Published: 8 Jul 2026, 10:55 UTC

Newsquawk Desk

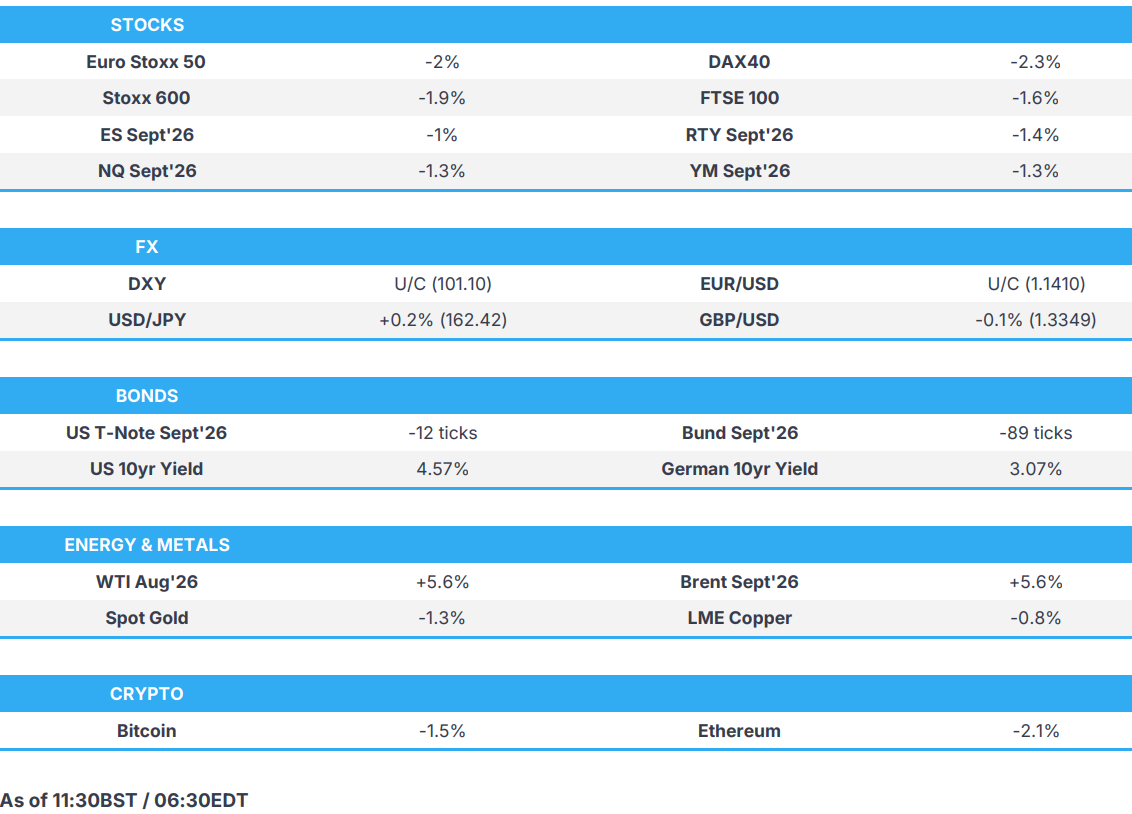

US Market Open: Risk-off trade as Trump casts doubts over US-Iran ceasefire

0:00--:--

- US President Trump said the Iran ceasefire is over, "I think", lifting Brent above USD 79/bbl, weighing on equities and fixed income.

- However, Trump did add he will allow US negotiators to continue talking with Iran, but said, "I think this is a waste of time"

- Euro Stoxx 50 -2.2%, ES -1.0%, NQ -1.4% given the above. Mixed APAC trade, but China was in the green after updates relating to DeepSeek and Zhiphu.

- Apple signed an agreement with Broadcom, to design and produce custom silicon components and wireless technologies, deal expected to exceed USD 30bln.

- NZD outperforms after the RBNZ hiked and signalled further increases "appear likely". Elsewhere, CAD bid on energy moves while JPY slips as a result of its import dependence and yield moves.

- Looking ahead, US Atlanta Fed GDP (Q2), NBP Policy Announcement (Jul), NBH Minutes (Jun), Fed Minutes (Jun), NATO Ankara Summit, Speakers include US President Trump, Supply from the US.

IRAN CONFLICT

Overnight:

- US CENTOM announced that it completed a new round of offensive strikes, hitting over 80 targets with precision munitions. CENTCOM added that forces remain postured and prepared to hold Iran accountable when the agreement is not adhered to or obeyed.

- Several explosions have been heard in Bushehr, Iran, according to Mehr news; Mehr's journalist on Kharg Island denies reported of an attack on Kharg, despite some reported of an incident being published.

- In response, Iran's IRGC said they hit 85 important US military installations in Port Salman, Bahrain's 5th Maritime Zone and Kuwait's Ali Salem Air Base.

Trump stated he "thinks" the ceasefire with Iran is "over":

- US President Trump said the Iran ceasefire is over "I think"; as far as I am concerned, it is a waste of time dealing with Iran. On the MoU, "think it is over". Adds, "I do not want to deal with Iran", they are a "bunch of liars".

- US President Trump said (on Iran) he will allow US negotiators to continue to talk if they want. But, "I think this is a waste of time".

Full updates can be found in the geopolitical section at the bottom of the sheet.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -1.8%) began the session lower amid renewed US-Iran developments which spurred energy benchmarks higher. The move then extended after US President Trump suggested that he thinks the ceasefire with Iran is "over".

- European sectors in Europe are entirely negative (excl. Energy +2%) as they react to elevated energy prices.

- Stateside, US equity futures are hit this morning in reaction to the above geopolitical updates. RTY (-1.4%) underperforms as yields move higher, NQ (-1.3%) also affected but to a lesser extent as tech recently underperformed.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- G10s are mostly lower against the Buck excl. commodity exporters CAD and NOK, which are resilient vs. the USD.

- USD rose throughout the morning in reaction to energy strength alongside sour equity sentiment after US President Trump said he thought the Iran ceasefire was over. To briefly summarise developments, yesterday the US Treasury revoked the June 21st Iran-related waiver, General License X, which had allowed Iran to produce, deliver and sell its oil; and US President Trump’s remarks this morning accelerated the move higher in USD/oil with “Iran ceasefire is over "I think" the kicker.

- Kiwi was the clear outperformer post RBNZ, but reversed gains against the Buck after the aforementioned Trump remarks. To briefly recap, the RBNZ hiked rates by 25bps in a unanimous decision, signalling further hikes to bring inflation to the 2% target mid-point; this saw some participants unwind bets for a hold. AUD/NZD appears the preferred vehicle to express the in-line/hawkish decision, now the Buck has picked up.

- JPY continues to underperform amid carry/Terms of Trade implications. USD/JPY remains on a 162.00 handle and has essentially pared that downside seen on potential intervention fears last week having risen throughout the London morning. Reporting overnight via Asahi and Nikkei noted that the Japanese government may tweak a reference to monetary policy in its annual policy agenda to avoid the appearance that it is putting pressure on the BoJ.

FIXED INCOME

- Fixed income started on the backfoot, as benchmarks gradually moved lower as energy continued to move higher overnight given the US revoked Iran’s oil waiver and then conducted strikes on 80 Iranian targets in retaliation to Iran targeting various cargo vessels on Tuesday.

- The early morning saw modest additional pressure, with Bunds and USTs lower by roughly 40 and five ticks, respectively, at first. The scheduled docket ahead featured supply and a few data points, but we were primarily awaiting comments from the US and/or Iran after the overnight action.

- US President Trump then spoke in Ankara, in a relatively short but packed interview where he said the ceasefire with Iran is over “I think” and specifically on the MoU said, “think it is over”. An update that sparked a marked and continuing move higher in energy, with crude firmer by over 6% and Dutch TTF by over 5%. As such, yields across the curve have jumped, benefiting the short-end most, and curves are bear-flattening globally, though with the US belly faring almost the same as the short-end.

- USTs down to a 108-29 base, lower by 13 ticks. We now look to the US 10yr note auction after Tuesday’s 3yr, and thereafter Fed Minutes for June, which will be scoured for further insight into how the first meeting led by Warsh went and how any discussions/disagreements among the board were presented; with particular reference to any mention around Warsh’s view on forward guidance.

- Bunds went down to around 125.30 following the above energy action and Trump language, lower by over 80 ticks. Energy-related action aside, the main focus point was a dismal first tap of a 2036 Bund, drawing a b/c of just 1.03x. Results of this sent Bunds lower by nearly 10 ticks, to a 125.23 base.

- Gilts opened lower by 57 ticks, acknowledging the US waiver removal yesterday and the tit-for-tat strikes overnight. Thereafter, as Trump spoke, further downside was seen, sending Gilts lower by 130 ticks in total to an 87.16 base. As usual, Gilts underperform amid periods of pronounced energy upside given the sensitivity of the UK market to global benchmarks.

- Germany sold EUR 3.902bln vs exp. EUR 6bln 3.00% 2036 Bund: b/c 1.03x, average yield 3.09%, retention 35%.

- UK sold GBP 1.5bln 0.125% 2028 Treasury Gilts via Tender: b/c 4.97x (prev. 4.28x), average yield 3.989% (prev. 4.219%), tail (prev. 0.3bps).

- Jefferies (JEF) to sell EUR-denominated 7yr noted; guidance seen +175bps to MS.

- Spain has reportedly proposed the EU issue an annual EUR 850bln in bonds to save countries billions of euros in interest costs, POLITICO reported.

- Australia sold AUD 900mln 4.25% 2036 AGBs: b/c 4.55x (prev. 3.86x), average yield 4.8745% (prev. 4.9735%).

COMMODITIES

- Following Iran’s decision to hit Saudi and Qatari tankers, the US struck various sites in Iran. As a result, Iran then hit regional partners, including Bahrain and Kuwait.

- US President Trump, who was speaking at the NATO Summit in Ankara, berated the Iranian regime. He stated that it is a waste of time dealing with Iran, and ultimately stated that he thinks the ceasefire and MoU is “over”. The mention of he “thinks”, gives the US a little bit of optionality on whether the deal is actually over; he stated that he will allow US negotiators to continue to talk. Nonetheless, the risks of a wider escalation remain; markets now await clarification on whether the MoU has officially ended, the Iranian response and also how Qatari/Pakistani mediators react to the comments made by Trump.

- WTI and Brent started the European session with gains in excess of 2%, but surged higher following the Trump comments; currently +5.6%. WTI Aug’26 holds at the top end of a USD 71.75-75.30/bbl range, whilst Brent Sept’26 sits near peaks of USD 75.44-79.26/bbl range. The latter remains well below the levels seen following the initial signing of the Islamabad MoU (USD 85/bbl), which signals some hopes that a) the Strait will remain open, b) the current MoU holds. On this theme, markets remain in backwardation, with front-month Brent prices still higher than second-month; should this flip, it would indicate that traders expect another large-scale supply glut.

- Spot gold (-1.2%) trades lower this morning, and at the bottom end of a USD 4,050-4,133/oz range. Much of the pressure came following the Trump comments, given the USD strength and the inflationary implications of the ceasefire being over. Base metals are broadly lower, given the risk-tone; 3M LME Copper trades at USD 13,190-13,396/t range.

- Kuwait’s Ministry of Electricity said power lines were damaged by shrapnel in recent attacks.

- European Commission, on the ETS revision, said they are still considering how and whether to add international carbon credits. Revision will include permanent domestic carbon removal. Will propose further investment.

- Russia’s Gazprom said Ukraine attacked facilities of gas exports to Turkey; supplies not affected.

- China reportedly lifts restrictions on refined fuel exports for the rest of July, according to sources.

- China purchases at least 5 more US soybean cargoes, Bloomberg reported.

- Japan aluminium premiums for Jul-Sep shipment set at USD 395/t, +12-13% Q/Q.

- US Private Inventory Data (bbls): Crude -0.399mln (exp. -1.5mln), Distillates -1.801mln (exp. +1mln), Gasoline -2.929mln (exp. -1.55mln), Cushing -0.069mln.

TRADE/TARIFFS

- Spanish PM Spokesperson said the trade comments from US President Trump are business as usual.

- USTR Greer said Canada and Mexico have not lived up to everything.

NOTABLE EUROPEAN HEADLINES

- US President Trump said he is not happy with NATO when it comes to Greenland. Spain is a wasted cause, they do not want to do trade. Cutting off all trade with Spain and all visits. "Do not want to do any more trade with them (Spain)". Treasury Secretary Bessent has been told to cut off all trade with Spain. US is paying too much into NATO. UK and Italy were both terrible in not allowing the US to use military bases. Greenland is not important to Denmark.

NOTABLE EUROPEAN DATA RECAP

- Swedish CPIF MoM Prel (Jun) M/M 0.3% (Prev. 0.9%).

- Swedish CPIF YoY Prel (Jun) Y/Y 1.3% vs exp. 1.2% (Prev. 1.5%).

- Swedish Inflation Rate MoM Prel (Jun) M/M 0.4% (Prev. 1%).

- Swedish Inflation Rate YoY Prel (Jun) Y/Y 0.7% (Prev. 0.8%).

- Swedish GDP MoM (May) M/M 0.9% (Prev. 0.5%).

CENTRAL BANKS

- The RBNZ hikes the OCR by 25bps to 2.50%, as expected; some further reduction in monetary stimulus is likely to be required to return inflation to the 2% target mid-point.

- RBNZ's Breman said inflation may have already peaked; seeing the economy rebounding now as oil prices fall. We are gradually moving rates towards neutral. Neutral rate is uncertain, with the range of 2.5-3.5%. Bringing inflation back down is needed to bring back demand. Felt it was needed that uncertainty has increased on rate timing.

- Westpac retains call for RBNZ OCR hike in September.

- BoJ's Asada said a rate hike could slow the economy.

- RBA Assistant Governor Hunter said the Board will act as needed to ensure inflation returns to target and the labour market to sustainable full employment.

- PBoC set USD/CNY mid-point at 6.8077 vs exp. 6.8018 (prev. 6.8054).

NOTABLE US HEADLINES

- South Korea's Foreign Ministry said they have signed an MoU with the US and Japan on cooperation to deploy small modular reactors.

CRYPTO

- Bitcoin is on the backfoot this morning, following the negative risk-tone; currently holding around the USD 62k mark.

GEOPOLITICS

IRAN COMMENTARY:

- Iranian Parliament Speaker Ghalibaf said the US has violated major parts of the MoU, citing US attacks on southern Iran, reinstating oil sanctions and threats of further strikes as MoU violations.

- Iran's Foreign Ministry states that the US activity overnight has "rendered important and fundamental parts of the Memorandum of Understanding on the End of the War ineffective".

- Iranian President Pezeshkian said the US, whether as World Cup host or in its foreign policy, manipulates the rules and resorts to deception, and that Iran rejects such tactics.

- Iran's top joint miliary command said Iran will give a crushing response to America's aggression and terrorist action, and under no circumstances will they allow them to interfere in the affairs of the Strait of Hormuz and its management.

- Advisor to Iran's Supreme Leader said US President Trump intends to attack again and we are fully prepared.

- Iran's Foreign Ministry condemns the US Treasury's move to revoke the temporary suspension of sanctions on Iranian oil sales, will take any measure it deems necessary to safeguard its interests and national security. Iran holds the US government responsible for the consequences of the breach of the Memorandum of Understanding.

OVERNIGHT ATTACKS:

- Several explosions have been heard in Bushehr, Iran, according to Mehr news; Mehr's journalist on Kharg Island denies reported of an attack on Kharg, despite some reported of an incident being published. Elsewhere, sirens were reported in Bahrain once again.

- Renewed explosions sounds heard around Iran's Qeshm and Sirik, Mehr reported.

- Iran's army said it targeted the Sheikh Isa Base in Bahrain and warns of more attacks if the US repeats strikes on Iran, Mehr reported.

- Iran's IRGC said that, in response to the US aggression, they hit 85 important US military installations in Port Salman, Bahrain's 5th Maritime Zone and Kuwait's Ali Salem Air Base.

- Iran's IRGC said they downed a US Mq9 drone in the south of Iran, Press TV reported.

- Iran fires several anti-ship missiles and drones towards US Navy warships in the Sea of Oman, Fars reported citing the Middle East Spectator.

- A US official said the strike on Iran was a punitive action, not a proportional response, and that the operation will not end in the short term, CNN reported.

US COMMENTARY

- US President Trump said the Iran ceasefire is over "I think"; as far as I am concerned, it is a waste of time dealing with Iran. On the MoU, "think it is over". Adds, "I do not want to deal with Iran", they are a "bunch of liars".

- US President Trump said (on Iran) he will allow US negotiators to continue to talk if they want. But, "I think this is a waste of time".

- US President Trump said have had some great meetings; attacked very powerfully against Iran last night. Have wasted a lot of time with Iran. Iran does not know what it is doing. Iran shot rockets at the ships, which is why the US shot back. Iran is a "dirty" player, "are scum".

- US President Trump approved the Iran strike plan and ordered it while in Turkey, a US official tells Axios' Ravid; the official said it is still unclear how long the strikes are going to continue.

- US Secretary of Defence Hegseth has cancelled his visit to Israel, N12/Ynet report.

OTHERS

- Turkish President Erdogan said Europe must take more responsibility when it comes to NATO.

- US President Trump said China is attempting to takeover the Panama Canal, will not let this happen. China has been treating the US right. Big fan of Chinese President Xi.

- Ukrainian Armed Forces said Kyiv is under missile attack.

- Israeli fighter jets carried out attacks in Barachit and Beit Yahoun in southern Lebanon.

- A Pakistani Boeing (BA) plane flying to Karachi has crashed, with sources stating the plane was mistakenly targeted by the US, IRIB reported.

- Chevron’s (CVX) Yasa Polaris oil tanker, used for CPC shipments, was attacked by drones off Russia’s Black Sea coast, according to sources.

- Russia’s Gazprom said Ukraine attacked facilities of gas exports to Turkey; supplies not affected.

- Ukraine's Military said it struck two oil refineries, six tankers, bridges and the Borisoglebsk airfield; AIF-NK oil refinery in Nizhny Kamsk was also damaged.

APAC TRADE

- Asia-Pac stocks traded mixed, with Chinese indices the only region in the green amid multiple IPOs and strength in China's tech space. Sentiment from the US session carried over in the Asia-Pac session, as energy prices surged amid the re-escalation of US-Iran tensions.

- ASX 200 continued to be weighed on by metals, with the Metals & Mining sector the worst performer, with Materials followed. Energy topped the sector pile

- Nikkei 225 started on the softer side, briefly returned to the unchanged mark before returning to the downside.

- KOSPI traded choppy, as the initial weakness briefly reversed to print modest gains. However, weakness returned as the session continued, resulting in the Korea Exchange activating the sidecar on the KOSPI and KOSDAQ. As a result, the KOSPI extended its losses from June peak to 20%, indicating a bear market.

- Shanghai Comp. and Hang Seng. were the only indices printing gains, with outperformance in the Hang Seng following strength in tech names. The strength can be attributed to two reports: 1) From Reuters, DeepSeek developing its own chip to power AI systems, and 2) from the Information, Zhiphu considering designing its own AI chip.

NOTABLE ASIA-PAC HEADLINES

- China's MIIT has issued a risk warning regarding the potential security backdoors in the AI programming tool Claude Code.

- South Korean Government said companies with consolidated assets of over KRW 10tln will be required to disclose information on their ESG performance and risks, starting 2028.

- South Korean Finance Minister said they are to watch risk factors around stock market volatility, will enhance FX monitoring system to respond to night-time volatility.

- Japan is considering a change to monetary policy wording in the Honebuto, Asahi reported.

NOTABLE APAC DATA RECAP

- Japanese Eco Watchers Survey Current (Jun) 44.0 vs. Exp. 44.6 (Prev. 43.6).

- Japanese Eco Watchers Survey Outlook (Jun) 45.7 (Prev. 40.7).

- Japanese Bank Lending YoY (Jun) Y/Y 5.7% vs. Exp. 5.8% (Prev. 5.7%).

- Japanese Current Account (May) 3.968B vs. Exp. 4121B (Prev. 3907B).

- Australian Private House Approvals MoM Final (May) M/M 2.8% vs. Exp. 2.8% (Prev. -1%).

- Australian Building Permits YoY Final (May) Y/Y 5.3% vs. Exp. 5.3% (Prev. 10.2%).

- Australian Building Permits MoM Final (May) M/M -1.1% vs. Exp. -1.1% (Prev. -3.4%).