Published: 6 Jul 2026, 06:05 UTC

Newsquawk Desk

EU Market Open: Europe primed for quiet open with newsflow light; USD/JPY remains on intervention watch

0:00--:--

- Asia-Pac stocks initially started the session with broad gains, but later reversed. Crude futures started the week on the back foot.

- Islamabad is the more likely option for the next round of US-Iran technical talks, with July 11th expected to be the date, Fox reported.

- OPEC+ agreed to raise output targets by an additional 188k bpd, in line with the group's plan to reverse output curbs.

- Ship-tracking data showed that at least 8 ships attempting to leave the Strait of Hormuz turned back, with the reasons unknown.

- European equity futures are indicative of a flat/slightly softer open with the Euro Stoxx 50 futures down 0.1% after cash closed +0.8% on Friday.

- Looking ahead, highlights include German Factory Orders (May), EU Retail Sales (May), US S&P Services/Composite PMI Final (Jun), and ISM Services PMI (Jun). Speakers include Fed's Waller, BoE's Mann, ECB's Schnabel, Lagarde and Lane.

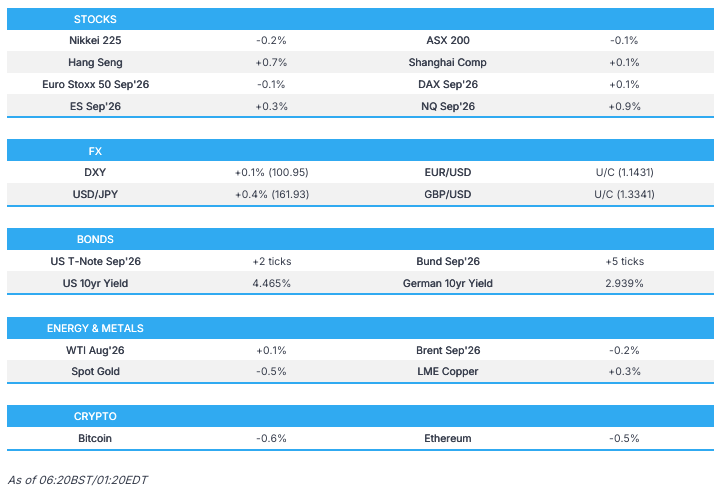

SNAPSHOT

US TRADE

EQUITIES

- US stocks were closed on Friday for US Independence Day.

TARIFFS/TRADE

- New Zealand's Trade Minister said they will begin negotiations with Brazil, Switzerland, Argentina, Bangladesh, Nigeria, Uruguay and the EU for new trade deals within 5 years.

- Australian PM Albanese is to sign a new security agreement with Fiji on Monday, while also finalising a deal to export uranium to India, The Australian reported.

NOTABLE HEADLINES

- US President Trump posted on Truth Social on Sunday that "There is nothing Americans can’t do except get Voter ID (Identification), Proof of Citizenship or, most importantly of all, TERMINATE THE FILIBUSTER (which the Democrats will do immediately upon gaining Office, and add 2 more States, 4 more Senators, 8 more Congressmen, at least 20 Electoral Votes, and it will be impossible for a Republican to ever be elected President again. I don’t want to be the last Republican President!). GET SMART REPUBLICANS, IF YOU DON’T, YOU WON’T BE IN OFFICE FOR LONG!"

- The Trump administration is releasing a regulatory plan to eliminate 702 existing administrative rules.

APAC TRADE

EQUITIES

- Asia-Pac stocks initially started the session with broad gains but reversed as the session continued, with a busy week ahead, which includes Samsung Electronics' Q2 earnings and SK Hynix's US listing.

- ASX 200 managed to limit its downside, and only posted modest losses, as upside in Energy and Health Care broadly offset the downside seen in Consumer Staples and Mining names. Further on the mining topic, Genesis Minerals made a AUD 5.6bln bid for Vault Minerals, hijacking a deal previously made with Regis Resources.

- Nikkei 225 was softer as it continued to pull back from its ATH of 72,832. Koixia was one of the big underperformers, after the Co. began shipping sample next-gen semiconductor products.

- KOSPI was under significant pressure, despite initially printing gains of as much as 2.9%, with Samsung set to report Q2 figures on Tuesday; operating profit expected to print at KRW 86tln. However, a miss would be detrimental to tech valuations, since doubts have crept in over the scale and durability of AI demand and capex.

- Shanghai Comp. traded either side of the unchanged mark while the Hang Seng posted decent gains. Alibaba found some comfort after a US federal judge ordered the Pentagon to give the Co. a reprieve from a lobbying ban tied to the Pentagon's curbs on Chinese companies.

- US equity futures began on the front foot, supported by tech amid stronger-than-expected Q2 revenue by Foxconn and initial upside in the KOSPI, but have since reversed lower.

- European equity futures are indicative of a flat/slightly softer open with the Euro Stoxx 50 futures -0.1% after cash closed +0.8% on Friday.

FX

- DXY was slightly firmer, trading near the top end of its range. This week's focus will be on the ISM Services PMI on Monday and the FOMC minutes on Wednesday.

- EUR/USD and GBP/USD traded in relatively contained ranges to start the week, with the EUR finding a base at 1.1428 after steadily stepping lower from a high of 1.1441 while GBP oscillated in a 1.3339-1.3356 range.

- USD/JPY trended higher since the open and resided near the top end of its range. As USD/JPY nears the 162.00 mark, focus will be on any further intervention by Japanese officials.

- Antipodeans were mixed, with the Kiwi underperforming the Aussie. Ahead of the RBNZ policy announcement on Wednesday, the New Zealand NZIER Shadow Board recommended that the RBNZ hold the OCR at 2.25%, which is against the market consensus of a 25bp hike to 2.50%. An 80% chance of a hike is priced in, so a hold would be seen as dovish and see a further unwinding of the hawkish bets.

- Goldman Sachs sees USD/JPY at 165.00 in a year's time, raising its forecast from 155.00, citing Japan's interest rate differentials with the US.

FIXED INCOME

- UST Futures traded with gains of a handful of ticks, holding near the top end of its 109-17 to 109-22 range as US traders get ready to re-enter the market from its extended holiday. US S&P Services and Composite PMI are expected to be unrevised; however, more focus will be on the ISM Services PMI, headline expected at 54.2 from the prior 54.5. Using the Manufacturing figure as a possible benchmark, the headline figure missed estimates while prices came down by 9 points. However, market reaction was fairly muted.

- Bund Futures rebounded after Friday’s low-volume selloff, moving higher right at the open. The earlier upside was seemingly helped by the lower energy prices and has held onto gains despite the reversal across the energy complex. As the European session approaches, pressure could be seen at the open after reports late in Friday’s session that the new net borrowing within the 2027 German draft budget was 7% higher than projected in April.

- JGB Futures were muted and rotated in a tight 127.05-127.28 range ahead of a large amount of supply this week: JPY 600bln of 30-year JGBs on Tuesday, JPY 2.5tln of 5-year JGBs on Thursday.

COMMODITIES

- Crude futures started the week on the back foot, helped by the lack of geopolitical updates over the weekend and the decision by OPEC+ to increase output by 188k bpd in August while flagging higher supply. WTI Aug’26 opened at USD 68.68/bbl and fell to a trough of USD 68.16/bbl, before remaining contained with a top of USD 69.16/bbl. In terms of weekend Middle Eastern newsflow, Iran's commercial attaché told IRNA that maritime trade between Iran and Qatar has resumed, while Qatar's Transport Ministry said that maritime activities would resume with immediate effect. In terms of hostilities, the UKMTO received a report of an incident 30 nautical miles southwest of Al Hudaydah, Yemen, of a cargo vessel under attack by unknown armed assailants.

- Precious Metals lacked any clear direction to start the week, and reversed the earlier gains. Spot gold oscillated in a USD 4170-4202/oz range, seemingly resilient despite a firmer dollar.

- 3M LME Copper traded at the upper end of its USD 13.38k-13.46k/t range, benefiting from the broadly positive tone, despite US equity futures pulling back from session highs.

- OPEC+ agreed to raise output targets by an additional 188k bpd, in line with the group's plan to reverse output curbs.

- A power outage has been reported at Marathon Petroleum's (MPC) Detroit refinery, causing controlled gas burning, according to local media.

- Hong Kong's pension fund will be able to invest in more gold ETFs as part of the government's push to the city into a gold trading hub, SCMP reported citing sources.

CRYPTO

- Bitcoin pulls back from the USD 64k handle after continuing to trade higher over the weekend.

NOTABLE ASIA-PAC HEADLINES

- China released draft amendments to its e-commerce law, changing platform responsibility rules by adding regulatory measures alongside existing penalties.

- South Korean President Lee said the administrative process must be sped up for chip clusters and power and water supply must be secured pre-emptively.

- New Zealand NZIER Shadow Board recommended that the RBNZ holds the OCR at 2.25%.

DATA RECAP

- Australian TD-MI Inflation Gauge MoM (Jun) M/M -0.4% (Prev. -0.3%); Y/Y 3.9% (Prev. 4.4%).

- Australian ANZ-Indeed Job Ads MoM (Jun) M/M -0.2% (Prev. 1.8%).

- Hong Kong S&P Global PMI (Jun) 52.0 (Prev. 50.4).

GEOPOLITICS

MIDDLE EAST

- Islamabad is the more likely option for the next round of US-Iran technical talks, with July 11th expected to be the date, sources told Pakistani newspaper Dawn, according to Fox. Negotiations are expected to focus on Iran's nuclear programme, frozen Iranian assets, the Strait of Hormuz and the Lebanon ceasefire.

- US President Trump spoke with Israeli PM Netanyahu on Friday, Axios reported, in which they agreed to meet in the US soon. This was later confirmed by the Israeli PM.

- Iran's ambassador to Beijing said China and other friendly countries will be granted special considerations, stating that there will be new arrangements concerning the Strait of Hormuz with the collaboration and cooperation of the state of Oman.

- Iran's commercial attaché told IRNA that maritime trade between Iran and Qatar has resumed. This followed an announcement by Qatar's Transport Ministry that maritime activities would resume with immediate effect.

- Israel is preparing to hand over 2 limited areas in southern Lebanon to the Lebanese army under a US-backed framework agreement, Israel's Ynet reported. Israeli PM Netanyahu held a small security cabinet meeting on Sunday evening while they waited for confirmation by the Lebanese army, the report added.

- Israeli Army Chief of Staff Zamir said that the Israeli army will continue its operations to eliminate threats from Lebanese soil.

- Israeli airstrikes hit multiple towns in southern Lebanon.

- UKMTO received a report of an incident 30NM southwest of Al Hudaydah, Yemen, of a cargo vessel under attack by unknown armed assailants.

- Ship-tracking data showed that at least 8 ships attempting to leave the Strait of Hormuz turned back, with the reasons unknown.

RUSSIA-UKRAINE

- Russia's Kremlin aide Ushakov said Russian President Putin and US President Trump spoke on the phone, in which Trump offered to help reach a settlement in Ukraine when he meets Ukrainian President Zelensky on Wednesday, while US envoys Witkoff and Kushner are to continue to help with peace efforts and are ready to come to Moscow.

- A Russian official said the Ukrainian attack cuts the electricity to Sevastopol in Crimea, AFP reported.

- Ukrainian President Zelensky posted on X that intelligence indicates that the Russians are preparing a new massive strike. Zelensky also called on partners to not delay any missiles for its Patriot air defences.

- There were multiple reports of several Russian ballistic missiles striking Ukraine's Kyiv with explosions being heard. This was later confirmed by the Kyiv mayor.

- Ukrainian forces struck an oil terminal in St. Petersburg with drones on Saturday, according to local officials.

- Ukraine said that it hit Russian airfields in Crimea, adding that around 7 jets were damaged. Additionally, Ukraine's commander of unmanned forces said it attacked 16 substations in Crimea as well as the Kherson, Luhansk and Zaporizhzhia.

- Ukrainian General Staff of the Armed Forces pushed back on claims that Russian forces have captured Kostyantynivka in Ukraine's Donetsk region.

OTHER

- China's National Defence Ministry said they will conduct a naval exercise in waters and airspace near Qingdao with Russia in July, followed by a joint maritime patrol in the Pacific Ocean.

EU/UK

NOTABLE HEADLINES

- ECB's Moulin said the ECB is in a good place, stating that the fall in oil prices puts the ECB in a better position on rates.

- ECB's Makhlouf said the ECB is determined to achieve 2% inflation.

- Andy Burnham announced that he will keep the triple lock, The Times' Swinford reported.

- Germany's AfD re-elected Alice Weidel as co-chair with 81% of the votes.