Published: 9 Jul 2026, 06:20 UTC

Newsquawk Desk

EU Market Open: Europe primed for firm open as energy looks past US-Iran strikes

0:00--:--

- US struck around 90 Iranian military targets. In return, the IRGC said it attacked two US bases in Bahrain and two in Kuwait.

- CNN reports that US President Trump is losing patience with the pace of negotiations, particularly on nuclear.

- Energy benchmarks modestly bid, but in relatively narrow ranges; downside seen in the early European morning as Trump reiterates that Iran wants to make a deal.

- APAC trade was initially resilient to the above, before then reversing as the night progressed.

- FOMC Minutes outlined that a few saw a case for raising rates, several did not see the stance as restrictive, a few as slightly restrictive.

- NZD continues to lead the FX space, USD is under modest pressure. Fixed rangebound, taking direction from energy.

- Looking ahead, highlights include German Trade Balance (May), US Initial Jobless Claims (Jul/04), Existing Home Sales (Jun), ECB Minutes (Jun), Banxico Minutes (Jun), Speakers include Fed's Williams, Logan, BoE's Breeden, Supply from the US and Earnings from PepsiCo.

- Click for the Newsquawk Week Ahead.

IRAN CONFLICT

- US President Trump said Iran was just hit very hard and we have many ways to win. He added that he do not know if Iran will honour a deal but Iran wants to make a deal badly.

- US President Trump posted "This is in retribution for yesterday’s bombing of ships by Iran. If it happens again, it will get much worse!"

- US CENTCOM announced the completion of its most recent round of strikes against Iran, in which forces struck around 90 Iranian military targets. There were reports of fresh explosions in Bandar Abbas, Sirik and Hormozgan. There have also been reports of explosions in Abu Musa Island and Bushehr. Nour news reported that the attack on Bushehr did not cause any damage to the nuclear power plant.

- A US official later said that the US air force bombed two railway bridges in Iran, Axios' Ravid reported. In response, Iran's IRGC said they would respond to the targeting of a bridge in Aqqala.

- An Iranian source said the armed forces will begin a widespread attack on US army bases in the region shortly, Nour News reported. Sirens and explosions were reported in Kuwait and Bahrain with reports of Iranian missiles targeting the Azraq base in eastern Jordan. The IRGC later announced that two US bases in Kuwait and two base in Bahrain were attacked and threatened that response will be extended to other US bases in the region if the US repeats its attacks.

- US VP Vance, on Iran, said if they shoot our ships, or try to close strait of Hormuz, we will respond.

- The length and severity of the new campaign depends entirely on Tehran's next moves, Axios reported citing a US official. The White House is preparing for a multi-day or multi-week exchange of fire with Iran over the Strait of Hormuz.

- US President Trump's frustration with Iran was due in part to his anger over the Strait not being fully open yet and that Iran hit ships transiting the Strait, CNN reported citing a US official. The official added that Trump is losing patience with the pace of negotiations, specifically Iran's appearing to slow walk Washington on the nuclear talks.

- A US official said the ceasefire with Iran has been halted, at least temporarily, CNN reported.

- Iranian Parliament Speaker Ghalibaf said America has not yet learned that bullying and breach of promise are no longer free. He added the Strait of Hormuz will only open with Iranian arrangements, not American threats.

- US CENTCOM said more than 20 US Navy warships are patrolling waters across the Middle East as CENTCOM forces continue promoting regional security and stability.

- Some war insurers advise shipowners to pause Hormuz voyages after attacks, according to Reuters citing sources.

- Lebanon demanded Israel's withdrawal from two "pilot zones" in the south before participating in the next round of direct negotiations in Rome next week, a diplomatic source familiar with the talks told AFP.

- Iraq has agreed to new controls aimed at preventing US dollars from flowing to Iran and its militia allies in exchange for the Trump administration lifting a four-month suspension in shipments of American currency to Baghdad, WSJ reported citing sources.

US TRADE

EQUITIES

- US stocks ultimately closed mixed on Wednesday, with the Nasdaq in the green while the S&P 500 finished marginally lower. The Dow and Russell 2000 were the clear laggards. Sector performance was predominantly weaker, although Technology and Energy closed in positive territory, while Materials underperformed amid broad weakness in metal prices. The primary driver throughout the session was the renewed escalation in Middle East tensions. Overnight, the US struck targets in southern Iran, prompting Tehran to retaliate with attacks on US military sites in the Gulf. Later in the day, President Trump said he believed the ceasefire was over, further lifting geopolitical risk sentiment. Also, in late trade, explosions were heard across southern Iran.

- SPX -0.28% at 7,483, NDX +0.27% at 29,253, DJI -1.09% at 52,353, RUT -0.88% at 2,956

TARIFFS/TRADE

- US President Trump said we will give companies up to two years to build in the US; if not, they must pay up to 250% tariff.

- US President Trump said a lot of good trade deals were made with Turkey and that Spain was very generous today as they honoured a request for lots of payment.

- A US official said that the US Treasury will work with USTR and the Commerce Department to present President Trump with a menu of Spanish products that may be subject to a trade embargo in the coming days.

CENTRAL BANKS

- FOMC MINUTES: Participants generally saw upside risks to price stability as elevated, while downside risks to maximum employment goal had moderated a bit. A few participants commented that, in light of these developments, there was a case for raising the target range for the federal funds rate. On policy, several participants remarked that they did not see the current policy stance as restrictive, while a few other participants commented that they saw the current policy stance as slightly restrictive. Most participants, however, also pointed to scenarios in which, in the context of stable labour market conditions, inflation would remain elevated due to strong AI-related demand, the conflict in the Middle East, or the effects of tariffs. In such scenarios, almost all of these participants indicated that some policy firming would likely be warranted to return inflation to 2%.

- SNB Chairman said we are at 0% rates and the bar to go negative is high, but we would do it if necessary. Schlegel also said they are ready to intervene in the FX market if needed.

NOTABLE HEADLINES

- US President Trump said he will be asking for a rehearing by the Supreme Court on birthright citizenship.

- The US Senate committee will reportedly vote next week on a bill to toughen the US government ban on Chinese automakers from entering the US market.

- Atlanta Fed GDPNow (Q2 26): 1.3% (prev. 1.4%).

APAC TRADE

EQUITIES

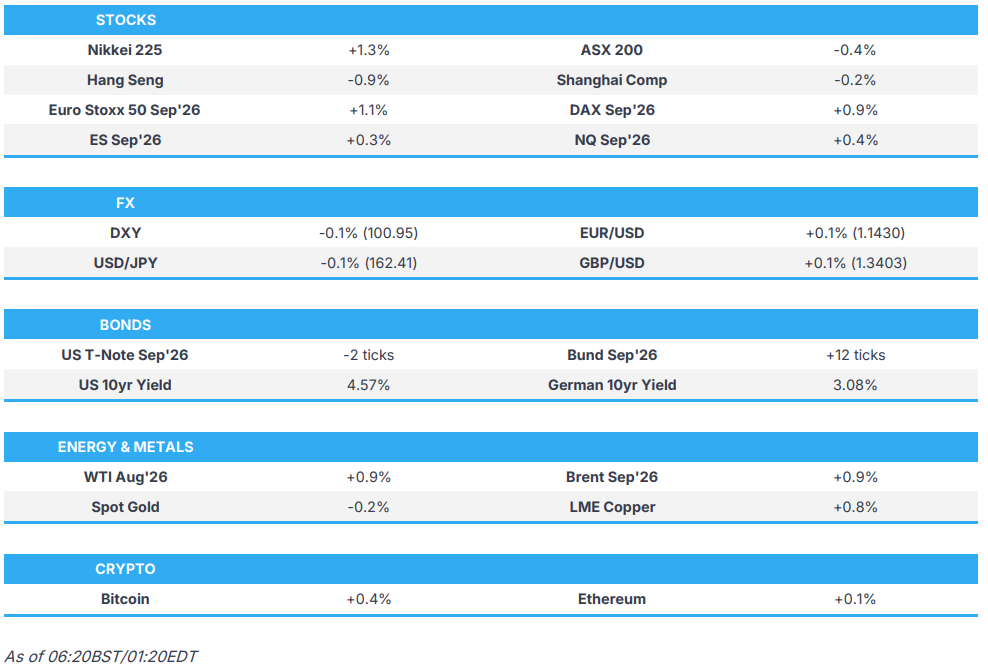

- Asia-Pac stocks initially proved resilient to the recent US-Iran strikes, with the majority of indices opening with decent gains. However, as the session progressed, market reversed, with the Nikkei 225 the only index printed gains. The reversal came without a clear driver, which highlights the extreme volatility in equity markets.

- ASX 200 began trade with losses and continued to trade in the red, however stabilised above 8,700. Energy was the sector outperformer, while Metals & Mining lagged for a fourth straight session.

- Nikkei 225 was the only index printing gains, helped by gains in Kioxia, after Bain Capital announced the sale of its entire stake, and Tokyo Election, as it highlighted the ability to cut chip gear delivery times by 50%.

- KOSPI initially surged at the open, following on from the tech-led gains stateside, with Samsung and SK Hynix printing gains of over 5% at one point. However, the index reversed, driven by the losses in the two tech giants, highlighting the extreme volatility in the South Korean benchmark. The KOSPI volatility index currently stands at 87.41, compared to Nasdaq’s 27.86.

- Shanghai Comp. and Hang Seng. opened with modest gains but gave back slightly. It was another day of IPOs for the Hang Seng, with the introduction of Luxshare Precision Industry, which didn't start as hoped.

- US equity futures traded with modest gains across the board.

- European equity futures are indicative of a firmer open with the Euro Stoxx 50 future +1.0% after cash closed -1.8% on Wednesday.

FX

- DXY continued to trade on the softer side, trading at the lower end of its 100.94-101.04 range. Price action on Wednesday was puzzling, with the index closing lower despite the higher energy prices. With the most recent CFTC figures showing aggregate dollar long increasing to its highest amount in over a decade, further upside in the USD may be limited.

- EUR and GBP traded rangebound in their respective 1.1417-1.1430 and 1.3386-1.3404 range. A light docket ahead for both regions, with the EUR just awaiting June’s ECB minutes.

- USD/JPY slipped below the 162.50 handle and found resistance at the key level. JPY on the weakest currency on a weekly timeframe, and without any intervention by the MoF or hikes by the BoJ, further weakness looks set to continue.

- Antipodeans traded mixed, with the Kiwi the clear G10 outperformer as gains continued following the RBNZ rate hike on Wednesday.

- CNH was slightly firmer against the dollar, despite a broadly cooler inflation print. Headline inflation Y/Y printed at 1.0% (exp. 1.1%, prev. 1.2%). However, as expected, PPI continued to accelerate as it rose to 4.1% from 3.9%

FIXED INCOME

- Global fixed income benchmarks traded rangebound, helped by the lack of movement in energy prices. Government debt continues to be hit when energy benchmarks take a leg higher, as worries of pass-through into inflation alter the central bank’s policy reaction.

- UST Futures oscillated in a narrow 128-27 to 108-31 band, with the 10yr yield topping just shy of the 4.60% mark in Wednesday’s session. The 10-year bond auction brought in strong demand, similar to the 3-year auction on Tuesday; however, this was dismissed as geopolitics remained front and centre. Ahead is a 30-year auction, which may bring strong demand as the 30yr yield returns back above 5.00%.

- Bund Futures, similarly, traded in a tight 13-tick range. Contrary to the US auction, the 10-year Bund auction was poor. Debt fell following the auction, however bunds were already lower by c. 80 ticks pre-auction. The ECB minutes for the June meeting is on the docket later, with focus on how the committee viewed the July vs September argument at the time.

- JGB Futures rotated in a 126.31-126.65 range. Moody’s came out with some positive commentary for Japan, reiterating its stable view despite the prospect of trillions of dollars of government spending. The 5-year auction brought in strong demand, with the b/c higher than the 12-month average; however, debt did trade lower following the auction.

- US sells USD 39bln of 10-year notes; Stop through 0.6bps.

- Japan sells JPY 2.5tln 5-year JGBs; b/c 3.43x (prev. 3.11x), average yield 2.020% (prev. 1.905%).

COMMODITIES

- Crude futures were fairly unreactive at the start of Thursday’s trade, despite the tit-for-tat strikes between the US and Iran. Following US President Trump’s threat of strikes at the NATO summit, US CENTCOM announced a fresh wave of attacks against military targets, with multiple areas in southern Iran hit. Bushehr, home of Iran’s nuclear plant, was targeted; no damage to the plant was reported. In retaliation, Iran struck US bases across the Gulf, including Kuwait, Bahrain and Jordan. Iranian officials maintain their stance on the Strait of Hormuz, with Iranian Parliament Speaker Ghalibaf stating it will only open with an Iranian arrangement, not with American threats. WTI and Brent rotated in their respective USD 73.88-75.13/bbl and USD 78.39-79.21/bbl range.

- Precious Metals traded in narrow ranges, but held onto Wednesday’s late bid higher, supported by the softer dollar. Spot gold traded in a USD 4054-4090/oz range. Taking a hint from ETF inflows, the yellow metal is seemingly finding value around USD 4k/oz, with around USD 8bln of net inflows in H1'26.

- 3M LME Copper was firmer, returning above the USD 13.2k/t handle, following the initial positive sentiment in Asia-Pac equities.

- Citi expects Brent to average USD 70/bbl in Q4'26 and USD 65/bbl in 2027, conditional on a US-Iran agreement and the reopening of Hormuz

CRYPTO

- Bitcoin found support at the 20-SMA and rotated in a USD 61.64k-62.6k range.

DATA RECAP

- Chinese Inflation Rate YoY (Jun) Y/Y 1.0% vs. Exp. 1.2% (Prev. 1.2%, Low. 0.8%, High. 1.5%).

- Chinese Inflation Rate MoM (Jun) M/M -0.3% vs. Exp. -0.2% (Prev. -0.1%, Low. -0.6%, High. 0%).

- Chinese PPI YoY (Jun) Y/Y 4.1% vs. Exp. 4.1% (Prev. 3.9%, Low. 2.6%, High. 4.5%).

GEOPOLITICS

RUSSIA-UKRAINE

- The Stavropol governor said a fire at the industrial site in Stavropol has intensified, reaching fuel tanks. This came following earlier comments stating that a UAV raid caused a fire at an industrial facility in Stavropol.

EU/UK

NOTABLE HEADLINES

- Andy Burnham has pledged to rebuild the country's hard power by ensuring that billions of pounds of additional defence spending is focused on the UK rather than given to American or European companies, according to the Times' Swinford.

- Andy Burnham is reportedly discussing plans to give the next deputy PM control of his new Downing Street outpost in Manchester, the FT reports citing sources

- UK RICS House Price Balance (Jun) -33% vs. Exp. -32% (Prev. -35%, Revised to -34%). "Until there is greater clarity over both the political backdrop and the path of interest rates, housing market activity is likely to remain relatively subdued in the near term."