Published: 8 Jul 2026, 06:00 UTC

Newsquawk Desk

EU Market Open: Europe primed for lower open as energy rises on US revoking Iran oil waiver

0:00--:--

- Mixed APAC trade, China in the green amid multiple IPOs and tech strength locally. US and European futures contained.

- DXY is range-bound despite the renewed Middle East clashes. Yields consolidate after the energy-driven lift on Tuesday, following the revocation of the Iranian waiver and tit-for-tat strikes.

- US Treasury revoked the June 21st Iran-related waiver, General License X, which had allowed Iran to produce, deliver and sell its oil

- Brent remains above USD 76/bbl, firmer by c. 3.5%, driven higher by the above points. Though, interestingly, the US strikes did not spur any further upside.

- RBNZ hiked by 25bps in-line with consensus, assessed the current OCR remains accommodative, and further increases "appear likely".

- Looking ahead, highlights include Swedish Inflation Prelim. (Jun), US Atlanta Fed GDP (Q2), NBP Policy Announcement (Jul), NBH Minutes (Jun), Fed Minutes (Jun), NATO Ankara Summit, Speakers include US President Trump, Supply from the UK, Germany and the US.

- Click for the Newsquawk Week Ahead.

IRAN CONFLICT

- US CENTOM announced that it completed a new round of offensive strikes, hitting over 80 targets with precision munitions. CENTCOM added that forces remain postured and prepared to hold Iran accountable when the agreement is not adhered to or obeyed.

- Earlier, US CENTOM announced that forces have begun launching a series of powerful strikes in response to Iranian attacks on three commercial vessels transiting through the Strait of Hormuz. Iran's demonstrated aggression was unwarranted, dangerous and a clear violation of the ceasefire. Axios' Ravid reported that the strikes targeted Iranian air defence systems, coastal surveillance systems, surface air missiles, anti-ship cruise missile sites, drone launch sites and port facilities.

- There were reports of explosions throughout the south of Iran, including Sirik, Qeshm and Bandar Abbas. There were also reports of explosions on Kharg Island.

- In response, Iran's IRGC said they hit 85 important US military installations in Port Salman, Bahrain's 5th Maritime Zone and Kuwait's Ali Salem Air Base.

- A US official said the Iranian military launched drones at Bahrain, Axios' Ravid reported. This came following sirens and explosions in Bahrain.

- Iran fired several anti-ship missiles and drones towards US Navy warships in the Sea of Oman, Fars reported citing the Middle East Spectator.

- US President Trump approved the Iran strike plan and ordered it while in Turkey, a US official told Axios' Ravid. The official added that it is still unclear how long the strikes are going to continue.

- A US official said the strike on Iran was a punitive action, not a proportional response, and that the operation will not end in the short term, CNN reported.

- A US official said negotiators continue to work in good faith towards a final agreement but Iran's actions in the Strait were wholly unacceptable to the US and will be met with consequences.

- US Treasury revoked June 21st Iran-related waiver; Revokes General License X, effective July 7th, 2026, which previously authorized the production, delivery, and sale of Iranian-origin crude oil and petrochemical products from Iran.

- Iranian Parliament Speaker Ghalibaf said the US has violated major parts of the MoU, citing US attacks on southern Iran, reinstating oil sanctions and threats of further strikes as MoU violations. The US also violated Iranian adjustments in the Strait of Hormuz and continued Israeli aggression on Lebanon.

- Iran's top joint miliary command said Iran will give a crushing response to America's aggression and terrorist action, and under no circumstances will they allow them to interfere in the affairs of the Strait of Hormuz and its management. The US army targeted parts of southern Iran in blatant aggression. The force also reiterated that the only safe route for the passage and traffic of commercial ships and tankers is the route that Iran has determined.

- Iran's Foreign Ministry condemned the US Treasury's move to revoke the temporary suspension of sanctions on Iranian oil sales. The Ministry said that we will take any measure it deems necessary to safeguard its interests and national security and that Iran holds the US government responsible for the consequences of the breach of the Memorandum of Understanding.

- Iran's Foreign Ministry Spokesperson said Qatar's accusations against Iran regarding attack on a vessel linked to the Country in the Strait of Hormuz are perplexing and inconsistent with the principle of good neighbours, adding that Iran is diligently fulfilling its commitments under the MoU to take measures to manage the Strait of Hormuz and urged countries and shipping companies to refrain from any actions that contradict the MoU.

- US official said the US military also shot down multiple drones launched by Iran today and the attacks are a direct violation of the MoU.

- There were reports of widespread power outages in cities in Kuwait and Bahrain. Later, Bahrain Electricity and Water Authority said power has been fully restored after a limited outage in several areas.

- Israeli PM Netanyahu said he and US President Trump see "eye to eye" on the big things related to the handling of Tehran, despite the occasional disagreements.

- US War Secretary Hegseth is reportedly planning to make a visit to Israel on Wednesday, CNN reported citing sources.

- Israeli fighter jets carried out attacks in Barachit and Beit Yahoun in southern Lebanon.

US TRADE

EQUITIES

- US stocks were sold on Tuesday, with the Nasdaq the clear underperformer as Technology led the downside, particularly across semiconductor and memory names. The primary catalyst was Samsung's preliminary Q2 earnings, which disappointed lofty investor expectations and prompted a reassessment of valuations following the recent rally in the memory sector. Industrials also lagged, with sharp weakness in GE Vernova (GEV) weighing on the AI theme given its exposure to supplying power infrastructure for energy-intensive data centres. Energy was the clear outperforming sector as crude prices moved higher on renewed geopolitical tensions. Iran attacked commercial vessels from Qatar and Saudi Arabia in the Strait of Hormuz, before the US later responded by revoking Iran's General License X, which had allowed the country to produce, deliver and sell energy products.

- SPX -0.48% at 7,501, NDX -1.77% at 29,173, DJI -0.25% at 52,925, RUT -0.91% at 2,982.

TARIFFS/TRADE

- USTR Greer said Canada and Mexico have not lived up to everything.

CENTRAL BANKS

- The RBNZ hiked the OCR by 25bps to 2.50%, as expected, and stated that some further reduction in monetary stimulus is likely to be required to return inflation to the 2% target mid-point. The decision to hike was unanimous. The Committee assessed that the current level of the OCR remains accommodative but while further OCR increases appear likely at upcoming meetings, their timing is highly uncertain.

- RBNZ's Breman said in the post-policy press conference that we are gradually moving rates towards neutral, however the neutral rate is uncertain, with the neutral figure lying in a range of 2.5-3.5%. She reiterated that they felt it was needed to stress that uncertainty has increased on rate timing.RBA Assistant Governor Hunter said the Board will act as needed to ensure inflation returns to target and the labour market to sustainable full employment. There are few signs of a marked slowdown in activity.BoJ's Asada said a rate hike could slow the economy.

NOTABLE HEADLINES

- Microsoft (MSFT) replaces OpenAI and Anthropic with it's own AI in some apps.

- Atlanta Fed GDPnow Model (Q2): 1.4% (prev. 1.2%).

APAC TRADE

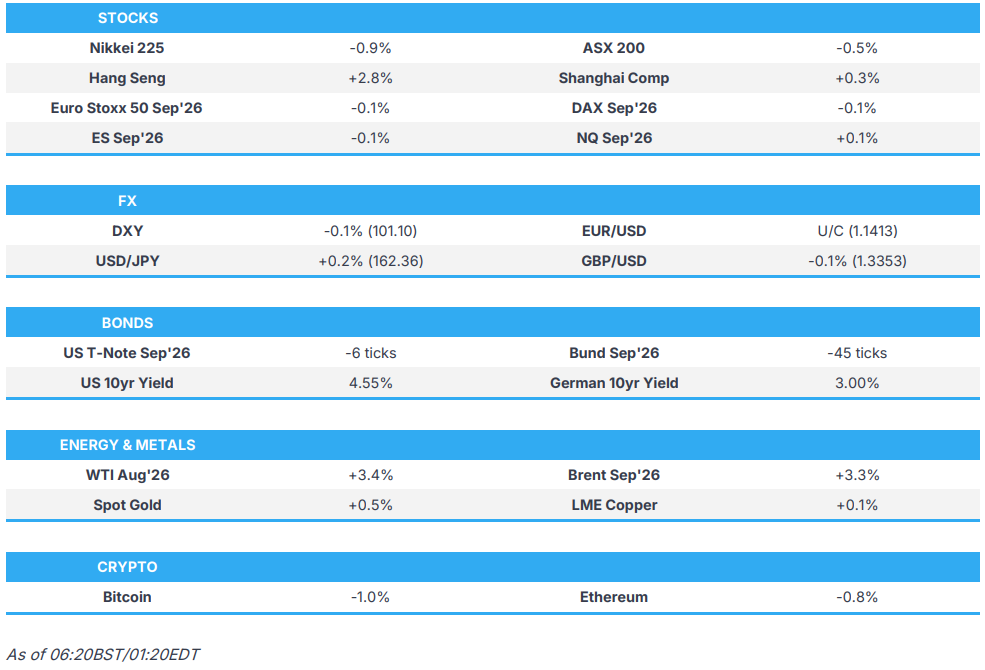

EQUITIES

- Asia-Pac stocks traded mixed, with Chinese indices the only region in the green amid multiple IPOs and strength in China's tech space. Sentiment from the US session carried over in the Asia-Pac session, as energy prices surged amid the re-escalation of US-Iran tensions.

- ASX 200 continued to be weighed on by metals, with the Metals & Mining sector the worst performer, with Materials followed. Energy topped the sector pile

- Nikkei 225 started on the softer side, briefly returned to the unchanged mark before returning to the downside.

- KOSPI traded choppy, as the initial weakness briefly reversed to print modest gains. However, weakness returned as the session continued, resulting in the Korea Exchange activating the sidecar on the KOSPI and KOSDAQ. As a result, the KOSPI extended its losses from June peak to 20%, indicating a bear market.

- Shanghai Comp. and Hang Seng. were the only indices printing gains, with outperformance in the Hang Seng following strength in tech names. The strength can be attributed to two reports: 1) From Reuters, DeepSeek developing its own chip to power AI systems, and 2) from the Information, Zhiphu considering designing its own AI chip.

- US equity futures started futures trade on the backfoot but pared slightly and currently trades flat.

- European equity futures are indicative of a muted open with the Euro Stoxx 50 future U/C after cash closed -1.2% on Tuesday.

FX

- DXY traded in a narrow 101.07-101.22 range despite the renewed aggression between the US and Iran, primarily as a result of IRGC strikes on 3 commercial ships in the Strait of Hormuz. Looking ahead, focus will be on the FOMC minutes from the June meeting.

- EUR and GBP rotated in tight ranges, with EUR/USD briefly slipping below the 1.1400 handle while GBP/USD traded either side of the 1.3350 mark. Not much on the docket in either region. ECB minutes are expected on Thursday, while final German and French inflation figures are to be released on Friday.

- USD/JPY regained the 162.00 handle during Tuesday’s session and has continued to extend higher on Wednesday, topping at 162.46. An interesting report by Asahi and Nikkei, stating that the Japanese government may tweak a reference to monetary policy in its annual policy agenda to avoid the appearance that it is putting pressure on the BoJ.

- NZD/USD was the G10 outperformer, after the RBNZ hiked rates by 25bps, unanimously, and signalled further hikes to bring inflation to the 2% target mid-point.

FIXED INCOME

- UST Futures oscillated in a narrow 109-02+ to 109-06+ range, as energy prices consolidated after crude futures surged over 5% in Tuesday’s trade following the revocation of Iran’s oil waiver and US threats, which then resulted in tit-for-tat strikes between the US and Iran.

- Bund Futures, in tandem with USTs, traded in a tight 17-tick range. This comes ahead of a 10-year Bund auction, in which Germany is to sell EUR 6bln 3.00% 2036 Bunds. With the recent rise in yields, this could bring in extra demand for German debt, as seen with the US 3yr auction on Tuesday.

- JGB Futures also traded on a slightly softer footing but in narrow ranges. Japanese yields have reached highs not seen since the 1990s, with a slight inversion at the long-end of the curve.

- US sells USD 58bln of 3-year notes; stop-through 0.6bps.

- Australia sells AUD 900mln 4.25% 2036 AGBs: b/c 4.55x (prev. 3.86x), average yield 4.8745% (prev. 4.9735%).

COMMODITIES

- Crude futures held onto its post-settlement gains, as Brent traded either side of USD 76/bbl. Post-settlement, the US Treasury revoked Iran’s rights to sell its oil, while a US official stated that Iran’s actions in the Strait will be met with consequences. This lifted the energy complex higher and later, US CENTCOM announced that forces began launching strikes, with explosions heard in Sirik, Qeshm and Bandar Abbas, targeting Iranian weapon launch sites, air defences and more. However, this did not result in any further upside in crude futures as participants telegraphed the US response. Iran released a statement, saying it will take any measure to safeguard its interests and national security, with Iran's IRGC claiming to have hit 85 US military installations in Kuwait and Bahrain.

- Precious Metals traded rangebound, with spot gold finding support at the USD 4100/oz handle, despite the renewed US-Iran strikes. Analysts think the yellow metal could test below USD 4k/oz. However, supporting the metal is continued central bank buying, with the PBoC having bought 480k troy ounces of gold in June, its biggest purchase since October 2023.

- 3M LME Copper opened lower, below the USD 13.3k/t mark, but reversed just shy of the unchanged mark amid positiveness in Chinese markets.

- US Private Inventory Data (bbls): Crude -0.399mln (exp. -1.5mln), Distillates -1.801mln (exp. +1mln), Gasoline -2.929mln (exp. -1.55mln), Cushing -0.069mln.

- EIA STEO: 2026 World Oil Demand at 102.8mln BPD (prev. 102.9mln BPD); 2027 World Oil Demand at 104.8mln BPD (prev. 105.3mln BPD).

- Discounts for Russian Urals crude raise to USD 10/bbl vs. Brent in India amid weaker demand.

- Japan aluminium premiums for Jul-Sep shipment set at USD 395/t, +12-13% Q/Q.

CRYPTO

- Bitcoin extended lower, back below USD 63k, amid the lack of desire to hold risky assets

NOTABLE ASIA-PAC HEADLINES

- Japan is considering a change to monetary policy wording in the Honebuto, Asahi reported.

DATA RECAP

- Japanese Bank Lending YoY (Jun) Y/Y 5.7% vs. Exp. 5.8% (Prev. 5.7%).

- Japanese Current Account (May) 3.968B vs. Exp. 4121B (Prev. 3907B).

- Australian Building Permits YoY Final (May) Y/Y 5.3% vs. Exp. 5.3% (Prev. 10.2%).

- Australian Building Permits MoM Final (May) M/M -1.1% vs. Exp. -1.1% (Prev. -3.4%).

GEOPOLITICS

RUSSIA-UKRAINE

- Russian officials have stated that military operations in Ukraine will cease the day after the withdrawal of the Armed Forces of Ukraine from Russian territory, RIA reported.

- Explosions heard in Ukraine's Kyiv, AFP reported, which was later confirmed by the Ukrainian Armed Forces.

OTHER

- US President Trump is expected to remove Syrian Terrorism Designation, Semafor reported.

EU/UK

NOTABLE HEADLINES

- The UK Conservative Party and Labour Party have both announced that they will not stand a candidate in the Clacton by-election.