Published: 3 Jul 2026, 05:47 UTC

Newsquawk Desk

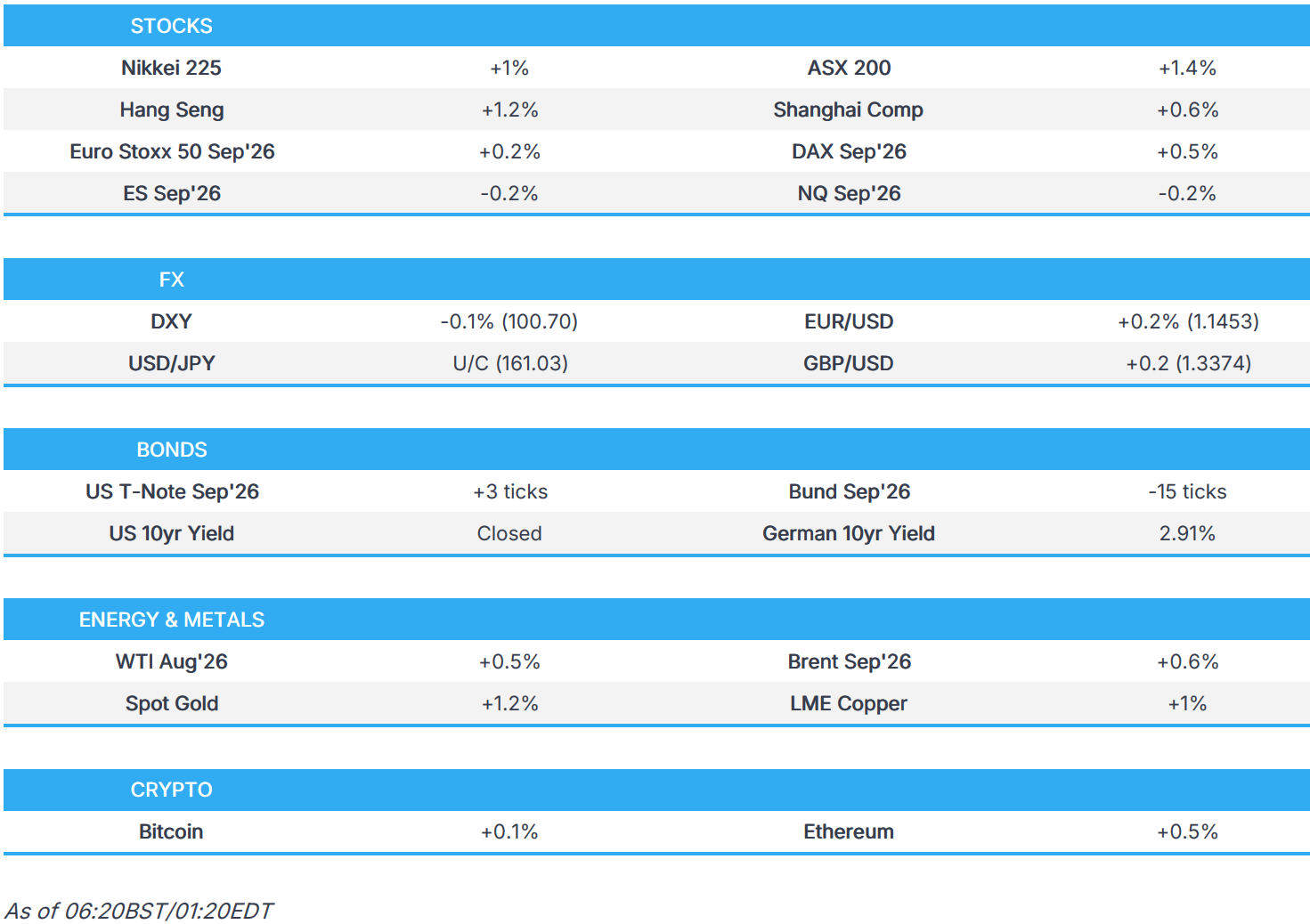

EU Market Open: KOSPI (+4.8%) rebounds from recent losses, and European equity futures indicative of a firmer open; USD/JPY holds near recent lows

0:00--:--

- US President Trump warned that Iran has some missiles left and that they could wipe those out. It was separately suggested that Trump made it clear Iran cannot impose fees on the Strait of Hormuz.

- APAC stocks gained, with strength seen in the KOSPI (+4.6%); European equity futures are indicative of a slightly firmer open.

- DXY traded subdued at around 100.70; USD/JPY holds just above the 161.00 mark, taking a breather following recent pressure.

- US and China are moving towards reducing tariffs on each other's agricultural products, Semafor reported.

- Highlights include Global S&P Services/Composite PMI Final (Jun), BoE DMP (Jun), Speakers including ECB's Lagarde & BoE's Bailey.

- Holiday: US Independence Day. Newsquawk audio and headline service will stop at 18:15BST/13:15EDT, however, Newsquawk widgets will continue to function as usual.

IRAN CONFLICT

- US President Trump reiterated that they can't let Iran have a nuclear weapon, while he stated that Iran has some missiles left and that they could wipe those out, while he thinks that Iran has agreed to about everything they need.

- US senior admin official says Strait of Hormuz is open and ship traffic through it is proceeding at a high rate, while the official added that President Trump made it clear Iran cannot impose fees on the Strait of Hormuz, which is an international waterway, and that active talks are continuing at high levels regarding all aspects of the MOU.

- US officials believed that Israel might have been plotting to kill Iran’s top negotiators while Washington was engaged with Tehran in delicate talks this spring to reach an interim peace deal, according to current and former US officials cited by NYT.

- Israeli fighter jets carried out an airstrike on the town of Baraachit in southern Lebanon, while large explosions were reported in northern Gaza, as Israel conducted operations east of the Jabalia camp.

US TRADE

EQUITIES

- US stocks were mixed, with the Dow the only major index to finish in positive territory, while the Nasdaq closed lower and the S&P 500 was flat. Although the softer-than-expected June nonfarm payrolls report saw traders pare Fed rate hike expectations, helping support broader risk sentiment, renewed weakness in large-cap technology stocks outweighed the macro tailwind for NDX. Market breadth was notably more constructive than the headline indices suggested. The majority of sectors finished higher, led by the traditional defensive sectors of Health Care, Consumer Staples and Utilities, while the heavyweight Technology, Consumer Discretionary and Communication Services sectors were the clear laggards. There was no obvious catalyst behind the renewed selling in technology shares, although the move may have reflected a continuation of Wednesday's weakness following the Meta disruption. Meanwhile, memory stocks remained under pressure, with the DRAM ETF falling 7.7%, while the Semiconductor ETF (SOXX) declined 5.6%. Elsewhere, Tesla (TSLA -7.5%) shares plummeted despite stronger-than-expected delivery numbers. It is also possible that some profit-taking and position squaring took place ahead of the long Independence Day weekend, with US markets closed on Friday.

- SPX -0.01% at 7,483, NDX -1.61% at 29,329, DJI +1.14% at 52,904, RUT -0.55% at 2,996.

- Click here for a detailed summary.

TARIFFS/TRADE

- US and China are moving towards reducing tariffs on each other's agricultural products, while a reduction in tariffs could open the door for China to ramp up purchases of US soybeans, according to Semafor citing officials.

NOTABLE HEADLINES

- US President Trump said Fed chair Warsh has a board that is a little bit hostile, and that Warsh has to do what he has to do, while he added that growth can be good for inflation, not just bad. Trump stated he could get Fed's Cook off the board by winning the case and will start a perfect removal procedure for removing her. Trump reiterated praised for the stock market when questioned about his finances, while he said he doesn't do anything related to his businesses and lets people invest his money, as well as noted that he has some stock in NVIDIA (NVDA) and thinks it’s very small.

- US Treasury Secretary Bessent said to expect to see real wage gains as soon as June and that he is hopeful gas prices will drop to USD 3/gallon by Labor Day, while he added that gas prices are a little stickier on the way down.

APAC TRADE

EQUITIES

- APAC stocks were in the green as sentiment gradually improved from the initial tech-related jitters that rolled over from the US, where the major indices were mixed as weaker-than-expected jobs data eased rate hike concerns and helped the DJIA notch a fresh all-time high, but the Nasdaq lagged on tech selling.

- ASX 200 climbed higher with the mining, materials, healthcare and resources sectors front-running the advances, and atoning for the weakness in utilities, energy, tech and telecoms.

- Nikkei 225 dipped at the open alongside tech pressure, but then pared the almost 1000-point drop to return to above the 69,000 level.

- KOSPI shrugged off the initial weakness with the fluctuation in the index, largely a reflection of the tech sector and swings in the SK Hynix shares. Set to end the APAC session with gains of c. 4.6%, with the likes of Samsung (+8.9%) and SK Hynix (+8.8%) both soaring.

- Hang Seng and Shanghai Comp conformed to the upbeat mood amid the rising tide across Asia-Pac stocks and as participants also digested better-than-expected Chinese RatingDog Services PMI data.

- US equity futures gained with Nasdaq futures bouncing back from yesterday's underperformance.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.3% after the cash market closed with gains of 1.2% on Thursday.

FX

- DXY remained subdued after retreating on the softer-than-expected NFP report, which eased some rate hike concerns and resulted in a pushback of the timing of the first fully priced-in Fed rate hike to December from October. Nonetheless, the downside was limited overnight with US markets shut on Friday ahead of Independence Day, and as such, trading conditions are set to be thinner.

- EUR/USD mildly benefited from the dollar weakness and with very little fresh catalysts for the single currency, while ECB's Lagarde said she was confident the ECB had made the right decision by raising interest rates in June, and stated that second-round inflation effects had not materialised.

- GBP/USD held on to recent spoils and is on track for a seventh consecutive daily gain, while there were some remarks from the likely next UK PM, Andy Burnham. He stated that he will stick to the Labour manifesto on tax and has not made up his mind on who his chancellor will be, but also commented that there is 'room for movement on tax' in Labour's manifesto.

- USD/JPY lingered near the prior day's trough after the recent outperformance of the Japanese currency and potential JPY intervention on Thursday, while Japanese officials continued with their regular jawboning. Looking to start the London session around the 161.00 mark.

- Antipodeans mildly strengthened amid the positive risk environment and upside in commodity prices.

- PBoC set USD/CNY mid-point at 6.8047 vs exp. 6.7808 (prev. 6.8088)

FIXED INCOME

- 10yr UST futures kept afloat following the prior day's steepening as money markets pushed back the first fully priced in Fed rate hike to December from October following the weaker-than-expected jobs report, while price action is contained overnight with US cash markets shut on Friday ahead of July 4th celebrations.

- Bund futures were lacklustre after recent indecision and with little reaction seen following comments from Lagarde that she was confident the ECB had made the right decision by raising interest rates in June, as well as stated that second-round inflation effects had not materialised.

- 10yr JGB futures rebounded from a one-month low, but with little fresh catalysts, while Japanese officials continue to echo the familiar rhetoric regarding policy and responding to currency moves.

COMMODITIES

- Crude futures gradually edged higher amid the positive risk appetite, but with price action contained in the absence of any fresh significant geopolitical headlines.

- Canadian PM Carney said the government agreed with Alberta that the best route for a new pipeline is south through the Trans Mountain corridor to the Pacific coast, while the government, Alberta and Oil Sands Alliance agreed on terms to launch the Pathways project. Furthermore, the Alberta government announced that work on the new West Coast pipeline may commence on September 1, 2027

- Baker Hughes Rig Count: Oil +5 to 445, Gas +1 to 126, Total +7 to 580.

- Spot gold extended on gains and approached just shy of the USD 4,200/oz following recent dollar weakness and an unwinding of Fed rate hike bets due to the weaker-than-expected US jobs report.

- Copper futures were lifted overnight as risk sentiment gradually improved in the Asia-Pac region.

CRYPTO

- Bitcoin was choppy and kept to within a relatively tight range above the USD 61,000 level.

NOTABLE ASIA-PAC HEADLINES

- China's MOFCOM said it welcomes UK companies to invest in China, and hopes the UK will adjust the steel trade measure, while it hopes the UK provides a fair environment for Chinese firms, as well as stated that Chinese and UK firms can deepen cooperation in the service sector.

- Anthropic moves to shut loopholes that allow Chinese access to Claude, according to FT.

- Japanese Finance Minister Katayama won't comment on specific FX levels, but reiterated they are ready to respond appropriately to currency moves and will conduct appropriate economic policy. Furthermore, she stated that they will conduct fiscal policy with efforts to gain market trust, when asked about higher JGB yields, as well as noted that specific monetary policies are up to the BoJ and they expect the BoJ to conduct appropriate monetary policy while coordinating with the government.

- Japanese Trade Minister Akazawa affirmed there are various factors that drive FX rates, but made no specific comment, while he stated they need to monitor and respond to the FX impact on small firms.

DATA RECAP

- Chinese RatingDog Services PMI (Jun) 54.1 vs. Exp. 53.6 (Prev. 54.4)

- Chinese RatingDog Composite PMI (Jun) 53.6 (Prev. 54.0)

GEOPOLITICS

RUSSIA-UKRAINE

- Industrial facility in Russia's Belgorod was reportedly on fire after a Ukrainian strike.

OTHER

- US President Trump posted an image showing US contributions to NATO and stated, "Ridiculous for the U.S.A. to continue along this one sided path when the relationship is not reciprocal. They were not there for us!!!"

EU/UK

NOTABLE HEADLINES

- UK MP Burnham said he will stick to the Labour manifesto on tax and has not made up his mind on who his chancellor will be, while he stated he is not undisciplined when it comes to public finances and will take responsibility to fully fund the defence spending plan. Furthermore, Burnham ruled out 'crude' short-term welfare cuts and said education reforms and more council houses will eventually bring down the number of jobless youngsters, but also stated there is 'room for movement on tax' in Labour's manifesto.

- UK MP Burnham's policy guru suggested cuts and reducing eligibility is the wrong approach to reform welfare, according to Sky News's Coates.

- BoE's Mann said the loosening in financial conditions since June, would be an important factor in determining her vote at the next policy meeting.

- German Chancellor Merz said the reform package could lift German 2027 GDP to at least 1%.

- ECB President Lagarde said she was confident the ECB had made the right decision by raising interest rates in June, adding that second-round inflation effects had not materialised.