Published: 1 Jul 2026, 05:58 UTC

Newsquawk Desk

EU Market Open: President Trump was reportedly briefed on "all out war options", but opted to stick to talks; DXY awaits Fed Chair Warsh

0:00--:--

- US President Trump was briefed on all-out war options on Iran, but opted to stick with talks, while he told aides he's okay if talks go past the August 18th deadline, WSJ reported. However, VP Vance said Trump is ready to drop bombs again.

- A US official said ships are transiting the Strait of Hormuz at higher levels.

- Iran's Foreign Ministry Spokesperson said the meeting on Wednesday in Doha will primarily focus on the release of blocked funds and the ceasefire in Lebanon. A US admin official, cited by the NYP, suggested the US has not released any frozen funds, and will not until Tehran “performs”.

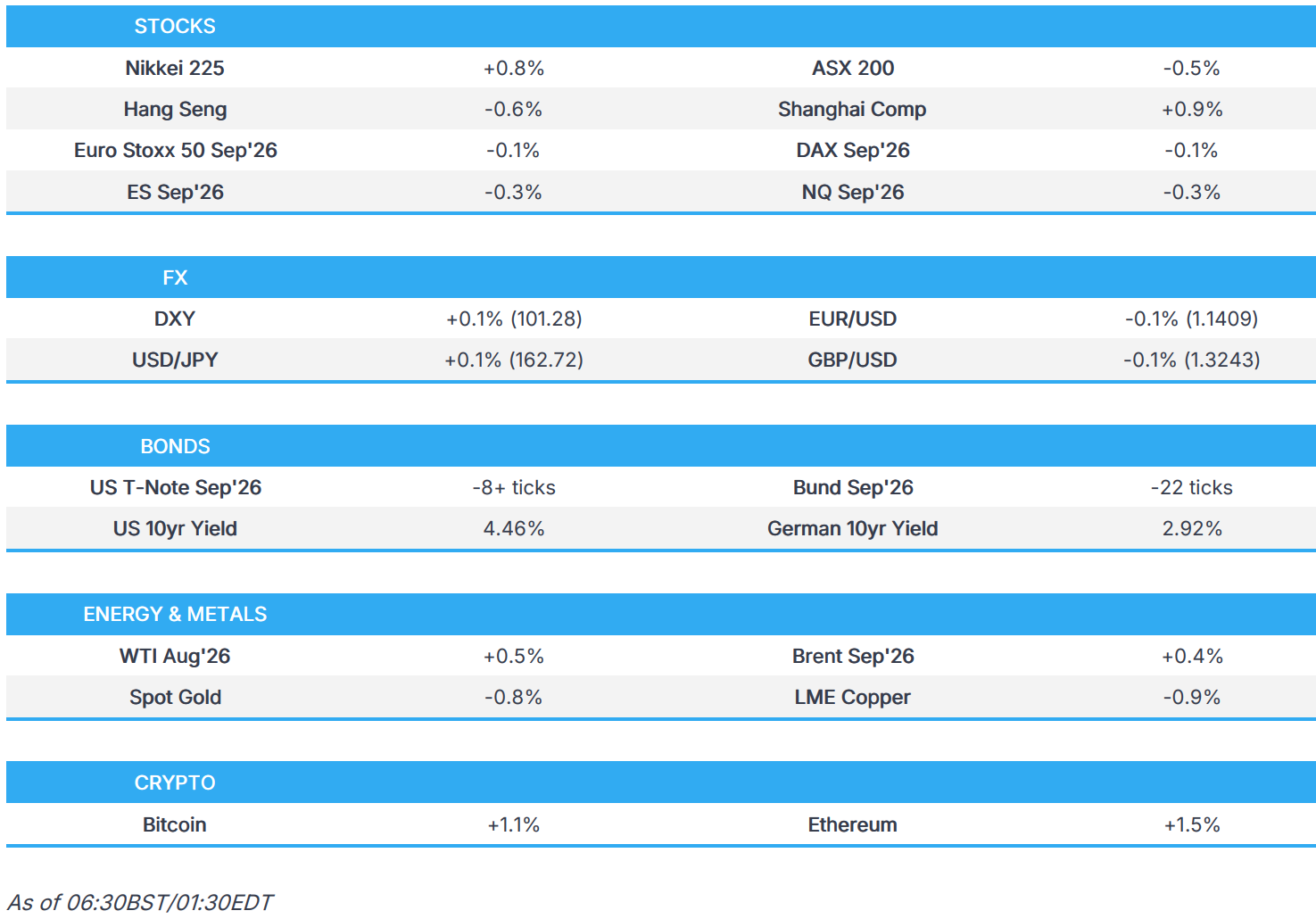

- APAC stocks were mixed, with outperformance in the Nikkei 225 after a solid Tankan survey; European equity futures are indicative of a slightly weaker open.

- DXY is mildly firmer into Fed Chair Warsh today; USD/JPY holds around 162.70, with top FX diplomat Mimura the latest to jawbone.

- Looking ahead, highlights include Global S&P Manufacturing PMI Final (Jun), EU Inflation Prelim. (Jun), US Challenger Job Cuts (Jun), ADP Employment Change (Jun), ISM Manufacturing PMI (Jun), Atlanta Fed GDP (Q2). Supply from the UK & Germany.

- Speakers include ECB's Vujcic, Cipollone, Lane & Lagarde, Fed's Warsh, BoE's Bailey, BoC's Macklem.

IRAN CONFLICT

- US President Trump was briefed on all-out war options on Iran, but opted to stick with talks, while he told aides he's okay if talks go past the August 18th deadline, according to WSJ.

- US VP Vance said President Trump is ready to drop bombs again, while he added that they have two options, which are either to pursue a long-term agreement with Iran on the condition that it changes its behaviour, or consolidate the gains that they made. Furthermore, he said Trump asked them to use the memorandum of understanding to resupply the global economy with oil, then they will see how things develop, and they want permanent, verifiable commitments from Iran regarding its nuclear disarmament.

- White House spokesperson Kelly stated that Trump remains firm that Iran cannot impose tolls on the international waterway, amid ongoing negotiations in Doha involving envoys Witkoff and Kushner.

- US admin official said the US has not released any of the USD 6bln in Iranian frozen funds, and won’t until Tehran “performs”, according to NY Post's Doornbos.

- US official said ships are transiting the Strait of Hormuz at higher levels.

- Iran's top negotiator Ghalibaf said the current meetings held by Iran are aimed at fulfilling MoU commitments, while Iran is committed to ensuring that passage through the Strait of Hormuz is carried out in accordance with Iranian arrangements. Ghalibaf also stated that America's commitment to end the war in Lebanon is a great victory, and noted that Iran is seeking to fulfil Article 13 of the Memorandum of Understanding in the current talks with the US, while he added they are ready for war if the other side does not want to fulfil its commitments in the talks. Furthermore, Ghalibaf separately commented that Iran has exported 40mln bbls of oil in less than two weeks.

- Iran's Foreign Ministry Spokesperson said the meeting on Wednesday in Doha will primarily focus on the release of blocked funds and the ceasefire in Lebanon.

- Oman presented a proposal regarding the future administration of the Strait of Hormuz to the US and other allies, while the proposal outlines a system for shipping companies to pay "service fees" for using the waterway, though sources differ on whether Oman is actively pushing for a fee-based structure, according to CNN citing sources.

- Qatar's PM and Foreign Minister met with US envoys Witkoff and Kushner, while they discussed the latest developments in the ongoing talks between the US and Iran, according to Qatar's Foreign Ministry.Furthermore, it was stated that Witkoff and Kushner affirmed Washington's commitment to the negotiating process and support for efforts aimed at reaching a comprehensive agreement.

- Spokesman for the Chief of General Staff of the French Armed Forces announced the deployment of the aircraft carrier Charles de Gaulle in the Gulf of Aden near the Strait of Hormuz.

- Israeli PM Netanyahu said that there are more peace agreements on the agenda, but also commented that Israel's war is 'never-ending' and confrontation with Iran is far from over

- Israeli Broadcasting Authority cited a source that stated the start of the pilot phase in Lebanon has been postponed until a monitoring mechanism is reached between the Lebanese and Israeli armies.

- News sources reported that the Israeli army carried out an explosive operation in the town of Beit Yahoun in southern Lebanon, according to Tasnim.

US TRADE

EQUITIES

- US stocks finished in the green on Tuesday, with outperformance in the Nasdaq driven by strength in the tech sector, while Industrials also rallied, although the picture was more mixed elsewhere, and the equal-weight S&P 500 closed flat. Furthermore, there was no obvious catalyst behind Tuesday's moves, with quarter-end rebalancing potentially providing support, while the latest JOLTS report reinforced the narrative of a resilient labour market ahead of Thursday's NFP report.

- SPX +0.78% at 7,499, NDX +1.69% at 30,276, DJI +0.26% at 52,318, RUT +0.52% at 3,026.

- Click here for a detailed summary.

TARIFFS/TRADE

- White House official said the Commerce Department was expected to lift export controls on Fable, while Commerce Secretary Lutnick confirmed they collaborated with Anthropic to review and authorise Fable 5.

- Mexico's Economy Minister said they don't think the USMCA treaty is to be scrapped.

- Mercosur and Japan are looking to expand market access for agricultural and non-agricultural goods, as well as cooperation and mutual investment.

NOTABLE HEADLINES

- US President Trump announced Pierre Yared will depart from the Council of Economic Advisers, while Trump separately announced approvals for several states regarding disaster relief.

- US President Trump’s administration is preparing a financial lifeline for smaller meatpackers struggling with dwindling cattle supplies that have pushed beef prices higher, according to WSJ. It was also reported that the US Agriculture Department is planning to provide up to USD 500mln in payments to small and medium-sized meatpacking companies, according to people familiar with the discussions.

- 'Big Short's' Michael Burry warned the AI rally is overextended, and he added bearish bets on NVIDIA (NVDA), Tesla (TSLA) and Applied Materials (AMAT), while he shorted Caterpillar (CAT) for the first time.

APAC TRADE

EQUITIES

- APAC stocks were mixed, in which bourses partially sustained the positive momentum from the tech-led gains on Wall St, where the S&P 500 and Nasdaq posted their best quarter in six years. The region also digested a slew of data, including the stronger-than-expected BoJ Tankan survey and numerous PMIs.

- ASX 200 was dragged lower by weakness in the consumer, financial, tech and telecom sectors, while sentiment was also not helped by a surprise contraction in Building Approvals data.

- Nikkei 225 rallied following the stronger-than-expected Tankan survey, which showed Large Manufacturing Sentiment was at the highest in 8 years, although the index gradually wiped out the majority of its gains amid intervention risks and as the data supported the case for the BoJ to continue normalising policy.

- KOSPI pared opening gains and lingered in the red as SK Hynix and Samsung Electronics retreated.

- Shanghai Comp was underpinned on the 105th anniversary of the founding of the Communist Party of China, and as participants digested the latest RatingDog Manufacturing PMI, which remained in expansion territory, while Hong Kong markets were closed for a holiday.

- US equity futures slightly pulled back following the prior day's tech-led momentum.

- European equity futures indicated a slightly lower cash market open with Euro Stoxx 50 futures down 0.1% after the cash market closed with gains of 1.6% on Tuesday.

FX

- DXY mildly strengthened amid recent upside in yields and ongoing Fed rate hike bets, while participants await looming key events, including comments from Fed Chair Warsh at Sintra later and Thursday's jobs data. On the latter points, US Treasury Secretary Bessent stating that he would not be surprised if June payrolls are very strong, although he had not seen the numbers.

- EUR/USD marginally weakened and reapproached the 1.1400 level to the downside following recent indecision and a slew of ultimately mixed ECB rhetoric.

- GBP/USD trickled lower after the recent choppy performance, but remained at the 1.3200 handle.

- USD/JPY edged higher after gaining a firmer footing north of the 162.00 level with the yen at its weakest in four decades, while there was a brief pullback after jawboning from Japan's top FX diplomat who stated that they are in touch with US counterparts more than most imagine and that recent intervention had meaning.

- Antipodeans pulled back overnight as the early positive momentum began to wane.

- PBoC set USD/CNY mid-point at 6.8067 vs exp. 6.7795 (prev. 6.8109).

- More central banks plan to reduce their US dollar holdings than increase them over the next decade for the first time, according to a global survey cited by CNN.

FIXED INCOME

- 10yr UST futures remained pressured after sliding yesterday as yields drifted higher across the curve as participants remained reluctant to price out the Fed's recent hawkish shift ahead of Thursday's Non-Farm Payrolls report, which Treasury Secretary Bessent touted to be a strong one. Attention today turns to several data releases and central bank speakers, including comments from Fed Chair Warsh at Sintra.

- Bund futures retreated following the prior day's whipsawing and slew of data, with prices not helped by the mild gains in energy prices and recent deluge of ECB rhetoric.

- 10yr JGB futures tracked the downside in global peers and with pressure seen after the stronger-than-expected BoJ Tankan survey and amid the ongoing intervention risk.

COMMODITIES

- Crude futures were rangebound after recent choppy trade as participants awaited any developments from Doha, where US and Iranian officials have travelled and are said to be conducting 'indirect' talks with mediators after Iran refused to meet with US envoys. Furthermore, prices were not helped by reports that Iran has exported as much as 50mln bbls of crude oil since the US-imposed blockade was lifted two weeks ago, while Iran's top negotiator said Iran had exported 40mln bbls in less than two weeks.

- US Private Inventory Data (bbls): Crude -6.1mln (exp. -4.1mln), Distillates +2.9mln (exp. -0.9mln), Gasoline -2.1mln (exp. -0.9mln), Cushing +0.5mln.

- Petrobras executive said they will cut diesel prices beginning July 1st.

- Spot gold trickled lower and returned to beneath the USD 4,000/oz level as the buck strengthened and yields climbed higher amid Fed rate hike bets.

- Copper futures retreated as the risk sentiment in Asia somewhat deteriorated.

CRYPTO

- Bitcoin gradually edged higher and returned to above the USD 59,000 level.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi stressed the party's commitment to serving the people in a speech commemorating the 105th CPC anniversary, while he reiterated absolute party leadership over the military and called for accelerated military modernisation.

- BoJ official noted regarding the recent Tankan survey that most firms replied before the US-Iran peace deal on June 15th, so the impact of the deal is likely not reflected much in the Tankan outcome.

- Japanese top FX diplomat Mimura said they are in touch with US counterparts more than most imagine and that a US official made supportive remarks about FX action, while he also commented that recent intervention had meaning.

DATA RECAP

- Japanese Tankan Large Manufacturers Index (Q2) 22 vs. Exp. 16 (Prev. 17)

- Japanese Tankan Large Manufacturing Outlook (Q2) 17 vs. Exp. 13 (Prev. 14)

- Japanese Tankan Large Non-Manufacturing Index (Q2) 37 vs. Exp. 35 (Prev. 36)

- Japanese Tankan Non-Manufacturing Outlook (Q2) 28 vs. Exp. 30 (Prev. 29)

- Japanese Tankan Large All Industry Capex (Q2) 11.5% vs. Exp. 11% (Prev. 3.3%)

- Chinese RatingDog Manufacturing PMI (Jun) 51.7 vs. Exp. 51.7 (Prev. 51.8, Low. 51, High. 52.3)

- Australian Building Permits MoM Prel (May) M/M -1.1% vs. Exp. 1.0% (Prev. -3.4%)

GEOPOLITICS

OTHER

- North Korean leader Kim pledged to deepen ties with China on shared socialist values and dispatched a congratulatory message to Chinese President Xi, on the Chinese Communist Party's founding anniversary, according to KCNA.

- Pakistan's air defence system shot down four rudimentary drones launched by Afghanistan's Taliban regime, while Pakistan's armed forces warned that continued provocation by the Taliban would be met with a befitting response that would cost them heavily.

EU/UK

NOTABLE HEADLINES

- French Presidential vote to be held on April 18th and May 2nd next year, with the official announcement expected on Wednesday, according to AFP citing sources.

- ECB's Demarco said the ECB should not rush into a further rate hike after the decline in oil prices, while he added the central bank can wait until next projections to decide if further hikes are needed, and that there are no signs of second-round effects, excessive wage pressures, or unanchored expectations.

- ECB's Dolenc said if current oil prices persist, the ECB may be able to wait until September before deciding whether further policy action is needed, adding there is no clear evidence of second-round inflation effects. Dolenc also commented that uncertainty around the Middle East is still elevated and a July ECB pause may be appropriate based on current data, while he added that there is no urgency to hike if energy prices stay subdued and that the situation can change quickly until the next meeting.

- ECB's Kazaks said there is no need for a forceful inflation response and the urgency of consecutive hikes is significantly lower. Kazaks also said it is too hard to say what'll happen in July and September, while he added that if things improve, it is possible that no hike will be warranted.