Published: 17 Jul 2026, 10:44 UTC

Newsquawk Desk

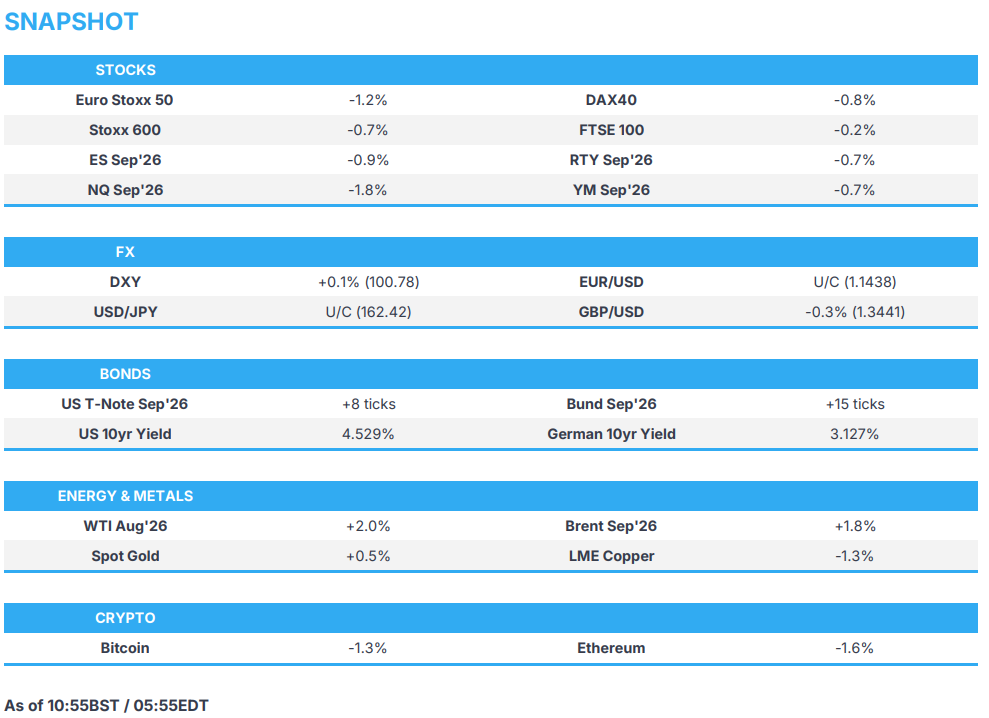

US Market Open: NQ -1.5% but off lows after weak APAC lead, USD and Fixed lifted on haven demand

0:00--:--

- The US continued to strike Iran, for a sixth consecutive night; Iran claimed that power facilities, bridges and civilian infrastructure were struck.

- Iranian Army Spokesman warned that if the US strike the infrastructure of Iran, all infrastructure in the region will be a legitimate target; he added that “either all countries in the region can export oil or no one can”.

- US equities slump after further worries of stretched AI valuations.

- DXY gains; JPY saw fleeting strength following PM Takaichi's GPIF comments.

- Fixed income benchmarks supported by safe haven flows.

- Crude futures higher after multiple UKMTO reports in the Middle East.

- Looking ahead, highlights include US Building Permits (Jun), Export/Import Prices (Jun), Industrial Production (Jun), UoM Consumer Expectations (Jul) & Atlanta Fed GDP.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.7%) are broadly lower, following on from the weakness in Asia (Nikkei -4%, Hang Seng -2.1%), with clear underperformance seen in the AEX (-1.0%) and FTSE MIB (-0.8%).

- Tech (ASML -4.2%, STMicroelectronics -6.9%) is the clear underperformer following the sharp selloff overnight in APAC names, as worries of stretched valuations persist. Despite the selloff, this week has been broadly positive in the tech space, with both TSMC and ASML reporting strong Q2 figures that beat estimates. Today's weakness just shows that, despite positive news, concerns over the AI capex and its current momentum persist.

- In terms of the broader sector space, the bias is mixed. Utilities (+1.5%) top the sector pile, followed by Food, Beverages & Tobacco (+0.9%) and Telecoms (+1.1%). Outside of Tech (-2.9%), Basic Resources (-2.1%) and Banks (-1.2%) are the sector laggards.

- US equity futures are lower across the board, with underperformance in the NQ (-1.9%), given the tech weakness overnight. After-hours, Netflix (-9% pre-market) reported Q2 earnings that came broadly in-line with expectations, but investors were left disappointed by its earnings forecast, with Q3 EPS and Revenue guidance missing estimates. For SpaceX (-3.5% pre-market) , shares fell below its IPO price of USD 135 for the first time on Thursday after the launch of Flight 13 was aborted.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mixed against Buck with recent outperformers AUD and GBP underperforming against the Greenback, while Thursday’s CHF underperformance reverses.

- USD is modestly firmer today as it gains some haven demand as stocks (NQ -1.9%) slip as tech weakness remains a theme. A couple of factors are driving today, but to summarise, Nikkei 225 was the target for selling amid the KOSPI closure overnight (due to domestic holiday), which saw stocks take a stronger negative lead from APAC and help the Buck. Aside from this, macro newsflow is light with crude a touch firmer as US and Iran continue to exchange strikes for the sixth day.

- GBP, which is set for a fourth week of gains, pulls back a touch from the 1.35 level as participants await the coronation of incoming PM Burnham. EUR/GBP also saw Sterling outperform for its fourth week, but like Cable, off recent lows as it reclaims 0.85. There remains a level of uncertainty around the incoming PM, with none of his cabinet officials confirmed as of yet, and many policies still unknown. ING expects a return to 0.870 in EUR/GBP by late summer.

- JPY is flat against the Buck despite c. 30pips of downside seen this morning. Japanese PM Takaichi said the govt. would pursue steps that encourage investment in Japanese financial assets, including by households and pension funds like the GPIF. To remind, last week FinMin Katayama said she would pursue steps to promote investment in Japanese assets by GPIF and others. There was some scepticism around this remark as it would be a textbook tactic to encourage domestic investment and passively limit outflows - Katayama is not in a position to direct changes, it would be under the jurisdiction of the Labour Ministry. We await further updates with a timeline around any potential GPIF changes, for now, JPY flat against the Buck near 162.50 despite earlier gains.

FIXED INCOME

- Fixed income benchmarks are firmer across the board, despite a clear driver; however, debt could be finding some haven flows as equities print deep selloffs globally.

- Gilts (+26 ticks) outperform, with Andy Burnham to begin his Labour premiership on Monday. Focus will be on who Burnham chooses as Chancellor (widely expected to be Home Secretary Mahmood) and what his plans are for the government. Reporting by Bloomberg stated that he has asked the civil service to prepare plans for new North Sea oil and gas drilling and public control of Thames Water. Regarding the Chancellor position, Mahmood is likely to be named Chancellor, but this has already drawn some backlash. Rachel Maskell told the Times that appointing Mahmood would be a mistake and that Miliband “shines well above Shabana.” Despite this, gilts trade at the top end of its 87.15-87.59 range.

- JGBs (+36 ticks) have steadily bid higher in early European trade, after Japanese PM Takaichi said the government will pursue steps that encourage investment in Japanese financial assets, including by households and pension funds. She even specifically named GPIF. Focus on pension fund investments in domestic assets started after FinMin Katayama said she wanted to encourage the GPIF to invest more. Takaichi's more recent comments would likely strengthen the view that the government is keen to have the GPIF consider altering its asset allocations.

- USTs (+8 ticks) trend higher despite a lack of events on the calendar. Fed's Jefferson gave remarks overnight, stating that it would be appropriate to reconsider the stance in the scenario in which inflation does not start cooling.

COMMODITIES

- The US continued to strike Iran for a sixth consecutive night. Following this, Iran claimed power facilities, bridges and civilian infrastructure were struck. And in response, Iran launched its own strikes on Gulf neighbours.

- More pertinently was a severe warning from the Iranian Army Spokesman. He stated that if the US strike the infrastructure of Iran, all infrastructure in the region will be a legitimate target; He added that “either all countries in the region can export oil or no one can”.

- Other news in the region, the UKMTO received 2 reports. More recently, there was a report 65NM south of Al Mukalia, in which unauthorised personnel boarded the vessel. Sources say armed assailants boarded a chemical products tanker Asana in the Gulf of Aden, which is potentially related.

- Crude benchmarks spent the overnight session in the green, amidst the aforementioned developments. Brent Sep’26 (+1.7%) holds towards the top end of a USD 83.71-85.88/bbl range.

- Spot gold (+0.5%) is incrementally firmer this morning, though still remains just shy of the USD 4k/oz mark, after dipping below that mark in the prior session. Recent pressure has been driven by the ongoing inflationary woes surrounding the latest US-Iran escalation. Nonetheless, some analysts remain confident in the structural drivers for the yellow metal, namely, continued central bank purchases. Elsewhere, base metals are broadly in the red this morning – hampered by the risk tone. 3M LME Copper trades within a USD 13,429-13,563/t range.

- BP (BP/LN) and ConocoPhillips (COP) reportedly set to announce billions of dollars of new investments in Iraq on Friday, CNBC reports; sources said the figure may be in the tens of billions.

- Chinese LNG importers are exploring ways to reduce reliance on Qatar, Bloomberg reported.

- China State Planner NDRC to cut retail fuel prices in the current bi-monthly cycle, effective July 18th. To cut gasoline prices by CNY 300/t, and diesel by CNY 290/t.

- TotalEnergies (TTE FP) cut output at Port Arthur refinery as the reformer is undergoing repairs.

TRADE/TARIFFS

- Brazil's Rosa, on rare earths, said the US asked them to limit investment by other countries that do not comply with market rules, and will not accept this.

NOTABLE EUROPEAN DATA RECAP

- EU Inflation Rate YoY Final (Jun) Y/Y 2.8% vs. Exp. 2.8% (Prev. 3.2%, Low. 2.8%, High. 2.9%).

- EU Inflation Rate MoM Final (Jun) M/M -0.1% vs. Exp. -0.1% (Prev. 0.1%, Low. -0.1%, High. -0.1%).

- EU Core Inflation Rate YoY Final (Jun) Y/Y 2.4% vs. Exp. 2.4% (Prev. 2.6%).

CENTRAL BANKS

- Fed's Jefferson (voter) said the current policy stance should support the job market and allow inflation to resume its decline towards 2% as tariff effects and energy prices pass through. Jefferson said in a scenario where inflation does not start cooling, it could be appropriate to reconsider the stance and ensure they deliver price stability, while he added that current policy is well-positioned to respond based on incoming data, the evolving outlook and balance of risks, and he is firmly committed to returning inflation to the 2% target, consistent with the dual mandate.

- BoJ reportedly sees little need for consecutive rate rises, may reconsider its assessment of economic risks, according to Bloomberg citing sources. It is also likely to raise its growth forecast for this year from its current 0.5%. Officials may revise their downside-risk assessment as AI-related demand supports exports, profits and incomes, while faster cost pass-through keeps underlying inflation risks elevated above the 2% target.

NOTABLE US HEADLINES

- US President Trump announced the immediate declassification of intelligence on elections during his primetime address and noted that China engaged in election-related activities in 2020 and did not want him to win the election, while he claimed that China attempted to manufacture ballots for Biden and worked to influence businesses against him. China's Foreign Ministry denied these accusations.

- US President Trump called on Congress to pass the Save America Act in light of recent revelations.

GEOPOLITICS

MIDDLE EAST

- US President Trump said they will see the fruits of labour in Iran shortly.

- US CENTCOM said forces conducted a new wave of strikes against Iran for the sixth consecutive night to further degrade Iranian military capabilities. The US launched a missile attack on Iranshahr airport, targeted a railway station in Bandar Abbas and struck five bridges in southern Iran. It was also reported that explosions were heard in Ahvaz, Chabahar and Bushehr, with missiles hitting air and naval bases in Bushehr.

- US CENTCOM announced Marines conducted an inspection aboard M/T Wen Yao in the Gulf of Oman on July 16th, while it was separately reported that only three ships crossed the Strait of Hormuz in the last 24 hours, according to marine traffic data cited by Al Jazeera.

- Iran targeted US radars in Kuwait with a drone strike, and explosions were reported at the US Navy's Fifth Fleet Naval Base in Bahrain, while blasts were heard at a US airbase in Qatar and in Erbil, Iraq.

- IRGC claimed to have launched an attack on a US command centre in Syria's Al-Tanf, while it warned no oil or gas will be exported through the Strait of Hormuz as long as US attacks continue.

- Iran has informed allies, including Hezbollah, that the waiting phase is about to end and ordered them to prepare for military scenarios, according to Kann news citing Lebanese press.

- Kuwait’s Defence Ministry said Iranian 'aggression' on Thursday targeted a number of vital facilities, resulting in material damage.

- Iranian armed forces senior spokesperson said they will never allow the US to interfere in the Strait of Hormuz, while he stated that the route Iran has determined in the Strait of Hormuz is safe, and any route outside it will be unsafe and ships will be damaged. The spokesperson also warned that if the US strike the infrastructure of Iran, all infrastructure in the region will be a legitimate target and stated that "Either all countries in the region can export oil or no one can".

- UKMTO has received a report of an incident 19 nautical miles east of Khasab, Oman. Additionally, the UKMTO received another report of an incident 65NM south of Al Mukalia, Yemen, with the vessel boarded by unauthorised personnel. Following this, maritime sources said armed assailants boarded a chemical products tanker Asana in the Gulf of Aden, off the coast of southern Yemen.

- Lebanese sources said the US-Israeli-Lebanon meeting would likely be postponed to finalise technical arrangements, Sky News Arabia reported.

- Islamic Resistance of Iraq put a USD 10mln bounty on US President Trump.

RUSSIA-UKRAINE

- Naftogaz said a Russian drone attack suspended operations at a gas production facility in Ukraine’s Kharkiv region.

CRYPTO

- Bitcoin extended Thursday's lows and slipped below the USD 63k handle.

APAC TRADE

- APAC stocks were pressured as the tech selling rolled over from Wall St and with sentiment weighed on by US-Iran escalation, in which the US conducted a sixth consecutive night of strikes on Iran and targeted infrastructure, including an airport, railway station and several bridges.

- ASX 200 was dragged lower by weakness in mining, materials, resources and tech, while telecoms, energy and defensives were at the other end of the spectrum, helping cushion the downside.

- Nikkei 225 underperformed and took the brunt of the semiconductor sell-off in the absence of its South Korean counterpart due to Constitution Day, while Kioxia was heavily pressured and has shed 50% of its market cap from last month's peak.

- Hang Seng and Shanghai Comp conformed to the downbeat mood amid the tech-related woes, and with sentiment also not helped by US President Trump's primetime address, in which he accused China of meddling in the 2024 US Election and called for Congress to pass the SAVE America Act.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Takaichi said the government will pursue steps that encourage investment in Japanese financial assets, including by households and pension funds like the GPIF.

- Chinese President Xi said that the world has entered an unprecedented period of AI innovation, adding they should seize rare historic opportunities to encourage open source AI.

- China FX regulator said foreign investments into China saw net inflows in H1 and outbound investments continue to grow steadily.