2.4% and from the prior 2.8%. This followed the Spanish print on Monday, which came in slightly hotter-than-expected, but saw relief after the core figure cooled. The German state CPIs can give further relief for the ECB, after prices broadly cooled in all states. This comes ahead of the nationwide figure later today; HICP is expected to hold at 2.7%.

- Many ECB policymakers were also on the wires this morning at the sidelines of Sintra. President Lagarde kicked off the Sintra conference on Monday. Even though her comments sounded slightly hawkish, it seemed to be an unwind of her dovish stance when she spoke last week in a way to keep all options on the table. Lane was the first GC member to speak today, in which he highlighted that the oil price curve is seen elevated in the coming years, which suggests higher economic costs.

- USTs (+2+ ticks) follow its German counterpart higher, albeit to a lesser extent, with focus this week being on comments by Fed Chair Warsh at Sintra on Wednesday and the US jobs report on Thursday.

- JGBs (-3 ticks) traded on the softer side in the Asia-Pac seen, however there was some relief following the 2-year JGB auction. The b/c was 4.82x, which was higher than the prior 3.70x and above the 12-month average of 3.74x. The strong auction was also backed by a small price tail. Despite the strong auction, investors remain concerned about further BoJ hikes, and perhaps more aggressively, to stabilise the Yen (USD/JPY recently topped 162.40).

- Japan sells JPY 2.15tln 2-year JGBs b/c 4.82 (prev. 3.70), average yield 1.407% (prev. 1.369%).

COMMODITIES

- Crude benchmarks are firmer, posting gains of around USD 0.10/bbl at highs of USD 70.88/bbl and USD 74.08/bbl for WTI and Brent, respectively.

- In brief, we await any information relating to or stemming from the Doha talks. US envoys Kushner and Witkoff are travelling to Doha. However, Iran has made clear it will not be holding talks with the US “at any level” in the next few days, with the Doha gathering to only discuss ceasefire compliance. Albeit, sources via Pakistani journalist Mallick suggest that talks could occur via Pakistani/Qatari mediators.

- Spot gold firmer, but only marginally so. Overnight, pressure was seen alongside a jump in USD/JPY (see FX/morning JPY update for details), action that was exacerbated by a breach of the USD 4000/oz mark to the downside. Sending XAU to a USD 3942/oz base.

- In the first part of the European morning this unwound, with XAU climbing back above USD 4k/oz and hitting a USD 4037/oz peak in short order. There wasn’t a specific or fresh fundamental driver behind this, though the move did take place alongside a modest uptick in the fixed income space, marginal downside in energy and a moderation of the performance of both European and US equity futures.

- Base metals in focus after the EU increased tariffs on steel. The move will reduce the duty-free import level by an average of 47%. Following the move, an official cited by the FT outlined that the EU hopes to create a “steel club” with the US and others, in order to reduce trade barriers. Broadly, base metals are firmer, reflecting the risk tone and despite the firmer USD.

- US President Trump posted "Gasoline Retailers must get their Prices down, IMMEDIATELY! They’re too high considering that Oil is now at $68 a Barrel, and heading south. The Retailers must quickly react to this statement, and do what they know is right".

- Shell (SHEL LN) expects LNG demand to increase by around 65% by 2050, largely driven by APAC nations.

- China is said to be easing some refinery fuel export restrictions as domestic supply is ample, according to reports.

- Morgan Stanley slashes its Q3 dated Brent forecast by USD 15 to USD 75/bbl as supply returns through Hormuz.

TRADE/TARIFFS

- USTR posted that the US welcomes Switzerland’s progress in implementing elements of a historic Framework Agreement, while it was stated that they will continue to work towards the conclusion of an agreement on fair, balanced, and reciprocal trade that will further remove non-tariff barriers.

- China and the EU agreed to maintain global supply chain stability, continue consultations on trade, and solve some intellectual property issues, while China and the EU exchanged market access lists.

- EU declared new rule to protect EU steel. The EU's steel measure, which enters into application on 1 July 2026, reduces duty-free imports of 26 categories of steel products into the EU by an average of 47% as compared with the quotas under steel safeguard.

- White House announced temporary suspension of duties on fertilizer from Morocco, according to a Fact Sheet.

NOTABLE EUROPEAN HEADLINES

- UK Government announced a GBP 15bln defence package.

NOTABLE EUROPEAN DATA RECAP

- French HICP YoY Prel (Jun) 2.0% vs. exp. 2.4% (Prev. 2.80%).

- French HICP MoM Prel (Jun) -0.3% (Prev. 0.10%).

- French Inflation Rate YoY Prel (Jun) Y/Y 1.8% (Prev. 2.4%).

- French Inflation Rate MoM Prel (Jun) M/M -0.2% vs. Exp. 0% (Prev. 0.1%).

- Italian HICP YoY Prel (Jun) 3.1% vs. Exp. 3.2% (Prev. 3.20%).

- Italian HICP MoM Prel (Jun) 0.1% vs. Exp. 0.2% (Prev. 0.30%).

- Italian Inflation Rate YoY Prel (Jun) Y/Y 3.0% vs Exp. 3.2% (Prev. 3.2%).

- Italian Inflation Rate MoM Prel (Jun) M/M 0.0% vs. Exp. 0.1% (Prev. 0.4%).

- German North Rhine Westphalia CPI YoY (Jun) Y/Y 2.1% (Prev. 2.4%).

- German North Rhine Westphalia CPI MoM (Jun) M/M -0.4% (Prev. -0.2%).

- German Import Prices MoM (May) M/M 0.7% (Prev. 1.2%, Low. -0.5%, High. 0.5%).

- German Import Prices YoY (May) Y/Y 6.8% (Prev. 5.3%).

- German Retail Sales MoM (May) M/M 1.1% (Prev. -0.3%, Low. -0.5%, High. 0.5%).

- German Retail Sales YoY (May) Y/Y 1.8% vs. Exp. 0% (Prev. -0.3%).

- UK GDP Growth Rate QoQ Final (Q1) Q/Q 0.6% vs. Exp. 0.6% (Prev. 0.2%, Low. 0.5%, High. 0.6%).

- UK GDP Growth Rate YoY Final (Q1) Y/Y 0.9% vs. Exp. 1.1% (Prev. 1%, Low. 1.1%, High. 1.1%).

- UK BRC Shop Price Inflation (Jun) 1.2% vs. Exp. 1.3% (Prev. 1.2%).

- UK Lloyds Business Barometer (Jun) 44 vs Exp. 48 (Prev. 47).

CENTRAL BANKS

- ECB's Lane said there has been some improvement in confidence, but not at pre-war levels. He added that the oil price curve sees elevated levels in the years coming, which suggest higher cost for the economy. On the ECB's rate path, he said July vs September is too narrow a debate but aiming to keep options open by not boxing themselves into a specific meeting.

- ECB's Nagel said it is too early make rate hike calls but rate policy has to stay vigilant as inflation may stay significantly above target.

- ECB's Wunsch said we might need another hike and would rather move quickly if the ECB needs another hike. A quick ECB move does not necessarily mean a July move.

- ECB's Sleijpen said while oil prices have come down, there is still a lot of uncertainty and reiterated the ECB's data-dependent approach.

- ECB sources said a rapid oil price retreat eases pressure on the ECB to hike in July and September is seen as more likely, although a June inflation surprise could reignite talk of a July hike, while sources added that a rate hike is not off the agenda even though it may be delayed, according to Reuters.

- BoJ's Sato said the de-escalation of the Middle East conflict is a welcoming move but uncertainty remains on outlook.

- RBA Minutes from the June meeting stated that policy needed to remain restrictive and it will do what is needed to achieve price stability, including raising rates if necessary. The Board saw merit in using the room created by earlier hikes to assess how the economy was faring and noted that leaving rates unchanged would best balance inflation and jobs objectives. Furthermore, it stated that the economy was operating with excess demand and broad-based price pressure, as well as noted that the Middle East conflict still posed material upside risks to inflation and downside risks to activity.

NOTABLE US HEADLINES

- US House Speaker Johnson said no veto is expected for the housing legislation and that the housing bill will become law, while he noted that President Trump has yet to decide on signing the bipartisan housing package, according to POLITICO.

GEOPOLITICS

MIDDLE EAST

- US President Trump's envoys Kushner and Witkoff are flying to Doha for talks, while Iran said the Doha mission is focused on ceasefire compliance and is not there for talks with the US, according to NYT.

- US Secretary of State Rubio said at a Congress briefing that there is a possibility the nuclear talks with Iran may fail, while he also stated that Iran has not yet received any funds under the MoU.

- Iranian President Pezeshkian said "Understanding is a bilateral matter. If the American side adheres to the memorandum of understanding, we will also fulfil our obligations", while he said their approach to unreasonable boasting and unfounded threats is to rely on rationality and human dignity in decision-making and to defend themselves decisively and fearlessly when taking action.

- Iran's Deputy Foreign Minister Gharibabadi said if they do not reach an understanding with Oman on the routes and arrangements of the Strait of Hormuz, they will, in any case, implement Iran's new sovereignty and policy in the Strait of Hormuz, while he added that they do not guarantee the safety and security of ships passing through parallel routes in the Strait of Hormuz.

- Iran's acting Defence Minister al-Reza said we do not trust the enemy and our hands are on the trigger in the event of any ceasefire violations, will take appropriate and necessary action.

- The framework agreement between Israel and Lebanon has reportedly caused a rift in Iran-Lebanon relations, with Iranian FM Araghchi refusing to visit Lebanon, according to Kan's Kais citing a Lebanese newspaper.

- An explosion was reported in southern Lebanon, which was carried out by Israeli forces, while it was also reported that Israeli forces conducted a strike on town of Deir Sryan in southern Lebanon and that Israeli attacks on Gaza left 48 dead and wounded, according to Tasnim and Mehr News Agency.

RUSSIA-UKRAINE

- Russia reported it shot down 419 Ukrainian drones overnight.

OTHER

- Afghanistan's Taliban said it is planning a retaliatory response to the Pakistan army, and it may close the Pakistan embassy in Kabul over attacks, but also commented that it prefers diplomatic talks to resolve Pakistan tensions.

CRYPTO

- Bitcoin failed to hold above USD 60k, as the crypto coin looks set for its third straight quarterly decline.

APAC TRADE

- APAC stocks were mixed with choppy price action seen overnight heading into quarter-end, despite the gains in the US, where the DJIA notched a record close, and the Nasdaq outperformed amid strength in tech and communications.

- ASX 200 traded little changed amid mixed performances of its sectors and after the RBA minutes from the June meeting continued to affirm a hawkish stance. It stated that policy needed to remain restrictive and the RBA will do what is needed to achieve price stability, including raising rates if necessary.

- Nikkei 225 ultimately rallied, but initially swung between gains and losses, with the index fluctuating through the 70k level, amid a weaker currency, FX intervention risks, and disappointing Industrial Production.

- Hang Seng and Shanghai Comp lagged as a rebound in tech stocks was counterbalanced by losses in miners and energy majors, while they also failed to benefit from better-than-expected PMI data and another PBoC overnight repo operation.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama won't comment on specific effects levels, but said they will respond appropriately to currency moves at any time as needed, while she added that action could include decisive action as agreed in the joint statement with the US.

- Japan's Chief Cabinet Secretary Kihara said he won't comment on FX levels, but added that they are always ready to take necessary action on FX.

- Decision on reducing Japan's consumption tax on food products has been postponed until July due to pushback from the opposition parties, according to TBS.

NOTABLE APAC DATA RECAP

- Chinese NBS Composite PMI (Jun) 50.6 (Prev. 50.5).

- Chinese NBS Manufacturing PMI (Jun) 50.3 vs Exp. 50.1 (Prev. 50).

- Chinese NBS Non-Manufacturing PMI (Jun) 50.2 vs. Exp. 49.9 (Prev. 50.1).

- Japanese Industrial Production MoM Prel (May) M/M 0.5% vs. Exp. 1.1% (Prev. 0.5%).

- Japanese Industrial Production YoY Prel (May) Y/Y -1.7% vs Exp. 1.2% (Prev. 2.0%).

- Japanese Unemployment Rate (May) 2.5% vs. Exp. 2.5% (Prev. 2.5%).

- Japanese Jobs/Applications Ratio (May) 1.17 (Prev. 1.18, Low. 1.17, High. 1.19).

- South Korean Industrial Production MoM (May) M/M -3.0% vs. Exp. 0.5% (Prev. -0.7%).

- South Korean Industrial Production YoY (May) Y/Y -0.9% vs. Exp. 3.6% (Prev. 1.5%).