Published: 1 Jul 2026, 10:22 UTC

Newsquawk Desk

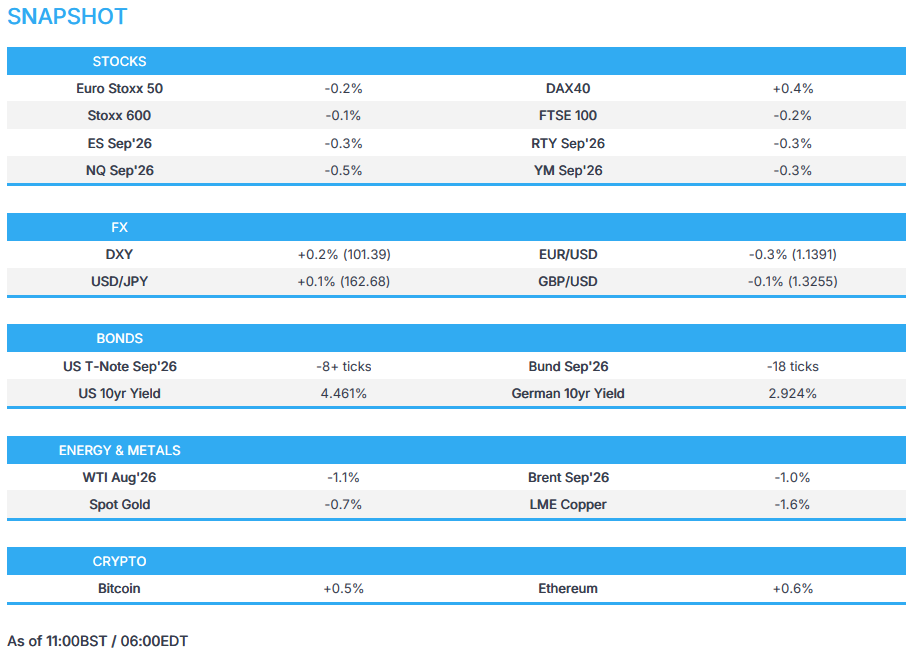

US Market Open: Crude slips as talks in Doha commence; Markets await the appearance of Fed Warsh at Sintra

0:00--:--

- Indirect US-Iran technical talks are reportedly underway in Doha, with Qatar and Pakistan acting as mediators. However, US envoy Witkoff and Kushner will not be attending the talks themselves.

- Iran is reportedly insisting on retaining control over the Strait of Hormuz and could charge ships to transit from mid-August, according to sources. The source added that Iran are not going to discuss other points until Hormuz is agreed.

- Global equities start Q3 with modest losses but off worst levels, with disappointing NKE outlook weighing on sporting names.

- DXY trades slightly firmer; G10s are softer across the board, AUD underperforms as metals continue to slump (XAU/USD -0.7%)

- Fixed income benchmarks weaker but off worst levels; EZ inflation surprise to the downside, briefly lifting EGBs.

- Crude futures fall as Doha talks begin (Brent -1.0%).

- Looking ahead, highlights include US ADP Employment Change (Jun), Revelio PLS (Jun), S&P Manufacturing PMI Final (Jun), ISM Manufacturing PMI (Jun), Atlanta Fed GDP (Q2), speakers include ECB's Lane & Lagarde, Fed's Warsh, BoE's Bailey, BoC's Macklem.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.1%) start Q3 on a softer footing, with Germany's DAX 40 (+0.4%) the only index printing modest gains; perhaps welcoming recent pension reform progress and the possible involvement of the Bundesbank. Final manufacturing PMI figures were broadly positive, with the majority of PMIs being revised higher. Commentary was relatively upbeat, with S&P stating that the sustained growth was accompanied by a welcome cooling of cost pressures.

- European sectors tilt to the negative side. Industrial Goods & Services (+0.5%), Technology (+0.5%) and Optimised Personal Care (+0.5%) are the top 3 sectors. To the downside lies Media (-1.7%), Consumer Products & Services (-1.5%) and Travel & Leisure (-0.1%).

- US equity futures are softer across the board, with underperformance in the NQ (-0.5%). Overnight, Business Insider reported that Microsoft (+1.6% pre-market) is planning to announce fresh job cuts of under 2.5%. Elsewhere, Nike (-4.0% pre-market) slips despite reporting strong headline metrics, though sales declined in China.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- Snapshot: G10s are mostly lower against the USD this morning, with clear underperformance in the Aussie, whilst the Kiwi fares a little better vs peers. USD/JPY continues to hold at elevated levels beyond the 162.50 mark, with further jawboning attempts seen overnight.

- DXY is firmer this morning and trades at the upper end of a 101.21-101.39 range (WTD peak at 101.43). The strength which comes amidst the markets’ continued hawkish shift at the Fed, seen following the last FOMC meeting. Markets also appear to be positioning for a hawkish commentary from Chair Warsh today, and then the NFP report on Thursday. On that note, Treasury Sec Bessent said he expects a strong jobs number, though clarified that he had not seen the report. Key releases today include: US ADP Employment, Challenge Job Cuts and ISM Manufacturing PMI.

- EUR and GBP have both been weighed on by the USD strength. The single currency has had a number of ECB members to digest, who are currently hosting the Sintra conference. Broadly speaking the remarks have been balanced, and with policymakers stressing data dependency heading into the July/September meetings. On the inflation front, today’s HICP release from the EZ saw the headline Y/Y cool from the prior (2.8% vs exp. 3%, prev. 3.2%). The Services figure also edged lower to 3.2% (prev. 3.5%). Some very mild pressure was seen in the EUR, and plays in favour of a hold in July. On the activity side of things, today’s Manufacturing PMI finals were subject to mild upward revisions, and the accompanying commentary was upbeat.

- JPY continues to remain in focus, with another jawboning attempt proving impotent. The latest attempt was by Top FX Diplomat who stated that Japan is in touch with US counterparts more than most imagine and that a US official made supportive remarks about FX action. This spurred some very mild pressure in the pair (05:30 BST / 00:30 EDT), falling from 162.79 to 162.56, before retracing about half of that move. A breach beyond the 163.00 mark could be difficult, given expectations that Japan may use the low-volume / holiday-thinned conditions on Friday (US Independence Day) to deliver effective intervention. Nonetheless, a hawkish Warsh and a strong NFP report on Thursday pose risk to the 163.00 level, which some have touted as the new “line in the sand”.

FIXED INCOME

- Global fixed income benchmarks are softer across the board, given Tuesday's post-settlement selloff. However, price action across the board has been range-bound, as markets look ahead to Fed Chair Warsh's first public appearance and updates from the US-Iran indirect Doha talks.

- Bunds (-18 ticks) have found support at the 127.00 handle, finding some stability after Tuesday's weakness, which was primarily driven by USTs. EZ inflation printed cooler than expected, with the headline figure at 2.8% Y/Y from 3.2% (exp. 3.0%) and ex-E, F, A & T dipping to 2.4% Y/Y from 2.6% (exp. 2.6%). Bunds did see some fleeting upside following the data, notching a new session high of 127.23 before falling back into the prior established daily range. ECB policymakers should find some comfort from the report, with some GC members starting to sound a bit more cautious on further rate hikes. On the supply front, a 2032 Bund auction was weak, with a poor b/c, though the average yield was less than the prior outing.

- USTs (-8+ ticks) oscillate in a narrow 109-18 to 109-23 band ahead of comments by Fed Chair Warsh at Sintra and the US jobs report on Thursday. Since his first remarks at the FOMC press conference, core PCE printed at 3.4% Y/Y, consumer confidence has surprised to the upside, and May payrolls printed strong (June payrolls due on Thursday). Given the backdrop, it would be hard for Warsh to soften his hawkish tone.

- OATs (-21 ticks) follow their European peers, but will come into greater focus as we near the Presidential elections in 2027. A date for the first round of elections has reportedly been set for April 18th, 2027, with a run-off set for May 2nd. The current President, Macron, cannot run in this election.

- Germany sells EUR 2.673bln vs exp. EUR 3.5bln 2.50% 2032 Bund: b/c 1.15x (prev. 2.4x), avg. yield 2.68% (prev. 2.8%), retention 23.6% (prev. 23.94%).

- UK sells GBP 1.25bln 0.125% 2031 I/L Treasury Gilt: b/c 4.26x (prev. 3.75x), real yield 0.933% (prev. 0.651%).

- Australia sells AUD 800mln 4.25% December 2035 bonds b/c 4.34, avg yield 4.748%

COMMODITIES

- A contained start for the energy complex, but with modest pressure emerging across the European morning. As the benchmarks pullback from the highs in yesterday’s session and the brief, but within existing ranges, uptick seen in the US late-afternoon as tensions flared somewhat. Currently, the waiting game continues amid the Doha gathering, but there is a positive skew to current expectations as the US and Iran are expected to hold in-direct talks and after President Trump’s openness to extending deadlines over taking military action.

- As the morning progressed the downside extended with participants looking to the Doha indirect meeting, and indeed sources since suggest that has commenced, no move on that latest report. Kushner and Witkoff are reportedly not involved in the technical exchange.

- Action that pushed Brent to a USD 71.62/bbl base, printing a fresh WTD low and falling below the USD 71.93/bbl trough. The next leg higher/lower will potentially be determined by the readout and/or sources around the talks, before we look to possible comments from President Trump or others on the state of relations.

- Spot gold saw pressure overnight, moving below the USD 4k/oz handle once again. The yellow metal is currently trading at the bottom-end of a USD 3,960-4,018/oz range, with the trough approaching the WTD low at USD 3,942/oz range. The recent pressure has been attributed to the markets’ continued hawkish shift at the Fed, stronger USD and rising US yields. Price action for the remainder of the day will be dictated by key US data (ADP/ISM Manufacturing) and Fed Chair Warsh.

- Base metals are entirely in the red, following the subdued risk sentiment seen in Asia, which has filtered through into the London session. 3M LME Copper (-1.67%) has traded lower throughout the day, and currently holds at the bottom end of a USD 13,134.08-13,384/t range.

- US Private Inventory Data (bbls): Crude -6.1mln (exp. -4.1mln), Distillates +2.9mln (exp. -0.9mln), Gasoline -2.1mln (exp. -0.9mln), Cushing +0.5mln.

- Petrobras executive said they will cut diesel prices beginning July 1st.

TRADE/TARIFFS

- The US is seeking alternative tungsten supplies to reduce reliance on China, according to the NYT.

NOTABLE EUROPEAN HEADLINES

- French Presidential vote to be held on April 18th and May 2nd next year, with the official announcement expected on Wednesday, according to AFP citing sources.

- UK Labour MPs reportedly want Burnham to appoint McFadden as Chancellor, in order to block Miliband, Huffington Post reported citing sources.

NOTABLE EUROPEAN DATA RECAP

- EU Inflation Rate YoY Flash (Jun) Y/Y 2.8% vs Exp. 3.0% (Prev. 3.2%, Low. 2.9%, High. 3.2%); Services 3.2% (prev. 3.5%).

- EU Inflation Rate MoM Flash (Jun) M/M -0.1% vs Exp. 0.1% (Prev. 0.1%).

- EU HICP ex-energy, food, alcohol & tobacco Y/Y Flash (Jun) Y/Y 2.4% vs. Exp. 2.6% (Prev. 2.6%).

- EU HICP ex-Food & Energy Y/Y Flash (Jun) 2.2% (prev. 2.3%).

- EU S&P Global Manufacturing PMI Final (Jun) 51.4 vs. Exp. 51.3 (Prev. 51.6, Low. 51.3, High. 51.6).

- German S&P Global Manufacturing PMI Final (Jun) 50.3 vs. Exp. 50 (Prev. 50.1, Low. 50, High. 50.1).

- French S&P Global Manufacturing PMI Final (Jun) 51.2 vs. Exp. 50.7 (Prev. 49.7, Low. 50.7, High. 50.7).

- Italian S&P Global Manufacturing PMI (Jun) 52.2 vs. Exp. 52.6 (Prev. 52.9).

- Spanish S&P Global Manufacturing PMI (Jun) 49.7 vs. Exp. 51 (Prev. 51.2).

- Swiss procure.ch Manufacturing PMI (Jun) 54.3 vs. Exp. 56.3 (Prev. 57.3).

- UK S&P Global Manufacturing PMI Final (Jun) 52.5 vs. Exp. 53.1 (Prev. 53.9).

- UK Nationwide Housing Prices YoY (Jun) Y/Y 2.2% (Prev. 1.7%).

- UK Nationwide Housing Prices MoM (Jun) M/M 0% vs. Exp. 0% (Prev. -0.6%).

CENTRAL BANKS

- ECB's Nagel pushed back on a "insurance hike" narrative in an interview with Bloomberg TV. He added that inflation will stay high in 2026 and remain above target in 2027, while stressing data dependency and a meeting-by-meeting approach. On the future rate path, he kept options open for July and September. He finished by stating that the first round effects continue, which increases the chance of second round effects and that he is currently seeing pass-through of first round effects on wages.

- ECB's Wunsch told Econostream that the case for further tightening is receding and any surprise in EZ inflation before the July meeting is more likely to be on the downside. He added he would need stronger second-round effects to justify further tightening and that one hike could suffice if shock fades before significant second-round effects. More than one hike to depend on more persistence and stronger second-round effects.

- ECB's Demarco said the ECB should not rush into a further rate hike after the decline in oil prices, while he added the central bank can wait until next projections to decide if further hikes are needed, and that there are no signs of second-round effects, excessive wage pressures, or unanchored expectations.

NOTABLE US HEADLINES

- US Challenger Job Cuts (Jun) 45.849K (Prev. 97.006K); cuts remain concentrated in tech, with AI continuing to reshape how companies think about headcount.

- White House official said the Commerce Department was expected to lift export controls on Fable, while Commerce Secretary Lutnick confirmed they collaborated with Anthropic to review and authorise Fable 5.

GEOPOLITICS

MIDDLE EAST

- Indirect US-Iran technical talks are reportedly underway in Doha, with Qatar and Pakistan acting as mediators. The sessions are to involve chief negotiators and specialist teams, sources suggest, however US envoy Witkoff and Kushner will not be attending the talks themselves.

- Iran is reportedly insisting on retaining control over the Strait of Hormuz, according to sources citing a senior Iranian official. Could see a recommence charging ships to transit from mid-August and are not going to discuss other points until Hormuz is agreed.

- US President Trump was briefed on all-out war options on Iran, but opted to stick with talks, while he told aides he's okay if talks go past the August 18th deadline, according to WSJ.

- US VP Vance said President Trump is ready to drop bombs again, while he added that they have two options, which are either to pursue a long-term agreement with Iran on the condition that it changes its behaviour, or consolidate the gains that they made. Furthermore, he said Trump asked them to use the memorandum of understanding to resupply the global economy with oil, then they will see how things develop, and they want permanent, verifiable commitments from Iran regarding its nuclear disarmament.

- US admin official said the US has not released any of the USD 6bln in Iranian frozen funds, and won’t until Tehran “performs”, according to NY Post's Doornbos.

- US official said ships are transiting the Strait of Hormuz at higher levels.

- Iran State Media said that a foreign container ship ran aground in the Strait of Hormuz after using a route which was undesignated by Iran.

- Oman presented a proposal regarding the future administration of the Strait of Hormuz to the US and other allies, while the proposal outlines a system for shipping companies to pay "service fees" for using the waterway, though sources differ on whether Oman is actively pushing for a fee-based structure, according to CNN citing sources.

- Qatar's PM and Foreign Minister met with US envoys Witkoff and Kushner, while they discussed the latest developments in the ongoing talks between the US and Iran, according to Qatar's Foreign Ministry.

- Israeli Broadcasting Authority cited a source that stated the start of the pilot phase in Lebanon has been postponed until a monitoring mechanism is reached between the Lebanese and Israeli armies.

- Israeli Defence Minister Katz said the IDF will remain in the security zones in Lebanon, Syria and Gaza.

- UKMTO said it received a report of an incident 76NM south of Yemen; the vessel being approached by multiple small craft but the crew reported safe.

OTHER

- North Korean leader Kim pledged to deepen ties with China on shared socialist values and dispatched a congratulatory message to Chinese President Xi, on the Chinese Communist Party's founding anniversary, according to KCNA.

- Pakistan's air defence system shot down four rudimentary drones launched by Afghanistan's Taliban regime, while Pakistan's armed forces warned that continued provocation by the Taliban would be met with a befitting response that would cost them heavily.

CRYPTO

- Bitcoin briefly dipped below last week's trough of USD 58k before bidding slightly higher and currently nearing USD 59k.

- Citigroup cuts its 12-month Bitcoin forecast to USD 82,000 from a prior forecast to USD 112,000, while it cut its 12-month Ethereum forecast to USD 2,240 from a previous USD 3,175

APAC TRADE

- APAC stocks were mixed, in which bourses partially sustained the positive momentum from the tech-led gains on Wall St, where the S&P 500 and Nasdaq posted their best quarter in six years. The region also digested a slew of data, including the stronger-than-expected BoJ Tankan survey and numerous PMIs.

- ASX 200 was dragged lower by weakness in the consumer, financial, tech and telecom sectors, while sentiment was also not helped by a surprise contraction in Building Approvals data.

- Nikkei 225 rallied following the stronger-than-expected Tankan survey, which showed Large Manufacturing Sentiment was at the highest in 8 years, although the index gradually wiped out the majority of its gains amid intervention risks and as the data supported the case for the BoJ to continue normalising policy.

- KOSPI pared opening gains and lingered in the red as SK Hynix and Samsung Electronics retreated.

- Shanghai Comp was underpinned on the 105th anniversary of the founding of the Communist Party of China, and as participants digested the latest RatingDog Manufacturing PMI, which remained in expansion territory, while Hong Kong markets were closed for a holiday.

NOTABLE ASIA-PAC HEADLINES

- Japanese top FX diplomat Mimura said they are in touch with US counterparts more than most imagine and that a US official made supportive remarks about FX action, while he also commented that recent intervention had meaning.

- BoJ official noted regarding the recent Tankan survey that most firms replied before the US-Iran peace deal on June 15th, so the impact of the deal is likely not reflected much in the Tankan outcome.

NOTABLE APAC DATA RECAP

- Japanese Tankan Large Manufacturers Index (Q2) 22 vs. Exp. 16 (Prev. 17)

- Japanese Tankan Large Manufacturing Outlook (Q2) 17 vs. Exp. 13 (Prev. 14).

- Japanese Tankan Large Non-Manufacturing Index (Q2) 37 vs. Exp. 35 (Prev. 36).

- Japanese Tankan Non-Manufacturing Outlook (Q2) 28 vs. Exp. 30 (Prev. 29).

- Japanese Tankan Large All Industry Capex (Q2) 11.5% vs. Exp. 11% (Prev. 3.3%).

- Japanese Consumer Confidence (Jun) 33.8 vs. Exp. 34 (Prev. 33.6).

- Japanese S&P Global Manufacturing PMI Final (Jun) 54.8 vs. Exp. 54.9 (Prev. 54.5).

- Chinese RatingDog Manufacturing PMI (Jun) 51.7 vs. Exp. 51.7 (Prev. 51.8, Low. 51, High. 52.3).

- Australian Building Permits MoM Prel (May) M/M -1.1% vs. Exp. 1.0% (Prev. -3.4%).