Published: 2 Jul 2026, 10:17 UTC

Newsquawk Desk

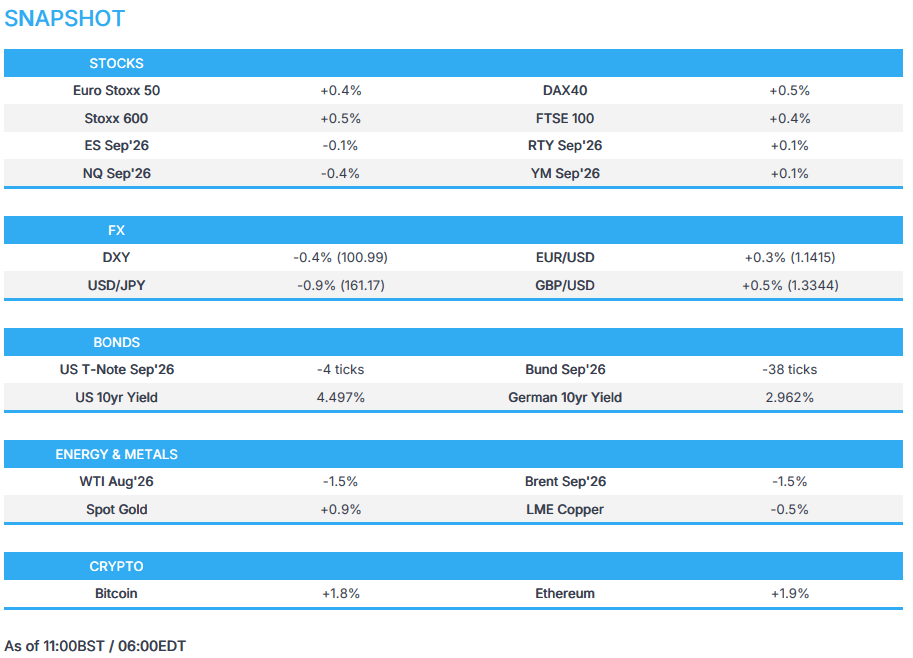

US Market Open: DXY slips below 101.00, weighed on by possible JPY intervention; US jobs report awaits

0:00--:--

- Qatar and Pakistan mediators concluded separate meetings with US and Iranian negotiators in Doha, highlighting positive progress on issues related to the Islamabad MoU.

- US equity futures trade mixed, with the NQ weighed by tech selling in South Korean stocks.

- DXY slips below the 101.00 handle, as the JPY strengthens on possible intervention.

- Fixed income benchmarks trade on the softer side heading into the US jobs report; NFP expected at 110K.

- Crude benchmarks continue to trade lower, Brent -1.5%.

- Looking ahead, highlights include US Jobs Report (Jun), Initial Jobless Claims, Speakers including ECB's Cipollone, BoE's Mann and Fed's Daly.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.5%) initially started Thursday's trade on a softer footing but have climbed off their lows, with all indices in the green, outside of the AEX (-0.3%). Sentiment overnight was on the softer side, following another tech selloff in South Korean stocks (Samsung -9.1%, SK Hynix -14.6%) after Meta plans to sell excess AI compute to build a cloud business, raising questions over excess in AI capacity. However, with Europe lacking the big AI giants, this seems to support the Euro area.

- European sectors point to a positive bias. Optimised Personal Care (+2.1%) tops the sector pile, followed by Food, Beverages & Tobacco (+2.0%) and Health Care (+1.5%). As expected, Technology (-1.9%) is the clear sector laggard and the only sector in the red.

- US equity futures are softer across the board, with the NQ lagging as it gets weighed on by the tech selloff in Asia. Losses have extended into chip names (NVDA -0.8% / AMD -1.3%) and memory (SanDisk -3%, Micron -1.7%).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY trades lower this morning, and trades at the bottom end of a 100.95 to 101.43 range. Pressure which comes after the lack of hawkish remarks from Fed Chair Warsh at Wednesday's policy panel, and with the move further exacerbated by a hefty move in the JPY this morning.

- On that front, this morning saw large and immediate selling pressure in USD/JPY, where the pair fell from 162.20 to a trough of 161.12. The pair then pared back about a third of that move, stabilising around 161.80, before then taking another beating towards the session low of 160.89 – now trading at levels not seen since 18 June.

- Given the sheer size of the move lower, it does appear to be the case that this is potentially intervention, rather than a rate check. Details of whether they enacted a form of intervention will be released in the monthly release, which is released on the last business day of every month.

- The move comes after Reuters reported that Japan would abandon its habit of warning the markets of intervention. The aim of this is to squeeze speculators and increase the cost of betting against the JPY.

- The potential intervention comes ahead of today’s NFP report; a USD positive report could see some of the “potential intervention” move be pared back. To preview the report in brief, US non-farm payrolls for June are expected to print 110K (prev. 172K), with the unemployment rate seen unchanged at 4.3%.

- Other G10s are stronger against the USD this morning. JPY unsurprisingly outperforms, followed by the GBP and CHF. For the latter, Switzerland reported in-line/cooler-than-expected inflation metrics, which broadly play in favour of keeping rates on hold for the foreseeable future.

FIXED INCOME

- Global fixed income benchmarks trade on a softer footing ahead of the US payrolls data while Germany announces a new set of reforms.

- USTs (-3 ticks) are lower by a handful of ticks, trading just shy of Wednesday's low of 109-12+. Looking ahead to the June jobs report; NFP expected at 110K (prev. 172K), unemployment to hold steady at 4.3%, average hourly earnings Y/Y expected at 3.5% (prev. 3.4%). In terms of technical levels, downside levels include 109-16 (prior week's low), 108-27 (key support level) and 108-10 (worst low seen due to Iran conflict). 110-00+ is the key level to the upside.

- Bunds (-38 ticks), unlike USTs, have extended on Wednesday's trough, currently trading at the lower end of its 126.78-127.06 range. German Chancellor Merz's coalition unveiled a package of reforms earlier, which included EUR 10bln in annual tax relief for lower-income earners, changes to the pension system and building more affordable housing. The overall aim is to restore competitiveness in Europe's biggest economy. Although the move lower in German debt has not been excessive, it could be a potential reason for the downside in German debt, as it brings growth back into the economy.

- OATs (-34 ticks) follow their German counterpart. In the upcoming months, French debt will be more in focus as the Presidential elections near. Political uncertainty continues to remain. More recently, the Green Party announced that it would put forward a motion of no confidence over the government's handling of the recent heat wave. However, this attempt to bring down PM Lecornuʼs government is likely to fail without the support of other opposition parties. The preference for German debt over OATs is clearly shown in the spread, currently trading at 75bps, up from the 58bps seen at the start of June.

- The UK sells GBP 3.25bln 4.625% 2037 Green Gilt: b/c 3.31x (prev. 3.63x), average yield 4.934% (prev. 4.975%), tail 0.2bps (prev. 0.2bps).

- France sells EUR 14.0bln vs exp. EUR 12.5-14bln 1.25% 2036, 3.70% 2036, 4.50% 2041 and 4.10% 2046 OAT.

- Spain sells EUR 5.958bln vs exp. EUR 5-6bln 2.60% 2031, 3.25% 2034 and 3.40% 2036 Bono and EUR 0.695bln vs exp. EUR 0.25-0.75bln 1.15% 2036 I/L Bono.

- Japan sells JPY 1.96tln 10yr JGBs, b/c 3.13x (prev. 3.53x), average yield 2.729% (prev. 2.649%).

COMMODITIES

- Crude benchmarks are on the backfoot, after mediators suggested positive progress was made in the US-Iran indirect conversation. Conversely, gas benchmarks continue to rise with Dutch TTF above EUR 44/MWh as the European forecast points to renewed heat.

- Brent down to a USD 70.38/bbl base, though it has reverted back towards the USD 71.00/bbl but remains in the red. The mentioned base is the lowest print since the end of February, when USD 70.20/bbl printed for the September contract. ,

- For today, US NFP will dominate the macro narrative, with a full Newsquawk preview available. Specifically for energy, we await any further update from the US-Iran talks, and while the mediator-led exchange has now concluded, we could still see updates as the parties agreed to continue talks over the “coming period”.

- Spot gold at a USD 4080/oz peak. In a recovery from the move below USD 4k/oz seen in the last two sessions. Upside today is a function of a weaker USD and relatively steady UST action. As above, impetus will come from the US NFP report.

- Base peers are under pressure, despite the constructive European risk tone and the mentioned USD pressure. As the complex follows the downbeat performance seen in mainland China overnight, and despite Hong Kong seeing strength on its holiday return.

- US President Trump posted that oil prices are plummeting fast and gas prices at the pump are dropping too, but not as fast as they should be, while he announced the Freedom Fuel Network will be lowering gas prices at 25 “FREEDOM FUEL” stations across the Greater Philadelphia Area.

- Venezuela's oil production was expected to recover to 1.1mln-1.2mln BPD by the end of Q2 2026 as the US expands export authorisations, allowing more companies to transport and market Venezuelan crude

- Saudi Aramco has reportedly increased its exports from the Ras Tanura port and have shifted to spot sales, according to sources.

- Hengli Petrochemical has reportedly cancelled its recent purchases of West African and Middle East oil purchases and also cut refinery operations, according to Reuters sources.

- Dubai spot crude's discount to swaps widened to more than USD 4.00/bbl, the largest gap since May 2020, according to Refinitiv data.

- UBS cuts its end-2026 gold forecast to USD 5k/oz, due to elevated interest rates.

TRADE/TARIFFS

- China's MOFCOM said China and the EU agreed to up to two annual ministerial trade talks and have invited EU's Trade Commissioner Sefcovic to visit in the Fall.

NOTABLE EUROPEAN HEADLINES

- Germany's ruling coalition unveiled a package of reforms, including EUR 10bln in annual tax relief for lower-income earners, changes to the pension system and building more affordable housing.

- Germany's VDMA reported May industrial orders -1% Y/Y, driven by weak domestic demand and a general decline across the EZ.

NOTABLE EUROPEAN DATA RECAP

- Swiss Inflation Rate YoY (Jun) Y/Y 0.5% vs. Exp. 0.5% (Prev. 0.6%, Low. 0.3%, High. 0.6%).

- Swiss Inflation Rate MoM (Jun) M/M 0% vs. Exp. 0.1% (Prev. 0.2%).

NOTABLE US HEADLINES

- The Trump administration is reportedly ready to launch "Trump Accounts" next week, but not allow firms to host children's savings accounts on their own systems, Semafor reported citing sources.

- OpenAI has discussed giving a 5% to the US government as the AI startup seeks to clear political obstacles by securing financial buy-in from the Trump administration, according to FT.

GEOPOLITICS

MIDDLE EAST

- US official said the US is hopeful that Iran will come to the table to negotiate seriously, but is prepared to walk away if they do not, according to a New York Post reporter on X

- US has informed Iran that changing the status quo around the Strait of Hormuz would be a violation of the current understanding and would be unacceptable, according to Al Arabiya sources.

- Iran said it will respond to US interventions in the Strait of Hormuz, Fars reported.

- Qatar's Foreign Ministry said Qatar and Pakistan mediators concluded separate meetings with US and Iranian negotiators in Doha, while it added that positive progress was made on issues related to the Islamabad MoU. It also stated that the parties agreed to continue discussion over the coming period, with the next meeting to be scheduled at the earliest possible time following the funeral processions of the former Iranian supreme leader.

- Iranian Parliament Speaker Ghalibaf said the claim that inspectors of the IAEA have access to the sites that were bombed is false, while he added that under no circumstances will access be granted to sites that were bombed and damaged.

- Iran's Deputy Foreign Minister Gharibabadi said Doha talks focused on US violations of the MoU and frozen assets. Gharibabadi separately commented that the Strait of Hormuz is defined under Iran's command, not CENTCOM, as well as stated that regional security is ensured by the end of interference and the departure of the US from the region, respect for the sovereignty of countries and acceptance of new geopolitical realities, not under the military umbrella of the US.

- Senior source told Al-Hadath that Iran is allowed to purchase American agricultural products using a portion of its frozen funds, but noted that no cash payments are to be dispersed to Iran

- Lebanon's PM said negotiations with Israel lack a deal framework, and the government seeks a timeline for Israel's withdrawal and insists on exclusive state control of weapons

- Israeli drones struck Al-Dir in southern Lebanon and Israeli shelling was also reported on the outskirts of Quneitra in Syria, while Israeli forces conducted night raids in Jenin and Ramallah, in the West Bank.

RUSSIA-UKRAINE

- Russian Armed Forces said it hit a Kyiv plant that produces control systems for specific missiles, RIA reported.

- Russian Defence Ministry said it shot down 327 Ukrainian drones overnight.

- Air defence systems were reportedly repelling a Russian drone attack on Kyiv, while it was separately reported that multiple explosions were heard in Ukraine's capital which was under ballistic missile attack.

- Ukrainian military said it has struck the Kstovo oil refinery in Russia.

OTHER

- China warned two Japanese Coast Guard survey vessels to stop conducting maritime surveys in the disputed East China Sea, prompting Japan to lodge a formal diplomatic protest.

CRYPTO

- Bitcoin extends further above USD 60k and briefly extended above USD 61k, currently trading at the top end of its USD 59.52k-61.12k range.

APAC TRADE

- APAC stocks were mixed but with the major indices predominantly in the red following the tech-related losses on Wall St, while participants also brace for the incoming Non-Farm Payrolls report in a holiday-shortened trading week stateside.

- ASX 200 was rangebound as strength in the top-weighted financial sector was offset by losses in the utilities, tech, energy and consumer sectors, while sentiment was also not helped by weak Australian trade data.

- Nikkei 225 retreated at the open amid tech selling and recent upside in yields, although the index then staged a partial rebound, before selling resumed later in the session.

- KOSPI slumped amid the pressure in memory chip stocks, and triggered a sidecar in early trade.

- Hang Seng and Shanghai Comp traded mixed with the mainland conforming to the broad risk-off mood, while the Hong Kong benchmark bucked the trend amid strength in local tech, biopharmaceutical and auto names on return from the holiday closure.

NOTABLE ASIA-PAC HEADLINES

- Japan's Government Panellist Nagahama said that the BoJ should raise rates once every six months; this would not hurt domestic investment.

NOTABLE APAC DATA RECAP

- Australian Trade Balance (May) -3.0B vs. Exp. 2.3B (Prev. 1.8B).

- Australian Exports MM (May) -6.9% (Prev. 7.2%).

- Australian Imports MoM (May) M/M 2.6% (Prev. 0.8%).

- South Korean Inflation Rate YoY (Jun) Y/Y 3.2% vs. Exp. 3.2% (Prev. 3.1%).

- South Korean Inflation Rate MoM (Jun) M/M 0.1% vs. Exp. 0.1% (Prev. 0.5%).