Published: 16 Jul 2026, 10:30 UTC

Newsquawk Desk

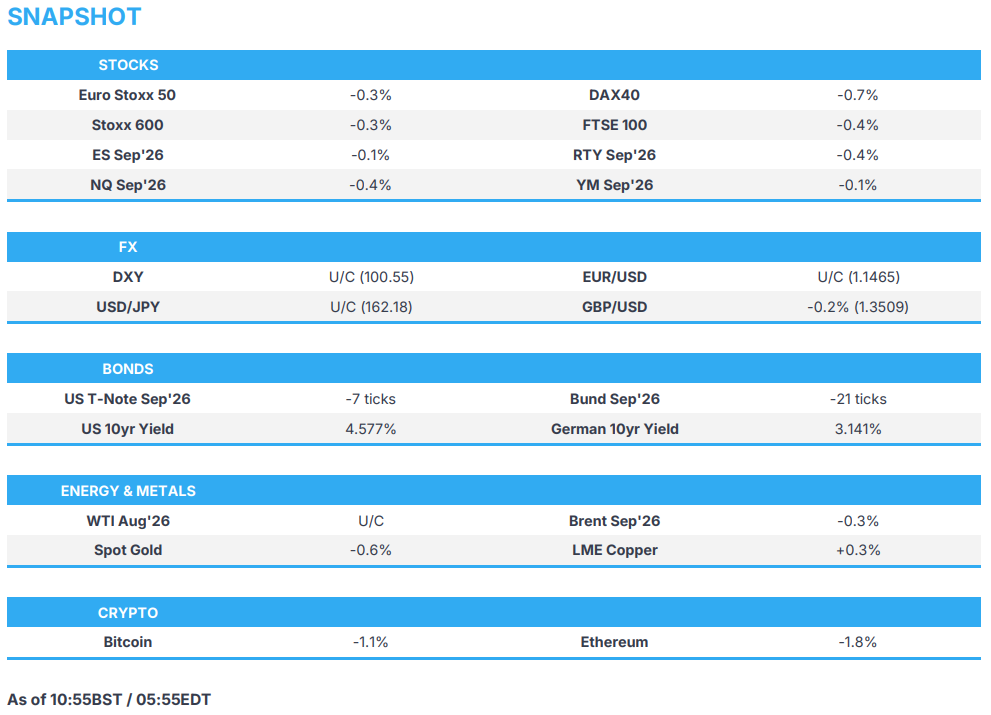

US Market Open: Equity futures lower despite TSMC beat and raise and large NVIDIA Rubin order from Japan

0:00--:--

- The US has completed another round of strikes on various parts of Iran, targeting military capabilities; Tehran responded with its own attacks on Kuwait and Jordan.

- TSMC reported Q2 metrics that beat estimates, while raising its Q3 revenue guidance above expectations. In addition, the co. is to add another USD 100bln of US investment.

- US equity futures lower despite strong TSMC earnings and Japan's large investment for Nvidia's Rubin chips.

- DXY rangebound while CHF and NOK outperforms; GBP unreactive following GDP data.

- Fixed income benchmarks softer despite lower energy; UK and French politics in focus.

- Crude benchmarks take a breather despite ongoing US-Iran strikes, spot gold moves a bit lower.

- Looking ahead, highlights include US Retail Sales (Jun), Jobless Claims, Philly Fed Index (Jul), Pending Home Sales (Jun), Atlanta Fed GDP, Speakers including Fed’s Logan & Schmid, Earnings from Netflix, Alcoa, GE Aerospace, US Bancorp, Abbott & State Street.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.3%) begin Thursday’s trade entirely in the red, with underperformance in the SMI (-0.9%) after earnings from Partners Group and ABB. On the data front, UK GDP M/M printed 0.1% M/M, in line with expectations, while the 3M ticked down to 0.7%, from 0.8%, but beat the 0.5% consensus; no reaction seen in the FTSE 100.

- Sectors highlight the negative bias, with Media (+0.6%) the only sector printing modest gains after earnings from Publicis (+2.1%), raising its FY revenue guidance. Underperformance is seen in Utilities (-1.1%), followed by Industrial Goods & Services (-1.0%) and Financial Services (-1.1%).

- US equity futures follow their European peers, trading entirely in the red, despite strong TSMC earnings and an Nvidia announcement. For TSMC, the Co. reported Q2 metrics that beat estimates and raised its Q3 revenue guidance. Additionally, the Co. is to add another USD 100bln of US investment. For Nvidia, the Co. announced that Japan, through Noetra, will buy 27,500 Rubin chips to build AI models for robots.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s lack direction against the Buck in light newsflow. GBP, CHF and NOK all lower after recent gains.

- DXY is marginally firmer, but USD gains are mixed against other G10 peers. Today’s calendar sees a few Fed speakers, Logan, Schmid and Jefferson, and the data slate features Retail Sales and weekly jobless claims.

- NOK and CHF are the worst performers against the Greenback, which attempts to retrace lost ground with energy prices weighing on NOK, and USD/CHF garnering support around 0.8050.

- Not too much was learned from the UK GDP reading for May, which rose but fell short of expectations. On Wednesday, GBP rallied after a number of outlets reported that Mahmood was set for the Chancellor role. Currently, GBP/USD is holding onto gains just above the 1.35 mark.

- EUR is flat against the USD and slightly firmer against GBP, with bloc-specific newsflow light. For now, EUR trades within a narrow 1.1460-74 range. EZ calendar light with ECB on its quiet period ahead of its policy meeting next week.

FIXED INCOME

- Global fixed income benchmarks are modestly softer across the board, with a lack of clear drivers, and as US-Iran strikes continue to stoke fears of prolonged inflation.

- Gilts (-15 ticks) trade at the lower end of its 87.15-87.60 range, giving back some of Wednesday’s gains. This morning, UK GDP printed 0.1% M/M, in line with expectations, while the three-month gauge ticked down to 0.7% (from 0.8%), but still beat the 0.5% consensus. Politics remain front and centre: reports on Wednesday suggest that incoming PM Andy Burnham is likely to appoint Home Secretary Mahmood as the next Chancellor. Markets have taken this as a positive as she is seen as fiscally conservative, though many still seek clarity on her broader positions. Polymarket gives Mahmood a 63% chance vs Miliband's 9% to become the next Chancellor. The UK had a decent auction, however demand did fall from the prior auction

- OATs (-22 ticks) follow their European peers lower. Politics remains in focus; recently, RN's Le Pen was found guilty of embezzlement by the Paris court, but given the timing of the first round of the Presidential Election, she is eligible to run for President. Since then, she announced she would appeal the court's decision and has launched her Presidential campaign. Polls show that Le Pen has extended her lead, with support rising to above 35% from 33% before she announced her bid. Today’s auctions came broadly in line with priors, with demand holding near 3x.

- USTs (-7 ticks) look ahead for more Fedspeak, with Logan, Schmid and Jefferson all set to speak on the economy and economic outlook today (note: Jefferson is after hours). On the data front, initial jobless claims and retail sales are the highlights.

- The UK sells GBP 4.25bln 4.875% 2036 Treasury Gilt: b/c 3.13x (prev. 3.46x), average yield 5.040% (prev. 4.858%), tail 0.1bps (prev. 0.1bps).

- France sells EUR 13.999bln vs exp. EUR 12-14bln 2.40% 2029, 1.50% 2031, 3.25% 2032 and 3.50% 2033 OAT.

- Spain sells EUR 5.974bln vs exp. EUR 5-6bln 2.35% 2029, 3.55% 2033 and 3.95% 2056 Bono.

COMMODITIES

- The situation between the US and Iran remains volatile. Overnight, the US completed another round of strikes on various parts of Iran, targeting military capabilities. Tehran responded with its own attacks on Kuwait and Jordan.

- The path to peace currently remains uncertain. President Trump said that strikes would expand next week; a recent report via the WSJ suggested that Trump is leaning toward expanding US military operations in Iran after days of briefings from top aides. If this proves to be the case, then the risk is that Iran responds with a harsher response against its regional peers. Thus far, Iran has generally avoided energy infrastructure across Gulf nations, but a US expansion could see Iran begin to target Gulf energy facilities, posing risks for oil supply. In the immediate term, the Strait remains shut and near-term flows have been slowed; longer-term, severe facility damage could see halts to production for several months/years, analysts say.

- Despite these risks, crude benchmarks are trading lower this morning; Brent Sep’26 (-0.5%) trades within a USD 84.30-85.55/bbl range. Price action was lacklustre overnight and into the European morning. However, some modest upticks (c. USD 0.30/bbl) were seen after an Iranian Top Military Commander stated that the Strait of Hormuz is a red line and added that all infrastructure in the region will be "crushed" if the US continues its interference.

- Spot gold (-0.6%) moved lower throughout the APAC session. The subdued action filtered through into London hours; currently holding at session lows of USD 4,024/oz (vs peak of USD 4,064/oz). Action, which is a bit of a paring back from the gains seen in the past couple of sessions. Elsewhere, base metals hold a modest positive bias. 3M LME Copper (+0.3%) holds within a USD 13,541-13,648/t range.

- Crude oil flows were suspended at all Iraqi oil loading terminals following a drone crash into an oil tanker at Iraq’s Basra terminal; no damage or fires were reported, security sources said.

TRADE/TARIFFS

- The US is to set a 25% tariff on some Brazil goods from July 22nd, with coffee and beef exempted.

- USTR Greer said that Canada offers no concessions and that Mexico is pragmatic in USMCA talks.

NOTABLE EUROPEAN HEADLINES

- Italy PM Meloni’s electoral reform has been approved by Italy’s lower house in a vote.

NOTABLE EUROPEAN DATA RECAP

- UK GDP YoY (May) Y/Y 1.3% vs. Exp. 1.4% (Prev. 1.2%).

- UK GDP 3-Month Avg (May) 0.7% vs. Exp. 0.5% (Prev. 0.7%, Low. 0.4%, High. 0.6%).

- UK GDP MoM (May) M/M 0.1% vs. Exp. 0.1% (Prev. -0.1%, Low. -0.3%, High. 0.1%).

- UK Goods Trade Balance (May) -18.66B vs. Exp. -23.6B (Prev. -26.05B).

- UK Manufacturing Production MoM (May) M/M 0.1% vs. Exp. -0.1% (Prev. 0.4%, Low. -0.5%, High. 0.3%).

- UK Manufacturing Production YoY (May) Y/Y 2.3% vs. Exp. 1.9% (Prev. 1%, Low. 1.7%, High. 2.6%).

- UK Industrial Production MoM (May) M/M -0.5% vs. Exp. 0.1% (Prev. 0%, Low. 0.5%, High. 1.4%).

- UK Industrial Production YoY (May) Y/Y 1.0% vs. Exp. 1.2% (Prev. -0.2%, Low. 0.5%, High. 1.4%).

- Italian Inflation Rate MoM Final (Jun) M/M 0% vs. Exp. 0.0% (Prev. 0.4%).

- Italian Inflation Rate YoY Final (Jun) Y/Y 3.0% vs. Exp. 3% (Prev. 3.2%).

CENTRAL BANKS

- BoK raised its 7-day Repo Rate by 25bps to 2.75%, as expected. BoK said the rate decision was unanimous and growth rate this year is expected to considerably surpass the May forecast of 2.6%. Will assess timing of further increase in inflation pressure, improvement trend in the economy and financial stability.

- BoE's Breeden said it is important firms are stress testing AI valuations. The Iran war shock is less likely to become embedded and lead to inflationary dynamics that members might need to lean against.

- NBP's Zarzecki said the base case is for rates to remain unchanged until the turn of 2026/27, with rates likely to rise in 2027.

- SNB Minutes (Jun): Although inflation risks have increased in recent months and stronger second-round effects are possible, there is no immediate need for action.

NOTABLE US HEADLINES

- BofA week-to-July 11th total card spending +4.5% (prev. 4.8%); spending growth slowed but remains solid.

GEOPOLITICS

MIDDLE EAST

- US President Trump posted that Iran allowed a US citizen who was wrongly detained in December 2024 to leave the country. Trump added that the citizen is now safely outside of Iran and in good condition, while he stated that the US appreciates the gesture of goodwill by Iran.

- US VP Vance said Israel is more effective than most at influencing the US, and that some people in the Israeli government want war indefinitely. Furthermore, Vance said they are not going to send ground troops for regime change and that the US will not simply engage in endless bombing of Iran.

- US CENTCOM said forces conducted operations for a second wave of strikes on Wednesday against Iran and that US forces disabled a non-compliant vessel in the Arabian Gulf, while it denied Iranian claims that US forces struck a civilian wheat storage facility in Hoveyzeh on July 14th and described the reports as false.

- Explosions were heard in Iran's Khorramabad, and US air strikes targeted areas in Tehran. Explosions were also heard in Iran's Qeshm and Bandar Abbas, while US projectiles hit near Sirik.

- Iran attacked economic interests and US facilities in Kuwait, while at least 10 explosions were heard at the US Navy's Fifth Fleet Headquarters in Bahrain, and Iran also targeted Jordan.

- Kuwait said its armed forces intercepted four cruise missiles and 21 drones from Iran on Wednesday, while Iranian aggression targeted a number of vital facilities, resulting in material damage, although no injuries were reported.

- Iran's Top Joint Military Command said the Strait of Hormuz is a red line and added that all infrastructure in the region will be "crushed" if the US continues its interference.

- Houthis were reportedly laying the groundwork and quietly extending their reach to the Horn of Africa, according to the Telegraph citing sources in Yemen, with Houthi rebels reportedly preparing to shut the Bab el-Mandeb Strait on behalf of Iran. Furthermore, sources said the effort was a deliberate Iranian attempt to control "the other side of the Red Sea" and create a situation similar to its grip on the Strait of Hormuz.

- Israeli Defence Minister said US operations against Iran was discussed in the phone call with the US Secretary of State Rubio, and said Israel will remain in security zones in Syria, Gaza and Lebanon.

RUSSIA-UKRAINE

- Ukraine's security service said it struck two Russian shadow fleet tankers in the Black sea and hit six more tankers and two tug boats in the Sea of Azov and Black sea.

OTHER

- US and Iraq to announce USD 60bln in commercial deals as Trump pivots US-Iraq ties towards commerce over military, according to Semafor.

CRYPTO

- Bitcoin fell just shy of the USD 64k handle while Ethereum holds above USD 1880.

APAC TRADE

- APAC stocks were ultimately mixed, albeit with a mostly negative bias in the major indices, as risk sentiment was dampened by a sell-off in semiconductor stocks.

- ASX 200 was subdued with the index pressured by losses in miners after BHP reported lower output.

- Nikkei 225 slid below 67,000 with chip-related stocks over-represented in the list of worst performers.

- KOSPI triggered sidecars as Samsung Electronics and SK Hynix slumped alongside the semiconductor sell-off, while the BoK also raised its key rate by 25bps to 2.75%, as expected, and signalled further action.

- Hang Seng and Shanghai Comp were mixed with the mainland in the red following disappointing loans and financing data, while the Hong Kong benchmark rallied amid strength in hyperscalers following reports that US companies were increasingly adopting open-weight Chinese AI models and that Alibaba's Qwen AI would be integrated into Apple Intelligence in China.

NOTABLE ASIA-PAC HEADLINES

- South Korea Financial Regulator said they are to revise rules on single-stock leveraged ETFs to temporarily halt new single leveraged products from listing. The minimum required investor deposit is to be raised to KRW 30mln from KRW 10mln.

- Japanese Finance Minister Katayama reiterated they will take appropriate action on FX anytime as needed, although she won't comment on specific FX levels, and stated they will monitor market developments and economic indicators to achieve fiscal sustainability.